By GraphDex Research · Reviewed for accuracy May 2026

Quick Answer

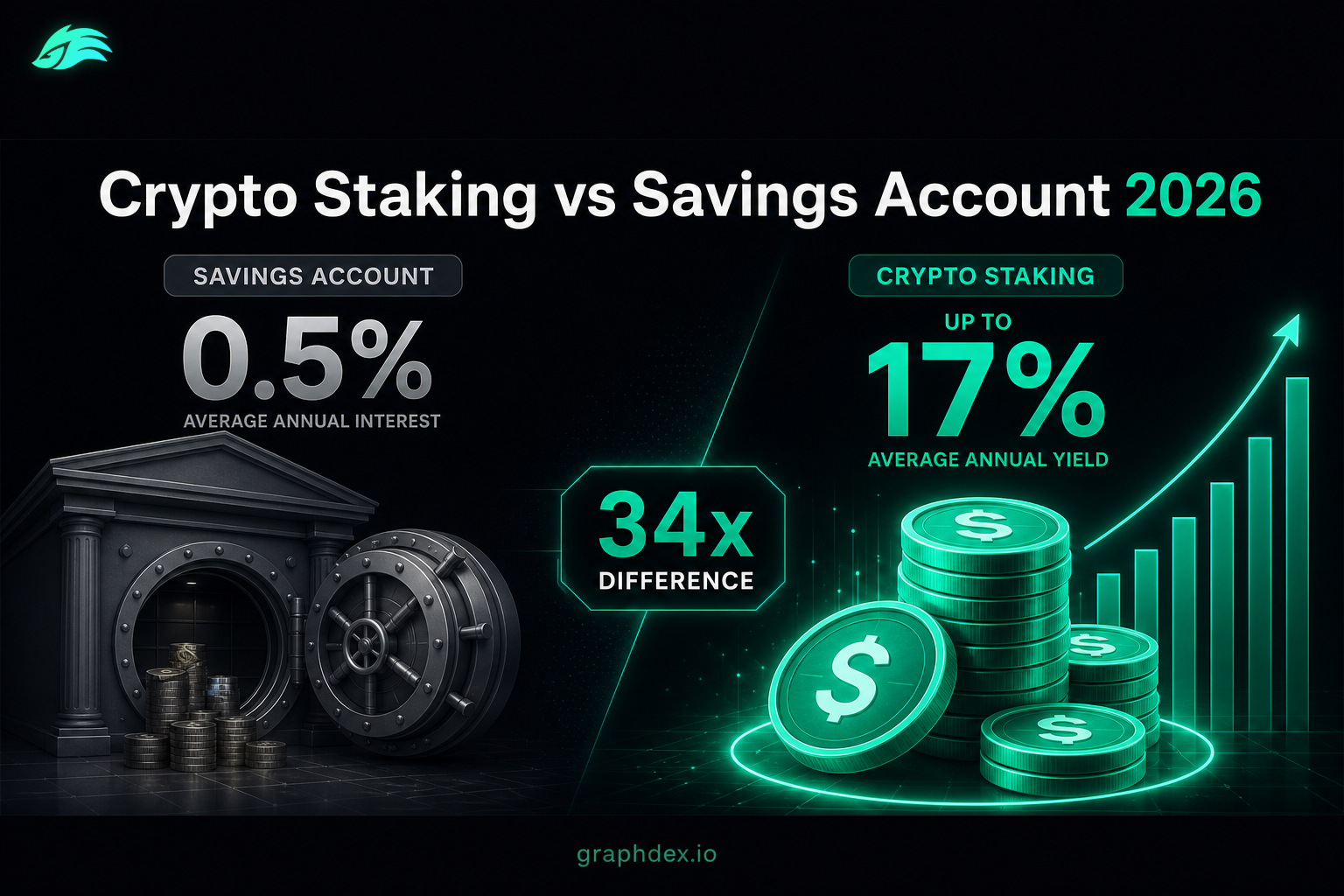

Crypto staking pays dramatically more than a savings account — but carries different risks.

