By GraphDex Research · Reviewed for accuracy May 2026

Quick Answer

To beat inflation in 2026, you need investments that earn more than the inflation rate (forecast up to 4.2%). The main strategies:

- Move idle cash out of checking (0.07%) into high-yield options

- High-yield savings / CDs: ~4%, FDIC-insured

- TIPS and I-Bonds: inflation-linked government bonds

- Dividend stocks and stocks: 7-10% long-term growth

- Real assets (real estate, gold, commodities): traditional hedges

- Stablecoin staking: up to 17%, well above inflation

The core principle: never let money sit idle losing value. Put each dollar into something that earns more than inflation erodes.

Earn up to 17% — well above inflation — with GraphDex

Key Takeaways

- Inflation in 2026 is forecast as high as 4.2%, while average checking accounts pay just 0.07%.

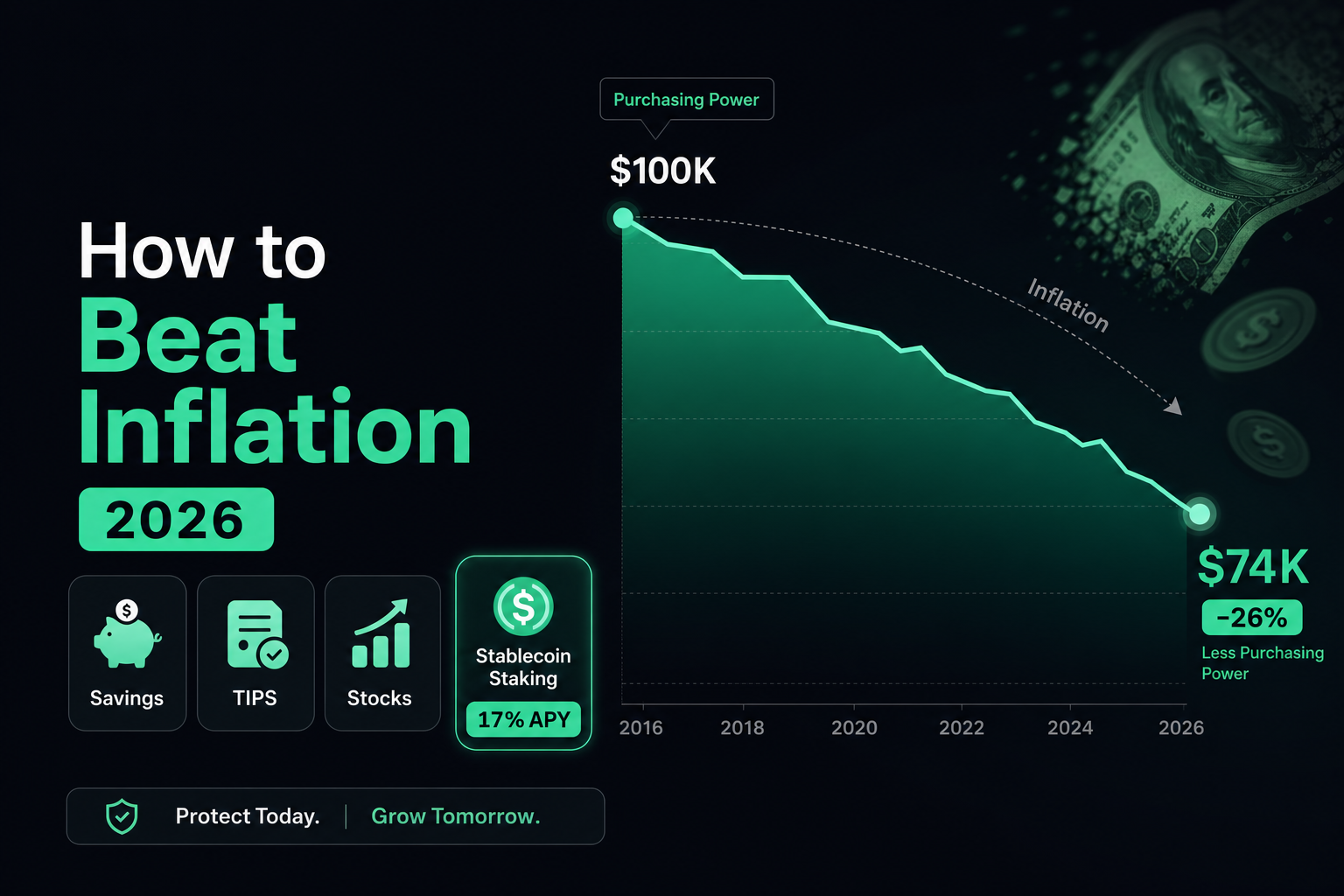

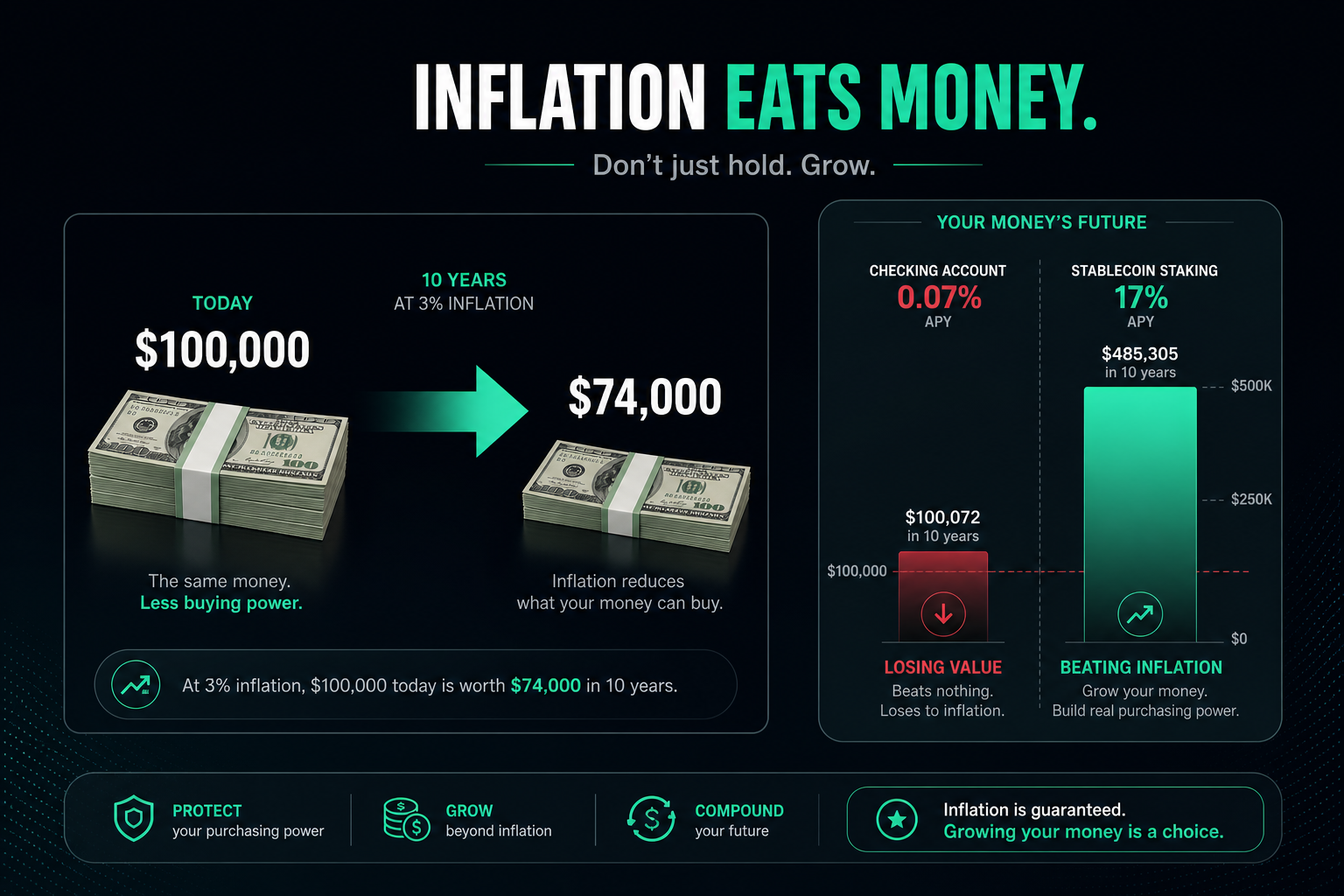

- At 3% inflation, $100,000 loses about a quarter of its purchasing power over 10 years.

- To beat inflation, your money must earn more than the inflation rate — idle cash guarantees a loss.

- Options range from TIPS and dividend stocks to stablecoin staking at up to 17% APY.

Why Is Inflation Destroying Your Savings?

