By GraphPay Research · Reviewed for accuracy May 2026

Quick Answer

In many jurisdictions, spending crypto on a card can be a taxable event — here's the general picture:

- Why it's taxable: Spending crypto (including via a card) often counts as "disposing" of the asset, which can trigger capital gains tax on any appreciation since you acquired it

- Spending appreciated crypto: If your crypto gained value, spending it may realize a taxable gain

- Spending stablecoins: Because stablecoins hold a steady value, spending them typically generates little or no taxable gain — a key advantage

- Records matter: You generally need to track your cost basis (what you paid) and the value when spent, to calculate any gain

The critical caveat: Tax treatment varies enormously by jurisdiction and changes over time. This guide gives the general picture only — it is NOT tax advice. Always consult a qualified tax professional about your specific situation and local rules.

The practical tip: Spending stablecoins (USDT/USDC) rather than volatile crypto minimizes taxable gains, since stablecoins barely change in value. Many users spend stablecoins on their card for this reason.

Spend stablecoins with a GraphPay card

Key Takeaways

- In many jurisdictions, spending crypto on a card can be a taxable event (disposing of the asset).

- Spending appreciated crypto may realize a capital gain; spending stablecoins typically minimizes this.

- You generally need to track cost basis and value-when-spent to calculate any gain.

- Tax rules vary by jurisdiction and change — this is general information, not tax advice. Consult a professional.