- Savings account: 0.5% APY typical (4-5% high-yield), FDIC-insured, fully regulated

- Crypto stablecoin staking: up to 17% APY, not insured, platform/smart contract risk

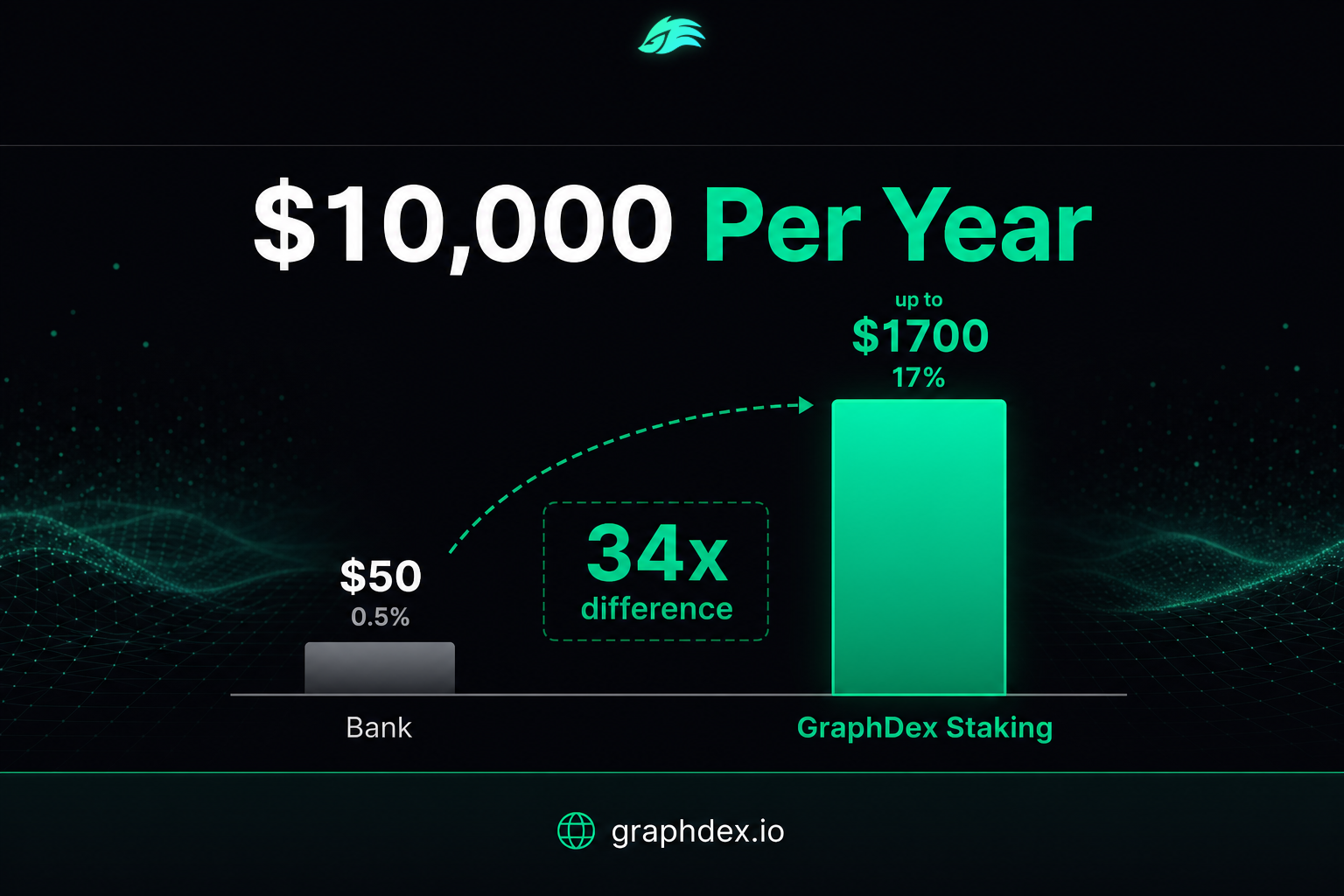

A $10,000 deposit earns about $50 a year in a typical savings account versus up to $1,700 staking stablecoins. The trade-off is insurance and regulation versus yield. Many people use both: emergency funds in a bank, working capital in stablecoin staking.

Earn up to 17% on stablecoins with GraphDex

Key Takeaways

- Crypto stablecoin staking pays up to 17% APY vs ~0.5% for typical savings accounts — a massive yield gap.

- Savings accounts are FDIC-insured and regulated; crypto staking is not insured and carries platform risk.

- Stablecoin staking avoids crypto price volatility — your principal stays pegged to the dollar.

- A common approach: keep emergency funds in a bank, working capital in stablecoin staking.

Crypto Staking vs Savings Account: The Core Comparison

| Factor | Savings Account | Crypto Stablecoin Staking |

|---|---|---|

| Typical yield | 0.5% (4-5% high-yield) | Up to 17% |

| Insurance | FDIC (US, to $250k) | None |

| Regulation | Fully regulated | Varies by platform |

| Access | Business hours / delays | 24/7 instant |

| Principal stability | Yes | Yes (pegged to USD) |

| Minimum balance | Often required | Low (from $50-100) |

| Who controls funds | The bank | You (non-custodial) or platform |

The headline difference is yield: stablecoin staking pays many times more than even high-yield savings accounts. The headline difference in the other direction is insurance: savings accounts are government-backed, staking is not.