Inflation is the increase in the cost of goods and services over time, and it directly erodes your purchasing power. As prices rise, your dollars buy less than they used to.

The numbers in 2026 are stark. US consumer prices rose 3.3-3.8% year over year, and the OECD raised its US inflation forecast from 2.8% to 4.2% for 2026. Meanwhile, the average checking account pays just 0.07% — meaning money sitting there loses roughly 4% of its real value every year.

Over time, this compounds dramatically. At just 3% annual inflation, $100,000 in purchasing power today becomes roughly $74,000 in ten years. At 4%, it drops to about $68,000. Your money doesn't disappear — it just buys less of everything, slowly and relentlessly.

This is why doing nothing is not a safe option. Leaving cash idle in a low-interest account is a guaranteed loss of purchasing power. Beating inflation requires putting your money into assets that earn more than the inflation rate.

How to Beat Inflation: 8 Strategies Compared

| Strategy | Typical Return | Inflation-Beating? | Risk |

|---|---|---|---|

| High-yield savings / CDs | ~4% | Marginally | Very low |

| TIPS / I-Bonds | Inflation + small premium | Yes (designed to) | Very low |

| Treasury bills | ~4% | Marginally | Very low |

| Dividend stocks | 3-9% | Usually | Moderate |

| Stocks (long-term) | 7-10% | Yes (historically) | High short-term |

| Real estate / REITs | 5-12% | Yes (traditional hedge) | Moderate-high |

| Gold / commodities | Variable | During high inflation | Variable |

| Stablecoin staking | Up to 17% | Yes (well above) | Platform risk |

1. Move Idle Cash Out of Checking

The first and easiest step: stop leaving large balances in a checking account paying 0.07%. This is the single biggest inflation mistake — and the easiest to fix.

Move cash you don't need for daily spending into a high-yield option. Keep an emergency fund covering 3-6 months of expenses somewhere accessible, but make sure even that money is working — in a high-yield savings account, not idle.

This one move alone can swing your idle cash from losing ~4% a year to roughly breaking even or better against inflation.

