By GraphDex Research · Reviewed for accuracy May 2026

Quick Answer

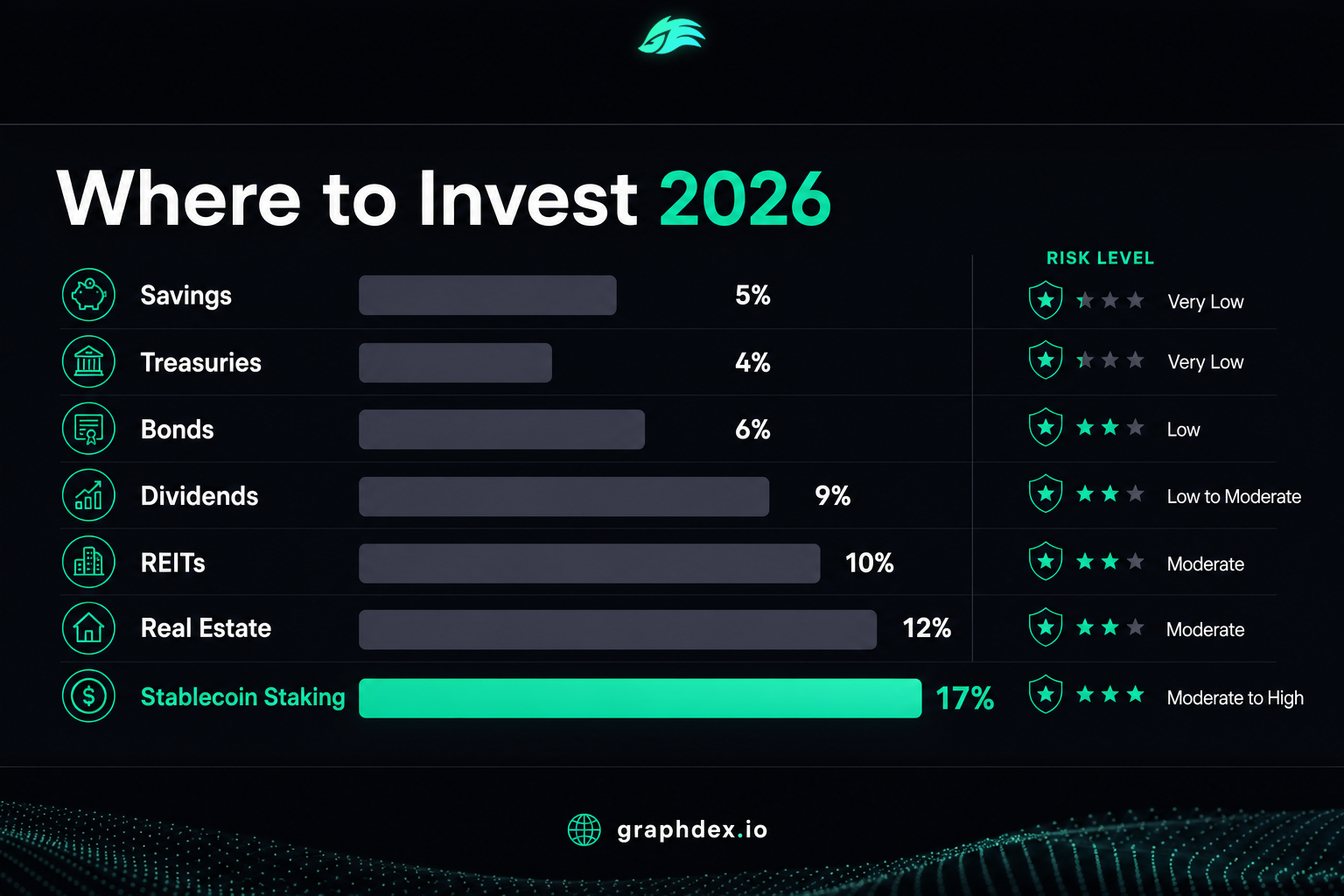

The main places to invest money in 2026, ranked roughly by typical return:

- High-yield savings / CDs: 4-5%, very low risk, FDIC-insured

- Treasury securities: ~4%, government-backed, very safe

- Bonds: 4-6%, low-moderate risk

- Dividend stocks: 3-9%, moderate risk, market-dependent

- REITs / real estate: 5-10%, property market risk

- Stablecoin staking: up to 17%, platform risk, not insured

The right choice depends on your risk tolerance, time horizon, and how hands-on you want to be. Most balanced portfolios combine several.

Earn up to 17% on stablecoins with GraphDex

Key Takeaways

- There is no single best investment — the right mix depends on risk tolerance, time horizon, and capital.

- Safe options (savings, Treasuries) pay 4-5%; higher-yield options carry more risk.