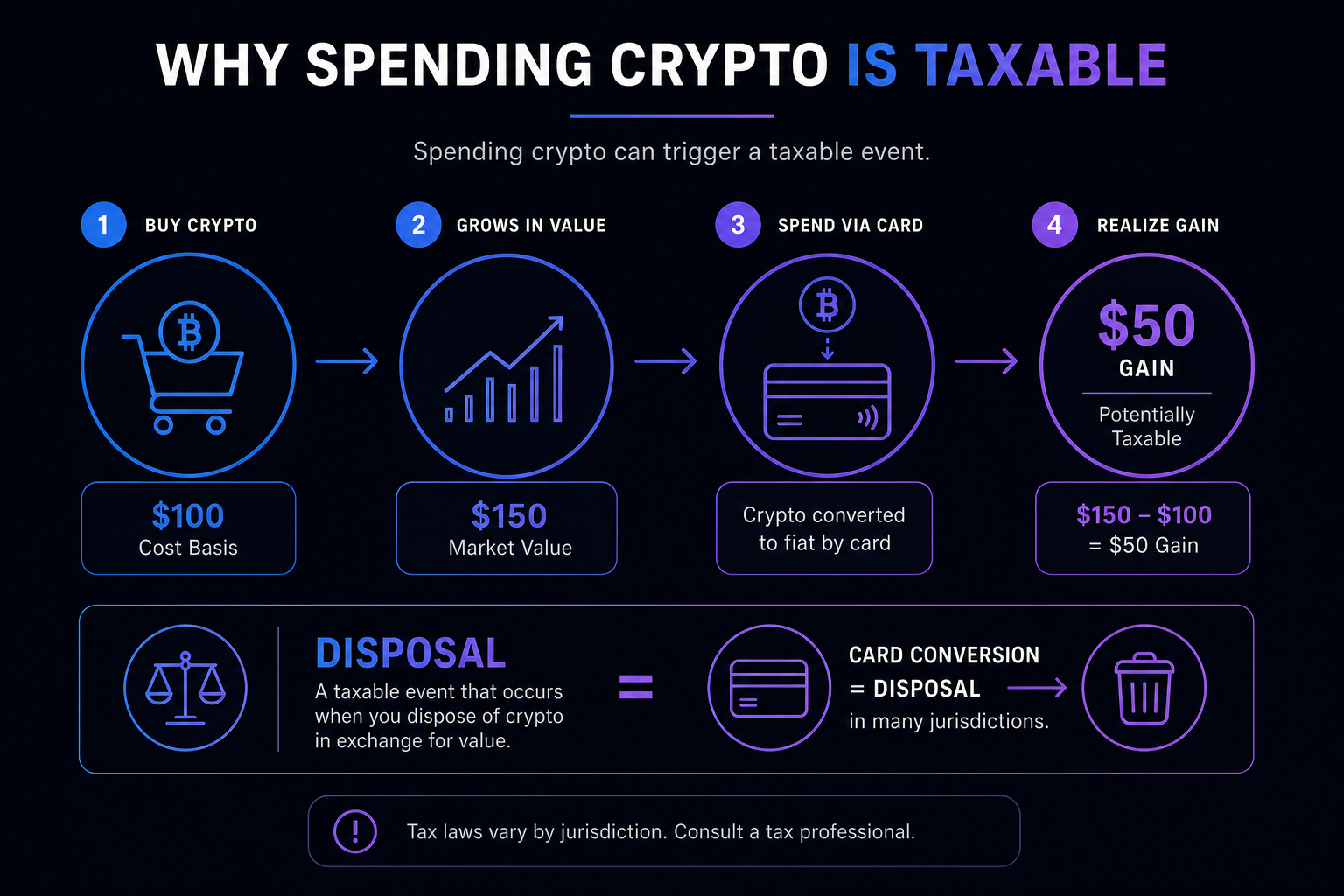

Why Spending Crypto Can Be Taxable

A common misconception is that spending crypto — rather than selling it on an exchange — avoids tax. In reality, many tax authorities treat spending crypto the same as selling it.

The core concept — "disposal": In many jurisdictions, tax rules treat spending crypto as "disposing" of an asset. When you dispose of crypto (whether by selling it for fiat, trading it for another crypto, or spending it on goods/services), you may realize a capital gain or loss based on how its value changed since you acquired it.

How it applies to cards: When you spend crypto via a card, the crypto is converted to fiat at the point of sale. From a tax perspective, this conversion is often treated as a disposal — the same as if you'd sold the crypto. So even though the user experience is "just spending," the tax treatment may be "selling."

What triggers a gain:

- You acquired crypto at one value (your "cost basis")

- The crypto's value rose by the time you spent it

- Spending it "realizes" that gain — the difference between what you paid and its value when spent

- This gain may be subject to capital gains tax

A simple illustration:

- You bought crypto worth $100

- Later, it's worth $150

- You spend it via your card (buying something for $150)

- You may have realized a $50 gain, potentially taxable

Why this surprises people: The card makes spending feel seamless — like using any debit card. But behind the scenes, the crypto-to-fiat conversion can be a taxable disposal. Understanding this prevents an unexpected tax situation.

The important nuance: This is the general concept in many jurisdictions. The specifics — rates, thresholds, exemptions, and whether this even applies — vary enormously by country. Always verify your local rules with a professional.