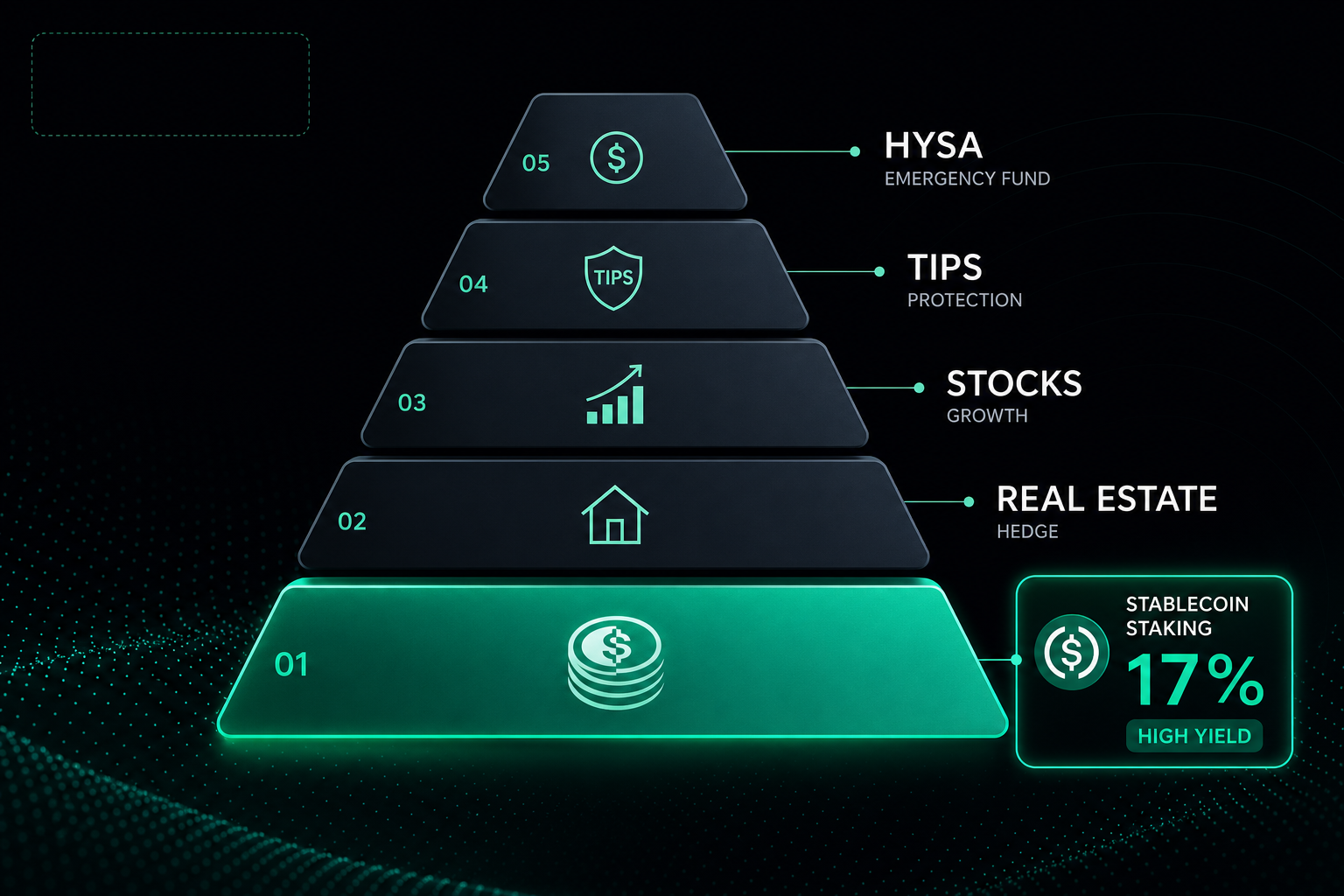

2. High-Yield Savings Accounts and CDs

High-yield savings accounts (HYSAs) and certificates of deposit can earn as much as 4% APY in 2026 — and they're FDIC-insured up to $250,000 per depositor.

Pros: FDIC-insured, liquid (HYSA), predictable. Cons: ~4% barely keeps pace with 3-4% inflation; after taxes, real returns can be near zero. Best for: Emergency funds and cash you need accessible.

HYSAs help, but they only marginally beat inflation — they protect purchasing power rather than grow it.

3. TIPS and I-Bonds — Built to Beat Inflation

Treasury Inflation-Protected Securities (TIPS) and Series I Savings Bonds are specifically designed to keep pace with inflation. Their value or interest adjusts with the inflation rate, so they protect the fixed-income portion of your portfolio from inflation risk.

Pros: Government-backed, explicitly inflation-linked, very safe. Cons: Returns are modest (inflation plus a small premium); purchase limits on I-Bonds. Best for: Conservative investors wanting guaranteed inflation protection.

4. Dividend Stocks and Stock Market Growth

Over long periods, the growth potential of stocks has historically been one of the most reliable defenses against inflation. The S&P 500 has historically delivered average returns of 9-10% over decades — well above inflation.

Dividend stocks add regular income (top payers yield 6.8-9.4%) plus growth. Companies with pricing power can raise prices during inflation, protecting their margins.

Pros: Strong long-term growth, beats inflation historically, dividends provide income. Cons: High short-term volatility, requires riding out downturns. Best for: Long-term wealth building and growth that outpaces inflation.

5. Real Estate and REITs

Real assets like real estate tend to rise in value along with inflation, making them a traditional inflation hedge. Rental income can outpace inflation, and property appreciates over time. REITs offer the same exposure with stock-like liquidity.

Pros: Traditional inflation hedge, tangible, income plus appreciation. Cons: Direct real estate is illiquid and capital-intensive; property market risk. Best for: Inflation protection through real assets — REITs for liquidity, direct for control.

6. Gold and Commodities

Gold has limited supply — unlike currency, which governments can print more of — giving it a hedge against inflation and currency debasement. During inflationary periods, commodities and commodity-related stocks (energy, metals, miners) tend to outperform the broader market.

Pros: Time-tested inflation hedge, holds value during currency debasement. Cons: No yield (gold), volatile, returns inconsistent. Best for: A portfolio hedge against high inflation and currency risk.

7. Infrastructure and Private Credit

Infrastructure assets (toll roads, utilities, data centers) can generate inflation-linked cash flows through contracts that adjust with inflation. Private credit, the fastest-growing alternative asset class, often carries floating rates that rise automatically when the Fed raises rates to fight inflation.

Pros: Contractual inflation linkage, floating rates rise with inflation. Cons: Often requires advisors or platforms; lockup periods. Best for: Sophisticated investors seeking alternative inflation hedges.

