By GraphPay Research · Reviewed for accuracy May 2026

Quick Answer

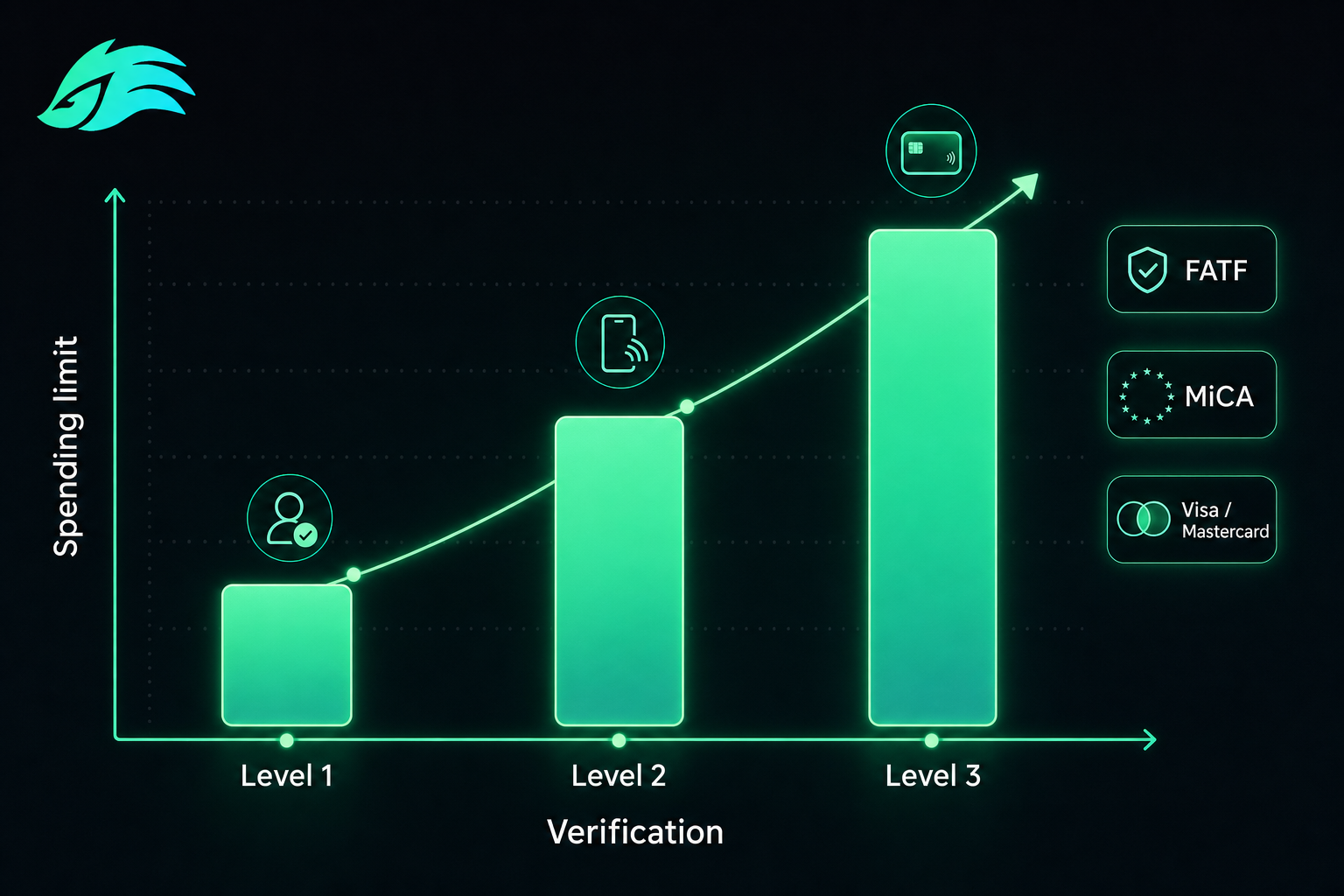

Crypto card limits scale with KYC verification level — each tier unlocks higher caps:

- Level 1 (Simplified): Lowest limits — suitable for small online payments and testing. Daily and monthly caps are conservative because verification is minimal.