- Stablecoin staking offers up to 17% — far above traditional yield — but isn't FDIC-insured.

- A diversified approach spreads risk across asset classes rather than betting on one.

How Should You Think About Where to Invest?

Before comparing options, understand the three dimensions every investment trades off:

Return — how much your money earns, expressed as annual percentage yield or total return.

Risk — the chance of losing principal or seeing volatile returns. Higher returns almost always mean higher risk.

Liquidity and effort — how easily you can access your money and how much active management it requires.

There is no one-size-fits-all strategy. Conservative investors lean toward bonds, Treasuries, and savings. Moderate investors add dividend stocks and REITs. Aggressive investors include higher-risk, higher-return options. The smartest approach for most people is diversification — spreading money across several options so no single failure is catastrophic.

Below, each major option in 2026, compared honestly.

Where to Invest Money in 2026: Full Comparison

| Option | Typical Return | Risk | Liquidity | Insured? |

|---|---|---|---|---|

| High-yield savings | 4-5% | Very low | High | Yes (FDIC) |

| CDs | 4-5% | Very low | Low (locked) | Yes (FDIC) |

| Treasury securities | ~4% | Very low | Moderate | Gov-backed |

| Bonds | 4-6% | Low-moderate | Moderate | No |

| Dividend stocks | 3-9% | Moderate | High | No |

| REITs | 5-10% | Moderate-high | High | No |

| Real estate (direct) | 5-12% | Moderate-high | Very low | No |

| Stablecoin staking | Up to 17% | Platform risk | Moderate | No |

1. High-Yield Savings Accounts and CDs

The simplest entry point. In 2026, top online banks offer 4-5% APY — a major improvement over the near-zero rates of recent years.

Pros: FDIC-insured (US, to $250k), zero volatility, instant access (savings) or fixed return (CDs). Cons: All interest taxed as ordinary income — higher-bracket investors keep only 60-70 cents per dollar. CDs lock capital for a fixed term. Returns barely beat inflation. Best for: Emergency funds and short-term capital you cannot afford to risk.

2. Treasury Securities

US Treasury bills, notes, bonds, and I-Bonds are among the safest income vehicles available — backed by the federal government and largely exempt from state and local tax.

Pros: Virtually no default risk, tax advantages, predictable. Cons: Lower returns (~4%), longer commitments for higher rates. Best for: Conservative investors prioritizing capital preservation.

3. Bonds and Bond Funds

Bonds let you lend money to companies or governments and collect interest. Considered safer than stocks but generally lower-returning. Bond funds (ETFs or mutual funds) spread risk across many bonds.

Pros: Steadier than stocks, diversification, regular income. Cons: Interest rate risk, lower returns than equities, corporate bonds carry default risk. Best for: Balancing a portfolio and reducing overall volatility.

4. Dividend Stocks

Dividend-paying stocks remain a gold standard of passive income — regular payouts plus potential capital appreciation. Top dividend stocks yield 6.8-9.4%, though most are lower.

Pros: Income plus growth potential, generally less volatile than growth stocks, payouts can grow over time. Cons: Requires research, dividends can be cut, market risk to principal. Best for: Investors wanting income plus long-term growth, with some research effort.

5. REITs and Real Estate

Real Estate Investment Trusts (REITs) invest in income-producing properties and must distribute most taxable income as dividends. They offer yields higher than many stocks or bonds, with property market and interest rate risk. Direct real estate ownership provides rental income that can outpace inflation, plus potential appreciation.

Pros: Inflation hedge, tangible asset (direct), high yields (REITs). Cons: Property market risk, interest rate sensitivity, direct ownership is illiquid and management-heavy, high capital required for direct. Best for: Investors wanting real estate exposure — REITs for liquidity, direct for control.

6. Stablecoin Staking

A newer option attracting traditional investors: staking stablecoins (USDT, USDC) earns yield far above traditional savings — up to 17% APY on platforms like GraphDex. Stablecoins are pegged 1:1 to the dollar, so unlike volatile crypto, your principal holds its dollar value.

Pros: Far higher yield (up to 17%), dollar-stable principal, 24/7 access, low minimums. Cons: Not FDIC-insured, platform and smart contract risk, newer and less familiar than traditional options. Best for: Investors comfortable allocating a portion of capital to higher-yield, higher-responsibility options.

How is the yield so much higher? On GraphDex, it comes from platform trading fees rather than the thin margins banks pass through. The trade-off is the absence of government insurance — you accept platform risk in exchange for several times the yield.

Learn how stablecoin staking works on GraphDex

Which Investment Matches Your Goals?

If capital preservation is the priority: Treasuries, high-yield savings, and CDs. You won't beat inflation by much, but your principal is safe and insured.