8. Stablecoin Staking — Yield Well Above Inflation

A newer strategy gaining traction: staking dollar-pegged stablecoins to earn yield far above inflation. On platforms like GraphDex, stablecoin staking pays up to 17% APY — comfortably above even the OECD's elevated 4.2% inflation forecast.

Pros: Yield well above inflation (up to 17%), dollar-stable principal, 24/7 access, low minimums. Cons: Not FDIC-insured, platform and smart contract risk, newer than traditional options. Best for: The portion of your portfolio where you want high real returns and can tolerate platform risk.

The math is compelling for inflation specifically: at up to 17% yield against ~4% inflation, you earn a real return of roughly 13% — versus losing ~4% in checking or barely breaking even in savings. Because stablecoins hold their dollar value, you get this inflation-beating yield without crypto's price volatility.

See how stablecoin staking beats inflation on GraphDex

How Do You Build an Inflation-Proof Portfolio?

No single strategy is the complete answer. The most resilient approach combines several, matched to your needs:

For accessible cash: High-yield savings (FDIC-insured, ~4%) for your emergency fund, so even reserves aren't losing as much to inflation.

For guaranteed protection: A portion in TIPS or I-Bonds, which explicitly track inflation.

For long-term growth: Stocks and dividend stocks, historically the strongest inflation defense over time.

For real-asset hedging: Real estate (or REITs) and a small gold/commodity allocation.

For high real yield: A stablecoin staking allocation at up to 17%, generating returns well above inflation on dollar-stable assets.

This diversified approach protects across economic environments. The key principle: don't let any meaningful amount sit idle losing value. Every dollar should be in something that earns more than inflation erodes — whether that's the safety of TIPS, the growth of stocks, or the high yield of stablecoin staking.

Add an inflation-beating allocation with GraphDex

Frequently Asked Questions

How do I beat inflation in 2026? Put your money into investments that earn more than the inflation rate (forecast up to 4.2%). Move idle cash out of checking (0.07%) into high-yield options, use TIPS/I-Bonds for guaranteed protection, stocks for long-term growth, and consider stablecoin staking at up to 17% for yield well above inflation.

What is the best investment to beat inflation? There's no single best — it depends on your risk tolerance. TIPS and I-Bonds are designed to track inflation safely. Stocks beat it historically over time. Stablecoin staking at up to 17% offers the highest margin above inflation, with platform risk. A diversified mix is most resilient.

Why is leaving money in the bank a bad idea during inflation? The average checking account pays 0.07% while inflation runs 3-4%. That means idle cash loses roughly 4% of its real value every year. At 3% inflation, $100,000 becomes about $74,000 in purchasing power over ten years. Doing nothing guarantees a loss.

Can stablecoin staking beat inflation? Yes. At up to 17% APY versus ~4% inflation, stablecoin staking earns a real return of roughly 13%. Because stablecoins are pegged to the dollar, you get this inflation-beating yield without crypto price volatility — though it isn't FDIC-insured and carries platform risk.

How much does inflation cost me each year? At 3-4% inflation, every $10,000 of idle cash loses $300-400 of purchasing power annually. Over a decade, $100,000 loses about $26,000-32,000 in real value. The higher the inflation rate and the lower your returns, the faster your money erodes.

What are inflation-proof investments? Investments that rise with prices or yield above inflation: TIPS and I-Bonds (inflation-linked), stocks (long-term growth), real estate and REITs (real assets), gold and commodities (during high inflation), and stablecoin staking (high yield). Diversifying across several is the most resilient approach.

Is gold or stablecoin staking better for beating inflation? Gold is a time-tested hedge that holds value but produces no yield. Stablecoin staking generates up to 17% yield, well above inflation, but isn't a tangible asset and carries platform risk. Many investors hold gold as a hedge and stablecoin staking for high real yield — they serve different roles.

About This Guide

This guide is published by the GraphDex Research team — analysts building the infrastructure for digital asset trading on Solana. Our content is based on live platform data and current market figures.

Sources & data: Inflation forecasts, rates, and return figures reflect publicly available information as of 2026 and are estimates. All investments carry risk; returns are not guaranteed. Stablecoin staking is not FDIC-insured. This guide is educational and not financial advice — consult a financial advisor for your situation.

GraphDex is the infrastructure for digital asset trading — trade, predict, and earn in one place. Learn more at graphdex.io.

Last reviewed: May 2026 · GraphDex Research

The infrastructure for digital asset trading. Trade, predict, stake, repeat. graphdex.io