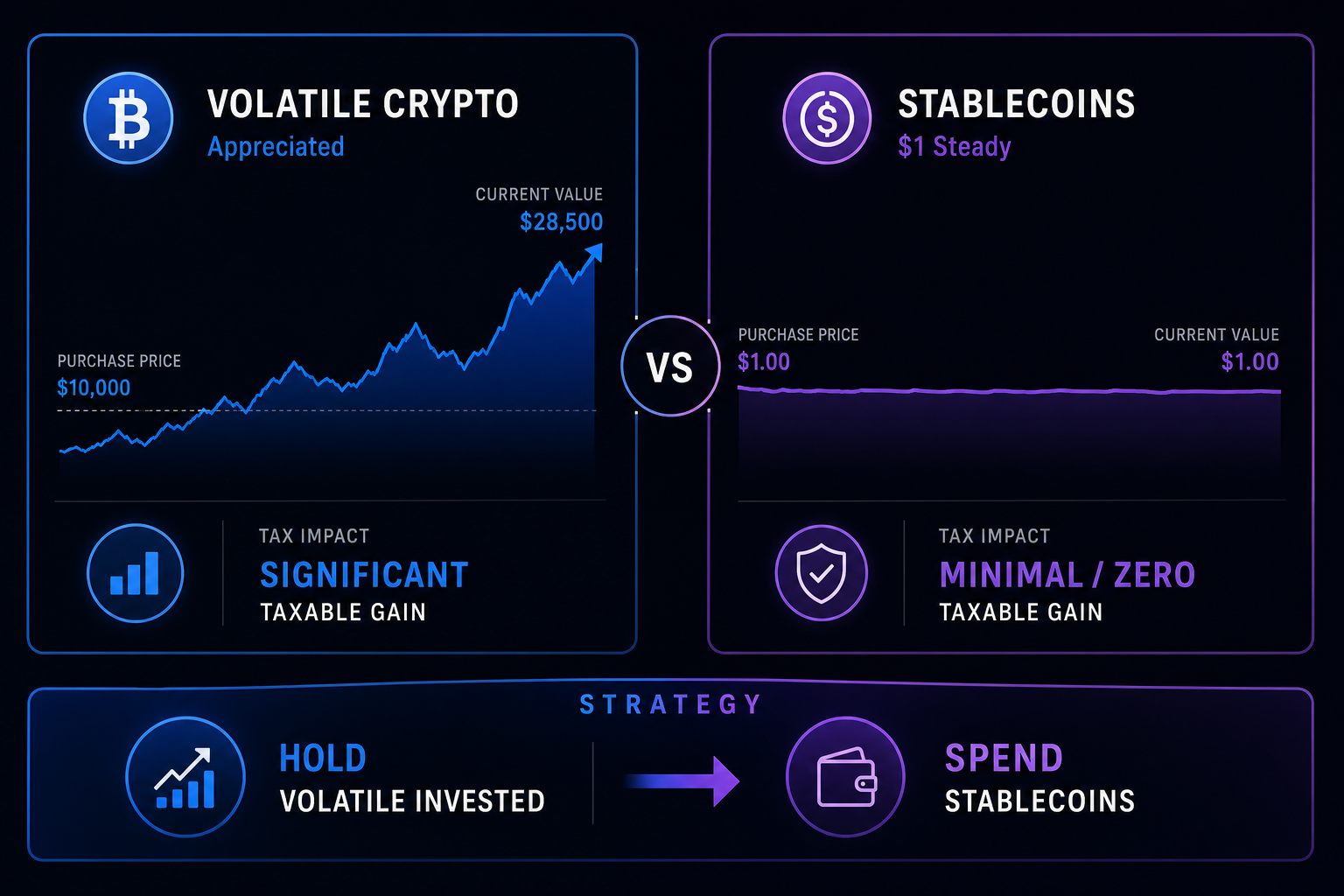

Why Spending Stablecoins Minimizes Tax

A key insight: spending stablecoins rather than volatile crypto can largely sidestep the taxable-gain issue.

The logic: Capital gains tax applies to the change in value between acquiring and spending an asset. Stablecoins (USDT, USDC) are designed to hold a steady $1 value — so there's little or no change in value to tax.

How it works:

- You hold stablecoins worth $100 (each ≈ $1)

- You spend them via your card (still ≈ $1 each)

- Because their value barely changed, there's little or no gain to realize

- The taxable gain is minimal or zero

Contrast with volatile crypto:

- Spending appreciated Bitcoin: may realize a significant taxable gain

- Spending stablecoins: minimal or no gain, since value is stable

The strategic approach many users take:

- Hold volatile crypto (BTC, ETH, SOL) for potential appreciation — don't spend it directly

- Spend stablecoins (USDT, USDC) on the card — minimal taxable gains

- This keeps volatile assets invested while spending stable value with minimal tax friction

The caveat: Even spending stablecoins may have some tax implications depending on your jurisdiction (e.g., if you acquired the stablecoin at a slightly different value, or if local rules treat it differently). And converting volatile crypto to stablecoins is itself a disposal that may be taxable. Stablecoins minimize but don't necessarily eliminate all tax considerations. Consult a professional.

