By GraphPay Research · Reviewed for accuracy May 2026

Quick Answer

Crypto card KYC levels are tiered verification stages — each unlocking higher limits and more features:

- KYC Level 1 (Simplified): Minimal verification (email, sometimes phone). Lowest limits, fastest setup. Best for testing or small online payments.

- KYC Level 2 (Standard): Phone + basic identity details. Moderate limits, more features (often mobile pay). Best for regular online spending.

- KYC Level 3 (Full): Government ID, selfie, proof of address. Highest limits, full features (physical cards, highest caps). Best for everyday primary spending.

Why tiers exist: Global regulations — FATF rules, the EU's MiCA framework (fully mandatory by July 1, 2026), and Visa/Mastercard network requirements — require identity verification scaled to transaction size. Higher limits legally require more verification.

The smart approach: Start at Level 1 to test the card, then upgrade only when you need higher limits or a physical card. With a non-custodial card like GraphPay, your funds stay in your wallet at every level.

Get a GraphPay card — start at Level 1

Key Takeaways

- KYC levels are tiered: Level 1 (minimal) → Level 2 (standard) → Level 3 (full), each unlocking higher limits.

- Tiers exist because regulations (FATF, MiCA, card networks) require verification scaled to transaction size.

- Start at Level 1 to test; upgrade only when you need higher limits or a physical card.

- A non-custodial card keeps your funds in your wallet regardless of KYC level.

What Are KYC Levels on a Crypto Card?

KYC stands for "Know Your Customer" — the identity verification that regulated financial services perform on users. On crypto cards, KYC isn't a single yes-or-no checkpoint. In 2026, it's a tiered system: you start at a basic level with quick setup and lower limits, then verify progressively to unlock higher limits and more features.

The core principle: More verification unlocks more capability. A Level 1 card might let you spend a modest amount per month with just an email. A Level 3 card — with full identity verification — unlocks much higher limits, physical cards, and full feature access.

This tiered model exists for a simple reason: regulations require identity verification proportional to financial activity. Small, low-risk transactions can use lighter verification; larger amounts legally require more.

Why this matters for you: Understanding KYC levels lets you choose the right tier for your needs. If you just want to make occasional online payments with crypto, Level 1 may be all you need. If you want a physical card for everyday spending, you'll want Level 3. Matching the level to your use case avoids both unnecessary verification and frustrating limits.

An important clarification: Tiered KYC is the legitimate, compliant model used by regulated card issuers worldwide. It's not about avoiding verification — it's about scaling verification appropriately to your usage. This is fundamentally different from the unregulated "anonymous card" schemes that regulators have largely eliminated and that carry serious risks of frozen funds and sudden shutdowns.

Why Do Crypto Cards Use Tiered KYC?