If you want income with moderate risk: Dividend stocks, bonds, and REITs. Higher yields than savings, with market and property risks.

If you want maximum yield and can tolerate the trade-offs: Stablecoin staking offers up to 17% on dollar-pegged assets, far above traditional options, in exchange for platform risk instead of insurance.

If you want a balanced portfolio (most people): Combine several. For example: emergency fund in high-yield savings, core in dividend stocks and bonds, real estate exposure via REITs, and a portion in stablecoin staking for high yield. Diversification means no single setback derails you.

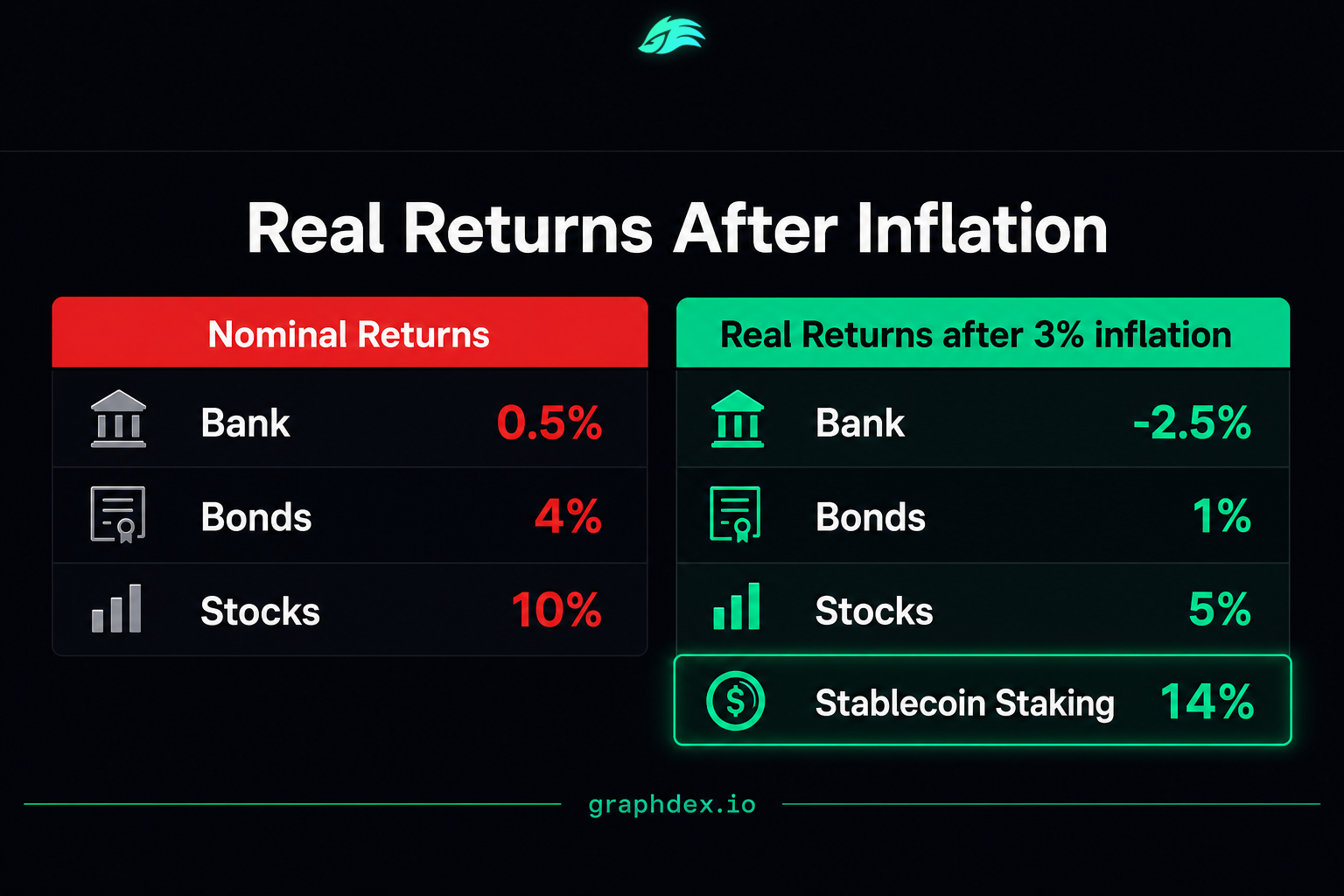

How Does Inflation Affect Your Returns?

A consideration that reshapes the comparison: inflation. With inflation around 3% in 2026, any investment returning less than that loses real purchasing power.

A savings account at 4.5% offers only ~1.5% real return after inflation. Treasuries at 4% barely keep pace. This is why investors increasingly look beyond traditional safe options — the "safe" 4-5% is a slow erosion in real terms once you account for inflation and taxes.