Everything else flows from this fundamental trade-off between regulated safety and higher returns.

How Much More Does Staking Earn?

The yield gap is dramatic. Here's what the same deposit earns over a year:

| Deposit | Savings (0.5%) | High-Yield Savings (4.5%) | Stablecoin Staking (up to 17%) |

|---|---|---|---|

| $1,000 | $5 | $45 | Up to $170 |

| $10,000 | $50 | $450 | Up to $1,700 |

| $50,000 | $250 | $2,250 | Up to $8,500 |

| $100,000 | $500 | $4,500 | Up to $17,000 |

Even compared to the best high-yield savings accounts, stablecoin staking offers several times the return. Against a typical savings account, the difference is enormous — up to 34x more on the same money.

This gap exists because the yield sources are different. Banks pay you a small fraction of what they earn lending your deposits. Crypto staking platforms pass through more of the yield — whether from lending, network rewards, or, in GraphDex's case, platform trading fees.

Why Are Crypto Staking Yields So Much Higher?

A reasonable question: if staking pays 34x a savings account, what's the catch? The answer lies in where the yield comes from and what protections you give up.

Banks operate on a wide margin. Your bank lends your deposits at, say, 7% and pays you 0.5%, keeping the difference. Heavy regulation, branch networks, and overhead also limit what they can pass through.

Crypto platforms pass through more. Whether from lending (Aave, exchanges), network rewards (Proof-of-Stake), or platform fees (GraphDex), crypto staking returns a larger share of the underlying yield to you. There's less overhead and less margin-taking.

You take on more risk. The higher yield compensates for giving up FDIC insurance and accepting platform and smart contract risk. This is the core trade-off — you're paid more because you're protected less.

Stablecoins avoid one risk entirely. Unlike staking volatile tokens, stablecoin staking keeps your principal pegged to the dollar, so you get the higher yield without crypto price exposure.

Understanding this makes the decision clearer: staking isn't "free money," it's a different risk-reward profile than banking.

See how GraphDex generates up to 17% yield

What You Give Up: The Honest Trade-Offs

To compare fairly, here's what crypto staking lacks versus a savings account:

No FDIC insurance. US bank deposits are insured up to $250,000. If your bank fails, you're made whole. Crypto staking has no equivalent government guarantee — if a platform fails, recovery depends on the platform.

Platform risk. Custodial staking platforms can fail (FTX, Celsius). Non-custodial platforms like GraphDex reduce this by keeping funds in your wallet, but smart contract risk remains.

Regulatory uncertainty. Banking is heavily regulated with clear consumer protections. Crypto regulation is still evolving and varies by jurisdiction.

Self-responsibility. With a bank, the institution handles security. With non-custodial staking, you're responsible for your own wallet security (though modern platforms like GraphDex simplify this with Privy — no seed phrase to lose).

These trade-offs are real. The question isn't whether staking is "better" universally — it's whether the higher yield justifies the trade-offs for a given portion of your money.

How to Reduce the Risk Gap

You can narrow the safety difference between staking and savings with smart choices:

Stake stablecoins, not volatile tokens. This eliminates price volatility — your principal stays at dollar value, just like a bank balance.

Use non-custodial platforms. Platforms like GraphDex keep funds in your wallet, eliminating the custodial risk that caused the biggest crypto losses. This is the closest structural equivalent to not trusting a single institution.

Choose transparent, audited platforms. Favor platforms with security audits, track records, and clear yield sources over unknown ones offering suspicious rates.

Diversify. Don't put everything in one platform. Spread across platforms, or split between staking and traditional banking.

Match commitment to liquidity needs. Use flexible terms for funds you might need, longer locks only for committed capital.

With these choices, stablecoin staking on a non-custodial, audited platform offers a risk profile far closer to banking than the "crypto is risky" stereotype suggests — while still paying many times the yield.