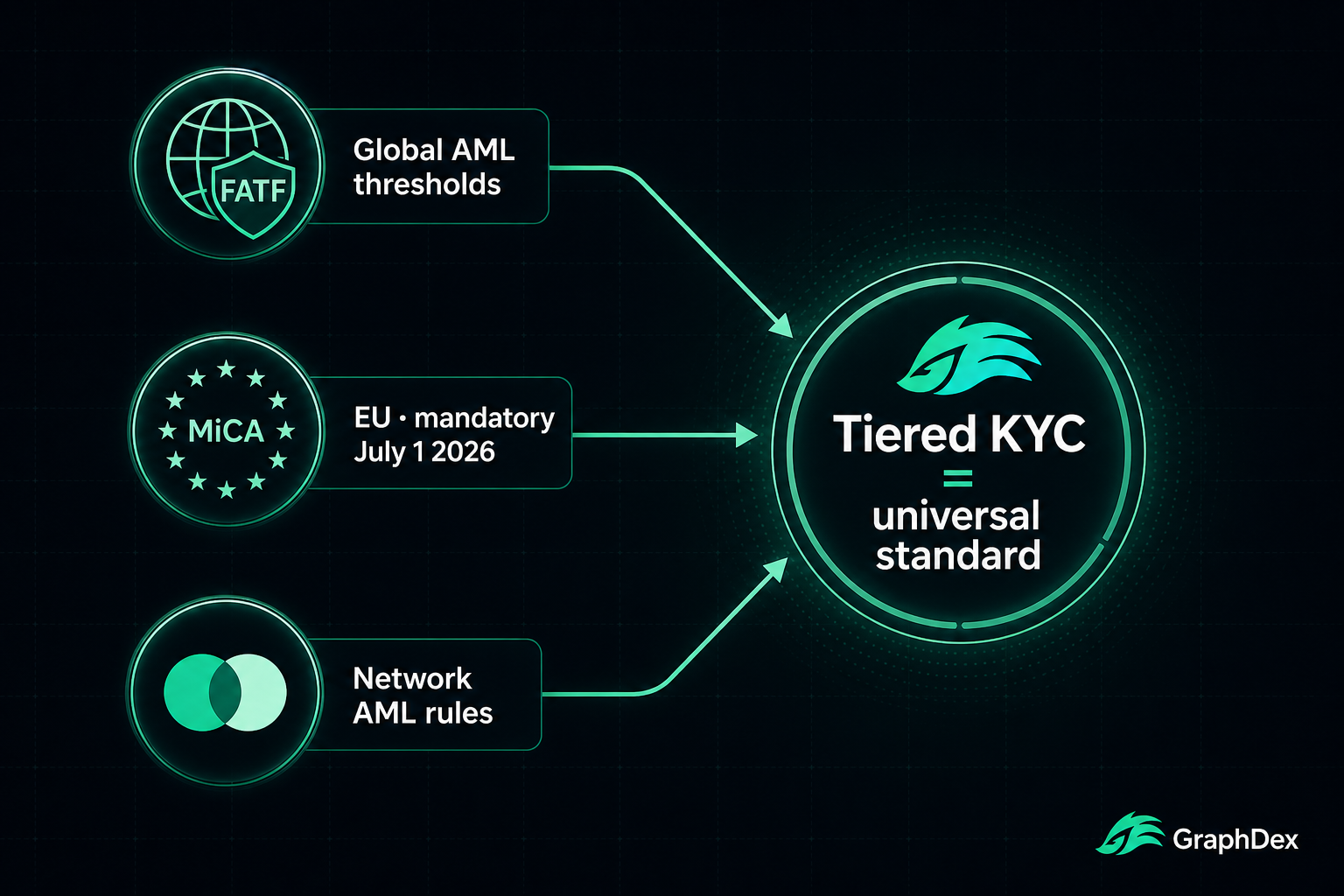

Three regulatory and structural forces make tiered KYC the universal standard in 2026.

Global AML Regulations (FATF)

The Financial Action Task Force (FATF) sets global anti-money-laundering standards. It requires Virtual Asset Service Providers (VASPs) to collect and transmit identifying information for transactions above certain thresholds. This means small transactions can use lighter verification, but larger amounts trigger mandatory identity checks — exactly the tiered model.

The EU's MiCA Framework

The Markets in Crypto-Assets (MiCA) regulation is the EU's comprehensive crypto framework. By July 1, 2026, all Crypto-Asset Service Providers (CASPs) operating in the EU must achieve full MiCA compliance. MiCA mandates identity verification for regulated crypto services — making compliant, tiered KYC the only sustainable model for card issuers serving European users.

Card Network Requirements (Visa/Mastercard)

Visa and Mastercard require their issuing partners to follow AML standards. Any crypto card running on these networks — which is virtually all of them, since these networks provide global merchant acceptance — must implement identity verification. This is why genuinely anonymous cards on major networks have essentially disappeared: the networks themselves require compliance.

The combined effect: These three forces make tiered KYC universal. Rather than a binary "verified or not," cards offer graduated levels that balance accessibility (quick Level 1 entry) with compliance (full Level 3 for higher limits). This benefits users — you get fast initial access while retaining the option to unlock more as needed.

KYC Level 1: Simplified Verification

The entry tier — designed for speed and minimal friction.

What's Required

Typically just an email address, sometimes a phone number. No government ID, no selfie, no proof of address. Setup often takes minutes.

What You Get

- A virtual card, usually issued instantly

- The ability to load crypto and spend at merchants

- Lower spending limits (appropriate for the minimal verification)

- Fast, frictionless onboarding

Best For

- Testing the card before committing to full verification

- Small online payments — subscriptions, digital services

- Privacy-conscious users who want to minimize data sharing for low-value transactions

- Quick access when you need a card immediately

Limitations

- Lower spending limits than higher tiers

- Often virtual-only (no physical card)

- May not support mobile pay (Apple Pay / Google Pay) at this tier

- Higher per-transaction costs on some providers

Level 1 is the ideal starting point — verify your needs match the card before deciding whether to upgrade.

KYC Level 2: Standard Verification

The middle tier — balancing accessibility with expanded capability.

What's Required

Phone verification plus basic identity details. Some providers may request limited additional information. More than Level 1, but typically still faster and lighter than full document verification.