- Level 2 (Standard): Moderate limits — enough for regular online spending and often mobile pay. Phone + basic verification unlocks higher caps.

- Level 3 (Full): Highest limits — suitable for everyday primary spending, travel, and larger purchases. Full ID verification removes most practical caps.

Why limits scale with verification: Regulations (FATF, MiCA) require identity verification proportional to transaction volume. Higher limits legally require more verification — so unlocking bigger caps means moving up KYC levels.

The smart approach: Match your level to your spending. If you hit Level 1 caps regularly, upgrade. With a non-custodial card like GraphPay, your funds stay in your wallet at every level — limits govern card usage, not custody.

Get a GraphPay card with flexible limits

Key Takeaways

- Crypto card limits scale with KYC level: Level 1 (lowest) → Level 2 (moderate) → Level 3 (highest).

- Limits scale with verification because regulations require ID checks proportional to transaction volume.

- Common limit types: per-transaction, daily, monthly, and sometimes lifetime caps.

- Match your level to your spending — upgrade when you regularly hit caps.

Why Do Crypto Card Limits Depend on KYC Level?

Crypto card limits aren't arbitrary — they're directly tied to verification level because of how financial regulation works.

The regulatory logic:

Global anti-money-laundering rules (set by FATF) require financial services to verify identity in proportion to transaction risk. Small transactions carry lower risk, so they can use lighter verification. Larger transactions carry higher risk, so they require more thorough identity checks.

This creates the tiered structure: a Level 1 card with minimal verification gets lower limits (the provider can only allow limited activity without knowing who you are), while a Level 3 card with full ID verification gets high limits (the provider has verified your identity and can allow more activity within compliance rules).

The frameworks driving this:

- FATF requires Virtual Asset Service Providers to collect identifying information above certain thresholds

- MiCA (mandatory for EU CASPs by July 1, 2026) requires identity verification for regulated services

- Visa/Mastercard require issuing partners to follow AML standards, including transaction monitoring

What this means for you: Your card's limits reflect how much you've verified. If you want higher limits, the path is upgrading your KYC level — not finding a workaround. This is the legitimate, compliant model, and it's why every regulated card uses tiered limits.