The practical takeaway: For minimizing crypto card tax friction, spending stablecoins (which hold steady value) rather than appreciated volatile crypto is a common, sensible approach. It's a major reason many crypto card users fund with and spend stablecoins.

What Records to Keep

Because spending crypto can be taxable, keeping good records is essential for calculating and reporting any gains.

What you generally need to track:

Cost basis. What you paid for the crypto (the acquisition value). This is the starting point for calculating any gain.

Acquisition date. When you acquired the crypto — relevant because some jurisdictions tax short-term and long-term gains differently.

Value when spent. The crypto's value at the moment you spent it via the card — this, minus cost basis, determines the gain.

Transaction records. Records of each card transaction — date, amount, and the crypto spent.

Why records matter:

- To calculate gains accurately (value when spent minus cost basis)

- To report correctly to tax authorities

- To substantiate your calculations if questioned

- To distinguish gains from non-taxable amounts

How to keep records:

- Many crypto card apps provide transaction history

- Crypto tax software can help track cost basis and calculate gains

- Keep records of when and at what value you acquired crypto

- Maintain a consistent system throughout the year

The stablecoin simplification: If you spend primarily stablecoins (minimal gains), record-keeping is simpler — there's little gain to calculate. This is another advantage of spending stablecoins. But still keep records, as you may need to substantiate that gains were minimal.

Spend stablecoins with GraphPay

The professional's role: A tax professional or crypto tax software can help you track cost basis, calculate gains, and report correctly. Given the complexity, especially with volatile crypto, professional help is often worthwhile.

Important: Tax Rules Vary — This Isn't Tax Advice

The most important section of this guide: a clear statement of its limits.

Tax treatment of crypto varies enormously:

- By jurisdiction: Different countries have vastly different crypto tax rules. Some tax crypto spending as capital gains; some have specific crypto rules; some have exemptions or thresholds; a few have no capital gains tax at all.

- By situation: Your specific circumstances (holding period, amounts, income level, local exemptions) affect your tax treatment.

- Over time: Crypto tax rules are actively evolving. What's true today may change.

What this guide is and isn't:

- Is: A general overview of the common concept that spending crypto can be a taxable disposal in many jurisdictions, and that spending stablecoins can minimize this

- Is NOT: Tax advice for your situation, a statement of your local rules, or a substitute for professional guidance

What you should do:

- Consult a qualified tax professional about your specific situation and local rules

- Use crypto tax software to help track and calculate

- Verify your local regulations — they may differ significantly from the general concept

- Keep good records regardless, so you're prepared

The honest bottom line: Spending crypto on a card may be taxable in your jurisdiction, but the specifics depend entirely on where you are and your situation. This guide can't tell you your tax obligations — only a professional familiar with your local rules can. Take the general concept here as a prompt to investigate your specific situation, not as definitive guidance.

How GraphPay Fits (With the Tax Caveat)

GraphPay is a non-custodial crypto card that supports stablecoin spending — which can help minimize tax friction — but your tax obligations depend on your jurisdiction and situation.

How GraphPay relates to the tax picture:

- Stablecoin support: Spend USDT or USDC — stablecoins that hold steady value, minimizing taxable gains compared to spending appreciated volatile crypto

- Non-custodial: Your crypto stays in your wallet; the card converts only what you spend — but note that this conversion may still be a taxable disposal in your jurisdiction

- Transaction records: Card transaction history can help with your record-keeping

- Multi-chain: Fund from BNB Chain, Ethereum, or TRON with USDT/USDC

The honest positioning: GraphPay's support for stablecoin spending aligns with the common tax-minimizing approach (spend stable value, keep volatile crypto invested). But GraphPay can't change your tax obligations — spending crypto may still be taxable depending on your jurisdiction. The card affects convenience and custody, not your underlying tax situation.