What You Get

- Higher spending limits than Level 1

- Often unlocks mobile pay (Apple Pay / Google Pay)

- More feature access

- Still relatively quick to complete

Best For

- Regular online spending beyond occasional small payments

- Users who want mobile pay but don't need maximum limits

- A middle ground between Level 1's restrictions and Level 3's full verification

Limitations

- Limits still below Level 3

- May not unlock physical cards (these often require full KYC)

- Requirements vary by provider and jurisdiction

Level 2 suits users who've outgrown Level 1 limits but don't yet need the full feature set.

KYC Level 3: Full Verification

The top tier — full features and highest limits.

What's Required

Government-issued ID, a selfie or facial scan, and proof of address. This is "full KYC" — the complete verification regulated financial services perform. Modern platforms often complete this in minutes despite the additional documents.

What You Get

- Highest spending limits (often dramatically higher than lower tiers)

- Full feature access

- Physical card eligibility (physical cards almost always require full KYC)

- Best economics (often lowest fees and best rates at this tier)

- Mobile pay and all integrations

Best For

- Everyday primary spending — using the card as your main payment method

- Higher-value purchases — travel, large purchases, business use

- Physical card users — tap-to-pay, ATM access

- Best value — full KYC typically unlocks the best fees and limits

Limitations

- Requires sharing full identity documents

- Slightly longer setup than lower tiers (though often still minutes)

Level 3 is for users who want a crypto card as a genuine everyday payment tool with no practical limits.

KYC Levels Comparison Table

| Feature | Level 1 | Level 2 | Level 3 |

|---|---|---|---|

| Verification | Email (± phone) | Phone + basic details | Gov ID + selfie + address |

| Setup time | Minutes | Minutes | Minutes (more docs) |

| Spending limits | Lowest | Moderate | Highest |

| Virtual card | Yes | Yes | Yes |

| Physical card | Usually no | Sometimes | Yes |

| Mobile pay | Sometimes | Often | Yes |

| Best for | Testing, small payments | Regular online spend | Everyday primary use |

What Triggers a Move to a Higher KYC Level?

Understanding what prompts an upgrade helps you plan.

Common triggers for higher verification:

- Requesting a physical card — physical cards almost always require full KYC (Level 3)

- Unlocking higher spending limits — the most common reason to upgrade

- Enabling mobile pay (Apple Pay / Google Pay) — sometimes requires Level 2+

- Higher transaction volumes — sustained higher spending may prompt verification

- Certain support actions — some account changes require identity confirmation

The smart strategy: Start at Level 1, use the card, and upgrade only when you hit a genuine need — a limit you want to exceed, a physical card, or mobile pay. There's no benefit to over-verifying before you need to, and no benefit to staying at Level 1 if your usage has grown beyond its limits.

A well-designed card makes upgrading seamless — a clear path from Level 1 to Level 3 with a defined verification step at each stage, rather than unexpectedly forcing full KYC without explanation.

How Custody Affects Your KYC Experience

A critical but often overlooked factor: whether your card is custodial or non-custodial.

Custodial Cards

The issuer holds your funds. You deposit crypto, and they manage it. This adds:

- Solvency risk (if the issuer fails, your funds may be at risk)

- Security risk (the issuer is a honeypot for hackers)

- More extensive data collection (they manage your money, so they verify more)

Non-Custodial Cards

You keep your funds in your own wallet. The card authorizes conversion only when you spend. This means:

- Your assets stay under your control regardless of KYC level

- Reduced custodial data exposure

- No issuer solvency risk to your held funds

- Regulators increasingly recommend self-custodial models

Why this matters for KYC: With a non-custodial card, KYC verification governs your card limits and features — but your funds remain in your wallet at every level. You're verifying to use the payment rails, not handing your assets to a custodian. This is the model GraphPay uses: your crypto stays yours, while KYC levels simply unlock higher card limits.

This combination — tiered KYC plus non-custodial architecture — gives you both regulatory compliance and self-custody, the approach regulators explicitly favor under frameworks like MiCA.

How GraphPay Handles KYC Levels

GraphPay is a non-custodial crypto card platform built around tiered KYC — combining compliance with self-custody.

The GraphPay approach:

- Tiered KYC (Level 1 → 2 → 3): Start with simplified verification and a virtual card; upgrade to unlock higher limits and physical cards as needed.

- Non-custodial: Your crypto stays in your own wallet (Web3 infrastructure). The card authorizes conversion only when you spend — your assets are never held by a third party.