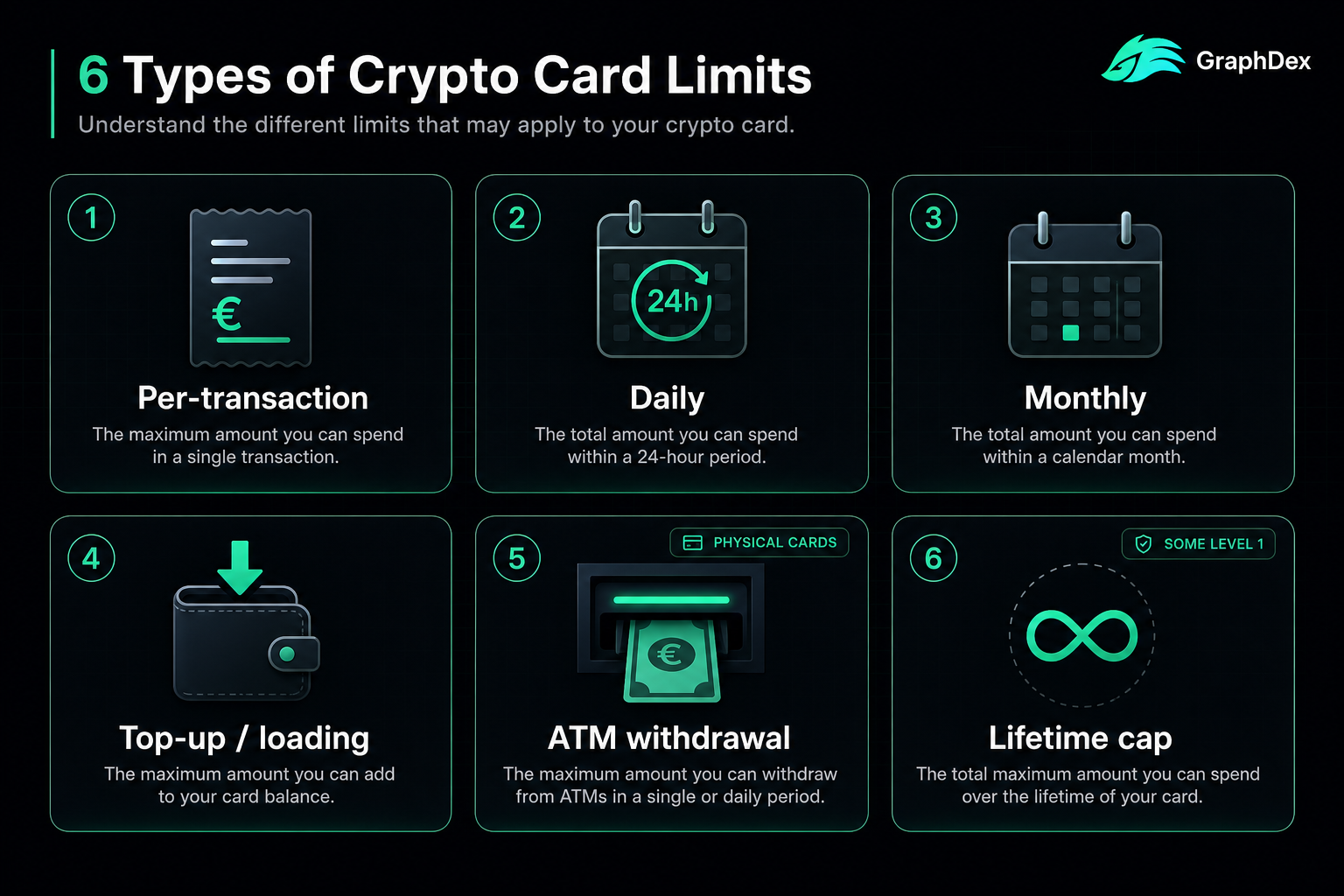

Types of Crypto Card Limits

Crypto cards typically apply several types of limits. Understanding each helps you choose the right level.

Per-Transaction Limit

The maximum amount you can spend in a single transaction. Lower at Level 1, higher at Level 3. Important for larger purchases (electronics, travel bookings) where a single transaction might exceed a low per-transaction cap.

Daily Limit

The maximum total you can spend in a 24-hour period. Affects days with multiple purchases or a few large ones. Scales up with verification level.

Monthly Limit

The maximum total spending per month — often the most relevant limit for everyday use. A Level 1 monthly cap might cover subscriptions; a Level 3 monthly cap can cover your entire monthly spending.

Top-Up / Loading Limit

The maximum crypto you can load (or, for non-custodial cards, the spending power your connected wallet enables) within a period. Scales with level.

ATM Withdrawal Limit (Physical Cards)

For Level 3 physical cards, the maximum cash withdrawal per transaction or day. Subject to both the card's limits and ATM operator limits.

Lifetime Limit (Some Lower Tiers)

Some Level 1 cards apply a lifetime cap — a total amount spendable before mandatory upgrade. This ensures compliance for minimally-verified accounts. Upgrading removes it.

The key takeaway: When evaluating a card, check all relevant limit types for your intended use — not just the headline monthly figure. A card with a high monthly limit but a low per-transaction cap might still block a large purchase.