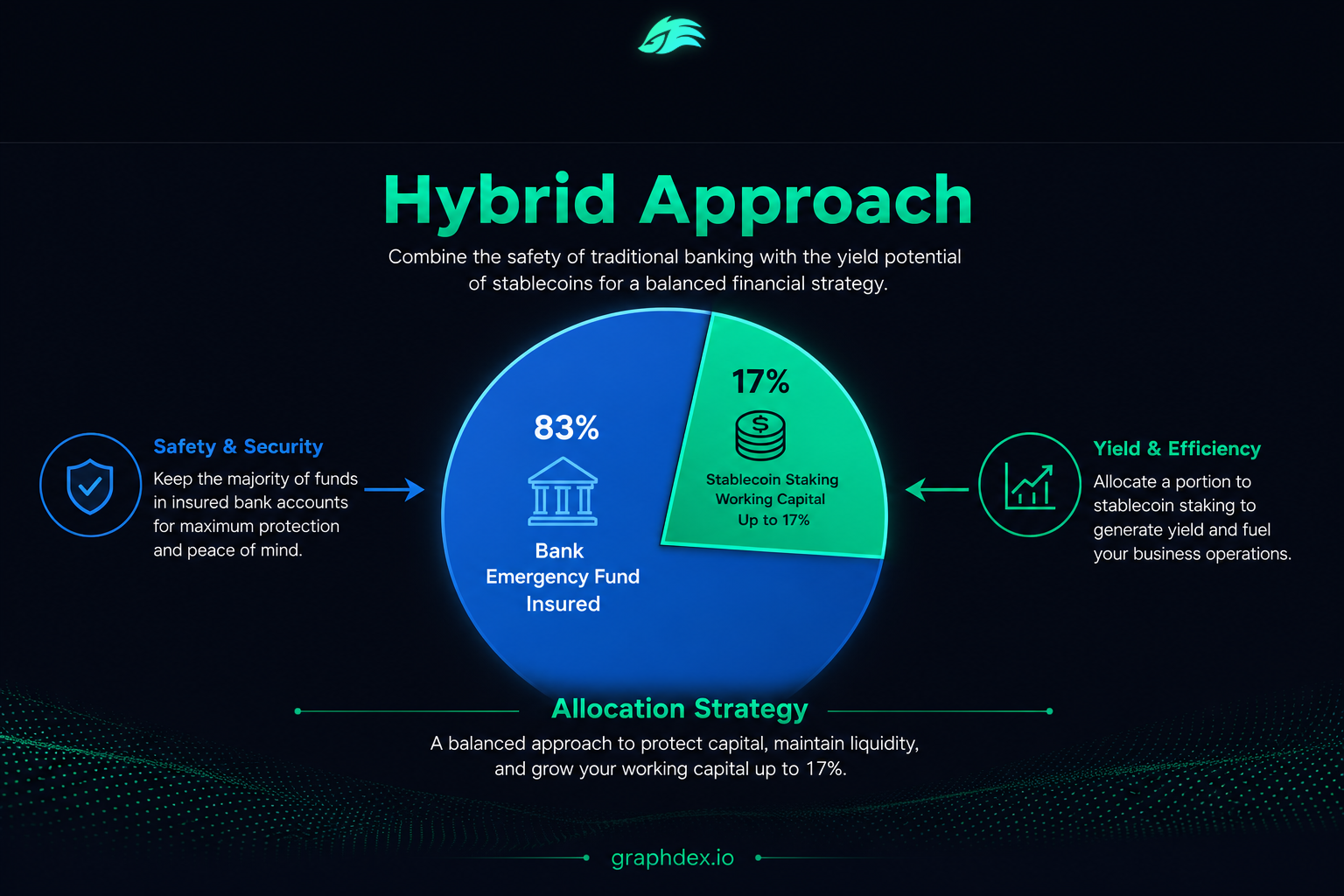

The Hybrid Approach: Best of Both Worlds

For most people, the smartest answer isn't choosing one or the other — it's using both strategically.

Keep in a bank:

- Emergency fund (3-6 months of expenses)

- Money you might need on short notice

- Funds you cannot afford to put at any risk

Put in stablecoin staking:

- Working capital you want earning meaningful yield

- Medium-term savings you won't need immediately

- The portion of your portfolio where higher returns justify the trade-offs

This hybrid approach captures the safety of insured banking for your essential reserves and the superior yield of staking for capital that can tolerate the different risk profile. A $50,000 saver might keep $15,000 in an insured bank for emergencies and stake $35,000 in stablecoins — earning up to $5,950 a year on the staked portion versus about $75 if it sat in a typical savings account.

Put your working capital to work on GraphDex

Crypto Staking vs Savings: Which Is Right for You?

Choose a savings account for:

- Emergency funds you cannot risk

- Money you need government-insured

- Funds requiring instant traditional banking access

- If you're entirely uncomfortable with any crypto risk

Choose crypto stablecoin staking for:

- Capital you want earning meaningful yield

- Money you can commit for defined periods

- The portion of your wealth where up to 17% beats 0.5%

- If you're comfortable using a non-custodial platform

Choose both (recommended) for:

- A balanced approach — insured reserves plus high-yield working capital

- Most people, most of the time

The decision isn't ideological. It's about matching each portion of your money to the right risk-reward profile.