- Multi-chain: Load from BNB Chain, Ethereum, or TRON using USDT or USDC.

- Major card networks: Cards run on Visa and Mastercard rails for global merchant acceptance.

- MiCA-aligned: Built for the compliant, self-custodial model regulators recommend ahead of the July 1, 2026 MiCA deadline.

Why the combination matters: Many cards force a choice — convenience with custodial risk, or self-custody with limited features. GraphPay's tiered KYC plus non-custodial architecture means you get graduated card limits (verify only as much as you need) while your funds stay under your control at every level.

Start at Level 1 to test, upgrade to Level 3 when you want a physical card and full limits — all while your crypto remains in your wallet.

How to Choose the Right KYC Level for You

Match the level to your actual needs:

Choose Level 1 if you:

- Want to test a crypto card before committing

- Make only occasional small online payments

- Prioritize minimal data sharing for low-value transactions

- Need a card immediately

Choose Level 2 if you:

- Spend regularly online beyond small payments

- Want mobile pay (Apple Pay / Google Pay)

- Need moderate limits but not maximum

- Want a balance of access and capability

Choose Level 3 if you:

- Want a crypto card as your everyday primary payment method

- Need a physical card for in-store and ATM use

- Make higher-value purchases (travel, large items, business)

- Want the best limits and economics

The practical path: Most users benefit from starting at Level 1, using the card to confirm it fits their needs, then upgrading toward Level 3 as their usage grows. With a non-custodial card, this progression happens while your funds stay in your wallet throughout.

Frequently Asked Questions

What are KYC levels on a crypto card? KYC levels are tiered identity verification stages. Level 1 (simplified) requires minimal verification (email, sometimes phone) with lower limits. Level 2 (standard) adds phone and basic details for moderate limits and more features. Level 3 (full) requires government ID, selfie, and proof of address for the highest limits and physical cards. Each level unlocks more capability.

Why do crypto cards require KYC at all? Three forces make KYC mandatory: FATF global AML rules requiring identity verification above thresholds, the EU's MiCA framework (fully mandatory by July 1, 2026), and Visa/Mastercard network requirements that issuing partners follow AML standards. Any card on major networks must verify identity — tiered KYC balances this with accessibility by scaling verification to transaction size.

Which KYC level do I need? Depends on your usage. Level 1 suits testing or occasional small online payments. Level 2 suits regular online spending and mobile pay. Level 3 suits everyday primary use, physical cards, and higher-value purchases. The smart approach: start at Level 1, then upgrade only when you need higher limits or a physical card.

What's the difference between custodial and non-custodial KYC cards? With custodial cards, the issuer holds your funds — adding solvency and security risk. With non-custodial cards (like GraphPay), your crypto stays in your own wallet, and the card authorizes conversion only when you spend. With non-custodial, KYC levels govern your card limits and features while your funds remain under your control at every level.

Can I upgrade my KYC level later? Yes. Well-designed cards offer a clear upgrade path from Level 1 to Level 3. You typically start with simplified verification and upgrade when you need higher limits, a physical card, or mobile pay. Common upgrade triggers include requesting a physical card, exceeding spending limits, or enabling Apple Pay / Google Pay.

Does a higher KYC level cost more? Usually the opposite — higher KYC levels often unlock better economics (lower fees, better rates) because full verification reduces the provider's risk. Lower tiers sometimes carry higher per-transaction costs to compensate for lighter verification. Full KYC (Level 3) typically offers the best limits AND the best value for regular spending.

Is tiered KYC the same as a "no-KYC" card? No. Tiered KYC is the legitimate, compliant model used by regulated issuers — you verify progressively to unlock more capability. "No-KYC" or "anonymous" cards operate in unregulated grey areas, carry serious risks (frozen funds, sudden shutdowns, no consumer protection), and have largely disappeared under 2026 regulations. Tiered KYC gives you fast Level 1 access within a compliant, sustainable framework.

About This Guide

This guide is published by the GraphPay Research team — building non-custodial crypto payment infrastructure. Our content is based on current regulatory frameworks, card industry practices, and 2026 market data.

Sources & data: KYC tier structures, regulatory frameworks (FATF, MiCA), and card network requirements reflect publicly available information as of 2026 and may change. Specific limits and requirements vary by provider and jurisdiction. This guide is educational and not financial or legal advice — always verify current terms with your card provider and consult local regulations.

GraphPay is non-custodial crypto payment infrastructure — your crypto, your pay. Learn more at graphpay.io.

Last reviewed: May 2026 · GraphPay Research