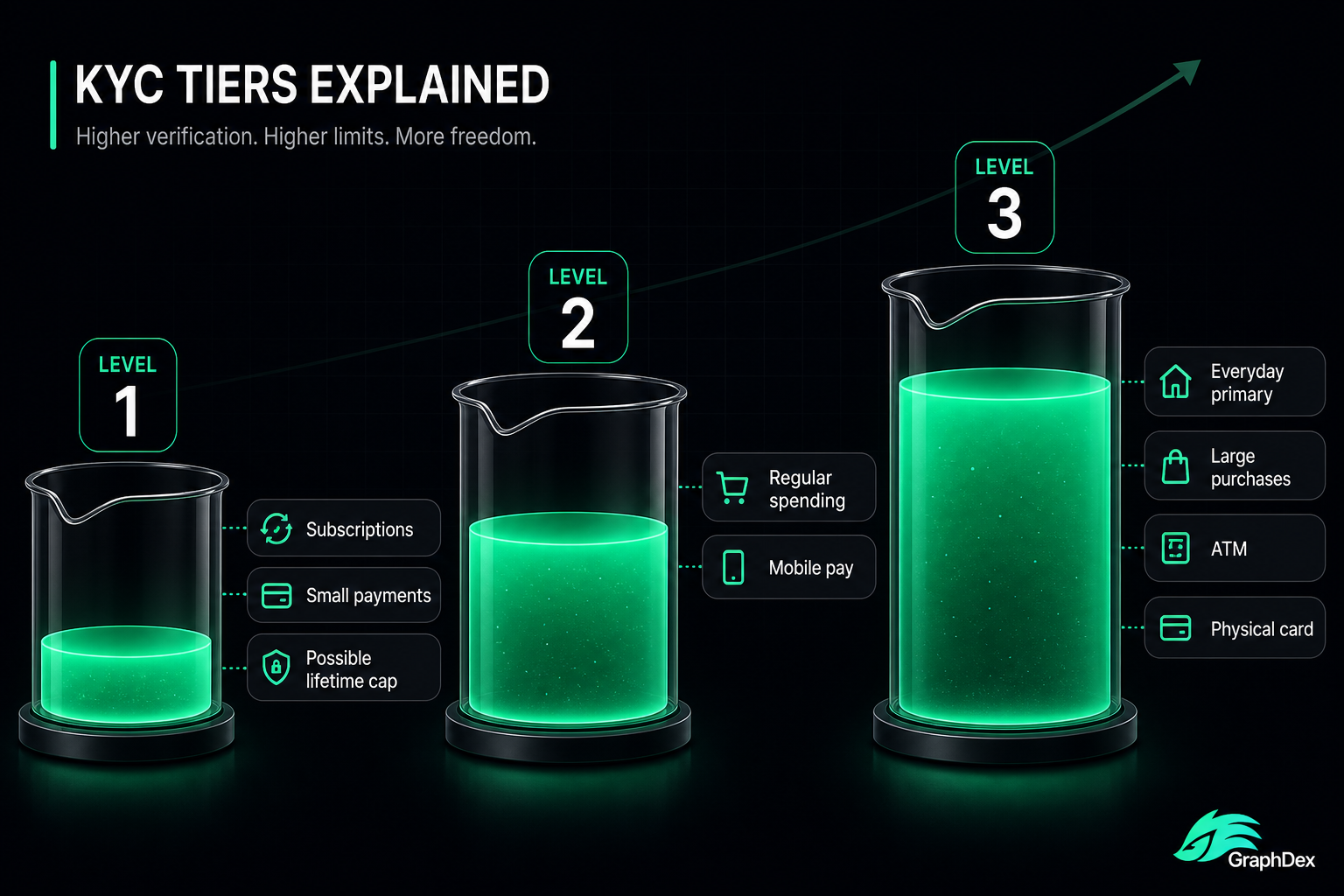

Limits at KYC Level 1 (Simplified)

The entry tier — designed for accessibility, with conservative limits.

Typical characteristics:

- Lowest per-transaction, daily, and monthly limits of the three tiers

- Sometimes a lifetime cap that triggers a required upgrade

- Conservative because verification is minimal (often just email/phone)

What Level 1 limits comfortably cover:

- Streaming and software subscriptions

- Small online purchases

- Digital services and apps

- Testing the card before fuller commitment

- Occasional low-value spending

What Level 1 limits may NOT cover:

- Large single purchases (electronics, travel)

- High monthly spending (using the card as your primary payment method)

- Significant ATM withdrawals (often not available at Level 1 anyway, since physical cards usually require Level 3)

Who Level 1 suits: Users testing a card, those making only occasional small payments, and privacy-conscious users keeping low-value activity light on verification. If you find yourself regularly hitting Level 1 caps, it's a clear signal to upgrade.