What GraphPay can't do: Provide tax advice or determine your obligations. For that, consult a qualified tax professional familiar with your local rules.

The practical use: Many users spend stablecoins (USDT/USDC) via GraphPay for predictable value and minimal taxable gains, while keeping volatile crypto invested. But always verify your local tax treatment and keep records — GraphPay facilitates spending, not tax compliance.

Spend stablecoins with a non-custodial GraphPay card

Frequently Asked Questions

Do you pay tax when spending crypto on a card? In many jurisdictions, potentially yes. Spending crypto (including via a card) often counts as "disposing" of the asset, which can trigger capital gains tax on any appreciation since you acquired it. The card converts crypto to fiat at purchase, and this conversion may be treated as a disposal — the same as selling. However, tax rules vary enormously by jurisdiction. This is general information, not tax advice — consult a professional.

Is spending crypto a taxable event? In many jurisdictions, spending crypto is treated as disposing of an asset, potentially realizing a capital gain or loss based on how its value changed since acquisition. This applies whether you sell it, trade it, or spend it on goods/services (including via a card). But the specifics vary by jurisdiction — some tax it, some have exemptions, some have no capital gains tax. Verify your local rules with a professional.

How can I minimize tax when spending crypto? A common approach: spend stablecoins (USDT/USDC) rather than appreciated volatile crypto. Because stablecoins hold a steady value, spending them typically generates little or no taxable gain (there's minimal value change to tax). Many users keep volatile crypto (BTC, ETH) invested for upside and spend stablecoins on their card. However, tax treatment varies — consult a professional about your situation.

Do I pay tax spending stablecoins on a card? Generally minimal, because stablecoins hold a steady value — so there's little or no gain to realize when spending them. This is a key advantage over spending appreciated volatile crypto. However, some tax considerations may still apply depending on your jurisdiction, and converting volatile crypto to stablecoins is itself a potentially taxable disposal. Stablecoins minimize but may not eliminate tax considerations. Consult a professional.

What records do I need for crypto card taxes? Generally: your cost basis (what you paid for the crypto), acquisition date (when you got it), value when spent (at the point of card purchase), and transaction records. These let you calculate any gain (value when spent minus cost basis). Many crypto card apps provide transaction history, and crypto tax software can help track and calculate. If you spend mainly stablecoins, record-keeping is simpler (minimal gains).

Does using a crypto card avoid crypto taxes? No — using a card doesn't avoid taxes. The card makes spending feel seamless (like a debit card), but behind the scenes, the crypto-to-fiat conversion may be a taxable disposal in your jurisdiction, the same as selling. "Spending without selling" refers to the user experience, not tax treatment. The card affects convenience, not your tax obligations. Verify your local rules and consult a professional.

Is this guide tax advice? No. This guide provides a general overview of the common concept that spending crypto can be taxable in many jurisdictions, but it is NOT tax advice for your situation. Tax treatment varies enormously by jurisdiction and circumstances, and rules change over time. Always consult a qualified tax professional familiar with your local rules, and consider using crypto tax software. Take this as a prompt to investigate your specific situation, not definitive guidance.

About This Guide

This guide is published by the GraphPay Research team — building non-custodial crypto payment infrastructure. Our content is based on general tax concepts and 2026 market data.

Sources & data: Tax concepts reflect general principles in many jurisdictions as of 2026 and may not apply to your situation. Tax treatment of crypto varies enormously by jurisdiction and changes over time. This guide is educational and is NOT tax, financial, or legal advice. Always consult a qualified tax professional about your specific situation and local rules, and consider crypto tax software for tracking and calculations.

GraphPay is non-custodial crypto payment infrastructure — your crypto, your pay. Learn more at graphpay.io.

Last reviewed: May 2026 · GraphPay Research