Higher-yield options — dividend stocks, REITs, and stablecoin staking at up to 17% — offer meaningful real returns above inflation. The trade-off is always more risk. The key is allocating each portion of your money to match its purpose: safety for capital you must protect, higher yield for capital that can tolerate risk.

How to Get Started with Higher-Yield Options

For traditional investors curious about stablecoin staking specifically, the entry is simpler than expected:

Step 1: Choose a reputable, non-custodial platform. Non-custodial means you keep control of your funds (eliminating the platform-failure risk that affected FTX).

Step 2: On GraphDex, register with email or social login via Privy — your wallet is created automatically, no seed phrase, no technical setup.

Step 3: Fund with USDC or USDT (dollar-pegged stablecoins).

Step 4: Choose your amount and term, and start earning up to 17% APY.

The onboarding takes minutes and feels like any modern fintech app — while paying multiples of a savings account.

Common Investing Mistakes to Avoid

Whether you're new to investing or experienced, these mistakes cost people money and are worth avoiding.

Chasing the highest yield blindly. A 17% yield isn't automatically better than 5% if the risk is mismatched to your needs. Match each investment to its purpose — safety for emergency funds, higher yield only for capital that can tolerate risk.

Failing to diversify. Putting everything in one asset class — all stocks, all real estate, all crypto — concentrates risk. A downturn in that single class can devastate your portfolio. Spreading across several smooths the ride.

Ignoring inflation and taxes. The "safe" 4-5% from savings barely beats inflation, and after taxes on ordinary income, real returns can be near zero. Always think in real, after-tax terms.

Locking up money you'll need. Don't put emergency funds in illiquid investments like real estate or fixed-term products. Match liquidity to your needs.

Letting emotion drive decisions. Selling stocks in a panic during downturns, or piling into an asset because it's trending, destroys returns. Discipline and a long-term plan beat reactive moves.

Not starting at all. Perhaps the biggest mistake: leaving money in a near-zero checking account out of indecision. Even conservative options like high-yield savings or stablecoin staking beat doing nothing — and compounding rewards starting early.

Avoiding these mistakes matters more than picking the single "best" investment. A diversified, disciplined approach across appropriate asset classes builds wealth more reliably than chasing any one option.

Put idle money to work with GraphDex

Frequently Asked Questions

Where is the best place to invest money in 2026? There's no single best place — it depends on your risk tolerance and goals. Safe options (savings, Treasuries) pay 4-5%; dividend stocks and REITs pay 5-10% with more risk; stablecoin staking pays up to 17% with platform risk. Most balanced portfolios combine several.

What investment has the highest return in 2026? Among lower-volatility options, stablecoin staking offers among the highest yields at up to 17% APY (versus 4-5% for savings). Stocks and real estate can return more over time but with higher volatility and risk. Higher return always means higher risk.

Where can I invest money safely with good returns? For safety with insurance, high-yield savings and Treasuries pay 4-5%. For higher yield with dollar-stable principal, stablecoin staking pays up to 17% but isn't insured. Diversifying across both balances safety and yield.

Is crypto staking a good investment compared to stocks or real estate? Stablecoin staking offers higher, more predictable yield (up to 17%) without price volatility, but lacks the long-term appreciation potential of stocks or real estate — and isn't insured. Many investors use it for a portion of their portfolio alongside traditional assets.

How much money do I need to start investing? It varies: stablecoin staking starts from $50-100, dividend stocks from the price of one share, Treasuries from $100, while direct real estate requires substantial capital. Low-barrier options let you start small and scale.

What's the safest investment with the highest yield? For insured safety, high-yield savings at 4-5%. For higher yield without price volatility (but no insurance), stablecoin staking up to 17% on non-custodial platforms. The "safest high yield" depends on whether insurance or yield matters more to you.

Should I move money from my savings account to higher-yield investments? Keep emergency funds and money you can't risk in insured savings. For capital that can tolerate more risk, higher-yield options (dividend stocks, REITs, stablecoin staking) offer better returns. A balanced approach uses both.

About This Guide

This guide is published by the GraphDex Research team — analysts building the infrastructure for digital asset trading on Solana. Our content is based on live platform data and current market figures.

Sources & data: Return figures reflect publicly available information as of 2026 and are estimates based on market conditions. All investments carry risk; returns are not guaranteed. Stablecoin staking is not FDIC-insured. This guide is educational and not financial advice — consult a financial advisor for your situation.

GraphDex is the infrastructure for digital asset trading — trade, predict, and earn in one place. Learn more at graphdex.io.

Last reviewed: May 2026 · GraphDex Research

The infrastructure for digital asset trading. Trade, predict, stake, repeat. graphdex.io