Limits at KYC Level 2 (Standard)

The middle tier — meaningfully higher limits with still-light verification.

Typical characteristics:

- Moderate per-transaction, daily, and monthly limits (higher than Level 1)

- Often unlocks mobile pay (Apple Pay / Google Pay)

- Requires phone verification plus basic identity details

What Level 2 limits comfortably cover:

- Regular online shopping

- Most everyday digital spending

- Moderate single purchases

- Mobile pay transactions

What Level 2 limits may NOT fully cover:

- Very large single purchases

- High-volume monthly spending as a primary card

- Physical card use (often still requires Level 3)

Who Level 2 suits: Users who've outgrown Level 1 but don't yet need maximum limits or a physical card. It's a practical middle ground — enough capacity for regular spending without full document verification.

Limits at KYC Level 3 (Full)

The top tier — highest limits and full feature access.

Typical characteristics:

- Highest per-transaction, daily, and monthly limits — often dramatically higher than lower tiers

- Physical card eligibility (with ATM withdrawal limits)

- Best economics (often lowest fees and best rates)

- Requires full verification: government ID, selfie, proof of address

What Level 3 limits cover:

- Everyday primary spending — use the card as your main payment method

- Large single purchases (electronics, travel, business expenses)

- High monthly spending volumes

- ATM withdrawals (physical card)

- Essentially unrestricted normal use for most individuals

Who Level 3 suits: Anyone using a crypto card as a genuine everyday payment tool. The full verification unlocks limits high enough that most users never hit them in normal use, plus physical card access for in-store and ATM use.

The value trade-off: Level 3 requires sharing full identity documents, but in return unlocks the highest limits AND typically the best economics (lowest fees, best conversion rates). For regular users, this trade-off strongly favors Level 3.

Limits Comparison Table

| Limit Type | Level 1 | Level 2 | Level 3 |

|---|---|---|---|

| Per-transaction | Lowest | Moderate | Highest |

| Daily limit | Lowest | Moderate | Highest |

| Monthly limit | Conservative | Moderate | Highest |

| Lifetime cap | Sometimes applies | Rarely | No |

| Physical card | Usually no | Sometimes | Yes |

| ATM withdrawals | Usually no | Sometimes | Yes |

| Best for | Small payments | Regular spending | Everyday primary use |

Exact figures vary by provider and jurisdiction. The pattern — limits scaling up with verification — is universal.

How to Choose the Right Level for Your Spending

Match your KYC level to your actual spending needs:

Estimate your monthly crypto card spending:

-

Under a few hundred per month, occasional small payments: Level 1 likely covers you. Test it; upgrade if you hit caps.

-

Regular monthly spending, want mobile pay: Level 2 offers the capacity and features for everyday online use.

-

Using the card as your primary payment method, want a physical card, or make large purchases: Level 3 removes practical limits and unlocks physical use.

Watch for these upgrade signals:

- You're regularly hitting your monthly cap

- A purchase was declined for exceeding a per-transaction limit

- You want a physical card for in-store use

- You want ATM access

- You want mobile pay (if your current level doesn't support it)

- You want the best fees and rates (Level 3 economics)

The practical strategy: Start at the level matching your current needs (often Level 1 to test), then upgrade when you hit a genuine limit. There's no benefit to over-verifying before you need to — and no benefit to suffering low caps when your usage has grown. A card with flexible tiers makes this progression seamless.

Get a GraphPay card and upgrade as you grow

How Custody Interacts With Limits

An important nuance: with non-custodial cards, limits work differently than you might expect.

With custodial cards: You load funds to the issuer, and limits cap how much you can load and spend. Your funds sit in the issuer's custody up to the loaded amount.

With non-custodial cards (like GraphPay): Your crypto stays in your own wallet. KYC-level limits govern how much you can spend through the card (per transaction, daily, monthly) — but your funds never leave your wallet until the moment you spend. The limits control card usage; they don't require parking funds in someone else's custody.