Inflation: The Hidden Factor

There's a dimension to this comparison that most savings-versus-staking discussions overlook: inflation.

When inflation runs at 3-4% a year, money sitting in a 0.5% savings account is actually losing purchasing power. You're earning 0.5% nominally but losing 2.5-3.5% in real terms. Your dollars grow on paper while buying less in reality.

This reframes the comparison. A savings account isn't just "low yield" — at typical rates, it's a guaranteed slow erosion of purchasing power during inflationary periods. Even high-yield savings at 4-5% barely keeps pace with inflation, leaving little real growth.

Stablecoin staking at up to 17% changes this calculation. After accounting for 3-4% inflation, you're still earning a substantial real return — purchasing power that actually grows rather than erodes. For capital you want to preserve and grow against inflation, the yield difference becomes even more significant in real terms than the nominal numbers suggest.

This doesn't eliminate the risk trade-offs discussed earlier. But it does mean the "safe" choice of a low-yield savings account carries its own hidden cost: the quiet loss of purchasing power over time. For the portion of your money that can tolerate staking's risk profile, the real-terms advantage compounds the case.

A Realistic Perspective

Crypto staking versus savings isn't a simple "crypto good, banks bad" story — or the reverse. Both have legitimate roles.

Savings accounts provide irreplaceable safety for money you cannot risk: emergency funds, near-term obligations, capital that must be there with certainty. The FDIC guarantee is real and valuable.

Stablecoin staking provides yield that banking cannot match, for capital that can tolerate a different risk profile. With non-custodial, audited platforms and stablecoins that avoid price volatility, the risk is manageable and understood — not the wild speculation crypto is sometimes assumed to be.

The mature approach uses each for what it does best. As stablecoin staking matures and non-custodial platforms like GraphDex make it safer and simpler, more people are allocating a thoughtful portion of their savings to capture the yield difference — while keeping their essential reserves in insured banking.

Start earning more on your dollars with GraphDex

Frequently Asked Questions

Is crypto staking better than a savings account? Crypto staking pays far more (up to 17% vs ~0.5% for typical savings) but lacks FDIC insurance and carries platform risk. It's "better" for yield, a savings account is "better" for guaranteed safety. Many people use both — banks for emergency funds, staking for working capital.

How much more does crypto staking pay than a bank? A typical savings account pays 0.5%; stablecoin staking on GraphDex pays up to 17% — roughly 34x more. On $10,000, that's about $50 a year from a bank versus up to $1,700 from staking. Even high-yield savings (4-5%) pays several times less than staking.

Is crypto staking as safe as a savings account? No — savings accounts are FDIC-insured and government-regulated, while crypto staking is not. However, non-custodial stablecoin staking (like GraphDex) significantly narrows the gap by avoiding price volatility and keeping funds in your control. The risk profile is different, not necessarily catastrophic.

Can I lose my money staking instead of using a bank? Yes — staking carries platform risk, smart contract risk, and (for volatile tokens) price risk, none of which apply to insured bank deposits. Stablecoin staking on non-custodial, audited platforms minimizes these risks but doesn't eliminate them. Never stake money you cannot afford to risk.

What's the safest way to earn high yield on dollars? Stake stablecoins (USDT/USDC) on a non-custodial, audited platform. This keeps your principal at dollar value, eliminates custodial risk, and pays far more than a bank. GraphDex offers non-custodial stablecoin staking up to 17% APY.

Should I move my savings into crypto staking? Not all of it. A balanced approach keeps emergency funds in an insured bank and puts working capital you can commit into stablecoin staking. This captures both the safety of banking for essentials and the higher yield of staking for the rest.

Do I pay tax on crypto staking like bank interest? In most jurisdictions, both staking rewards and bank interest are taxable as income. Staking tax treatment varies by country and can be more complex. Keep records and consult a tax professional. This is general information, not tax advice.

About This Guide

This guide is published by the GraphDex Research team — analysts and traders building the infrastructure for digital asset trading on Solana. Our content is based on live platform data, current market figures, and hands-on experience with the platforms covered.

Sources & data: Yield figures and comparisons reflect publicly available information as of 2026. APY rates are variable and not guaranteed; staking carries risk and is not FDIC-insured. This guide is educational and not financial advice.

GraphDex is the infrastructure for digital asset trading — trade, predict, and earn in one place. Learn more at graphdex.io.

Last reviewed: May 2026 · GraphDex Research

The infrastructure for digital asset trading. Trade, predict, stake, repeat. graphdex.io