Why this matters: With a non-custodial card, hitting a limit doesn't mean your funds are stuck somewhere — they're always in your wallet. Upgrading your KYC level raises your spending limits while your custody arrangement (funds in your wallet) stays the same. You get higher capacity without ever surrendering control of your assets.

This combination — tiered limits plus non-custodial architecture — means you control both how much you verify (KYC level) and where your funds live (your wallet).

How GraphPay Handles Limits Across Levels

GraphPay scales limits across KYC levels while keeping your funds non-custodial throughout.

The GraphPay model:

- Level 1: Virtual card with conservative limits — ideal for testing and small payments, minimal verification

- Level 2: Standard verification unlocks higher limits and more features

- Level 3: Full verification unlocks the highest limits, physical card, and best economics

Throughout every level:

- Non-custodial: Your crypto stays in your own wallet — limits govern card spending, not custody

- Multi-chain: Spending power from BNB Chain, Ethereum, or TRON (USDT, USDC)

- Visa & Mastercard: Global merchant acceptance

- Seamless upgrades: Move from Level 1 to Level 3 as your spending grows

The advantage: You start with a quick Level 1 card, upgrade to higher limits as your usage grows, and your funds stay in your wallet at every step. Limits scale with your verification; custody never changes. You're always in control.

Frequently Asked Questions

How do crypto card limits work by KYC level? Limits scale with verification: Level 1 (simplified) has the lowest limits, Level 2 (standard) moderate, Level 3 (full) the highest. This is because regulations (FATF, MiCA) require identity verification proportional to transaction volume — higher limits legally require more verification. Common limit types include per-transaction, daily, monthly, and sometimes lifetime caps.

Why are Level 1 crypto card limits so low? Because Level 1 requires minimal verification (often just email/phone), regulations only permit limited activity. Without full identity verification, providers must keep caps conservative to stay compliant with AML rules. Level 1 limits comfortably cover subscriptions and small payments; for higher limits, you upgrade to Level 2 or Level 3 by completing more verification.

How do I increase my crypto card limit? Upgrade your KYC level. Moving from Level 1 to Level 2 (phone + basic details) raises limits and often unlocks mobile pay. Moving to Level 3 (government ID, selfie, proof of address) unlocks the highest limits and physical cards. There's no compliant way to get high limits without verification — upgrading your level is the legitimate path.

What's the highest limit a crypto card offers? Level 3 (full KYC) offers the highest limits — often high enough that typical individuals never hit them in normal use. Exact figures vary by provider and jurisdiction. Level 3 also unlocks physical cards with ATM withdrawal limits. For everyday primary spending and large purchases, Level 3 is the tier that removes practical caps.

Do non-custodial cards have spending limits? Yes — non-custodial cards still apply KYC-level limits (per transaction, daily, monthly) for regulatory compliance. The difference is that your funds stay in your own wallet rather than the issuer's custody. Limits govern how much you can spend through the card; they don't require parking funds with a third party. Upgrading your level raises limits while custody stays with you.

What happens if I hit my crypto card limit? The card will decline transactions that exceed your limit until the limit period resets (daily limits reset each day, monthly limits each month) or you upgrade your KYC level. With a non-custodial card, hitting a limit doesn't lock up your funds — they remain in your wallet. To avoid declines, match your KYC level to your spending or upgrade when you regularly hit caps.

Which KYC level do I need for my spending? Estimate your monthly crypto card spending. Occasional small payments: Level 1. Regular online spending with mobile pay: Level 2. Primary payment method, physical card, or large purchases: Level 3. Start at the level matching your current needs and upgrade when you hit genuine limits — flexible-tier cards make this seamless.

About This Guide

This guide is published by the GraphPay Research team — building non-custodial crypto payment infrastructure. Our content is based on current card industry practices, regulatory frameworks, and 2026 market data.

Sources & data: Limit structures and regulatory frameworks reflect publicly available information as of 2026 and may change. Exact limit figures vary by provider and jurisdiction. This guide is educational and not financial or legal advice — always verify current limits with your provider and consult local regulations.

GraphPay is non-custodial crypto payment infrastructure — your crypto, your pay. Learn more at graphpay.io.

Last reviewed: May 2026 · GraphPay Research