By GraphPay Research · Reviewed for accuracy July 2026

Quick Answer

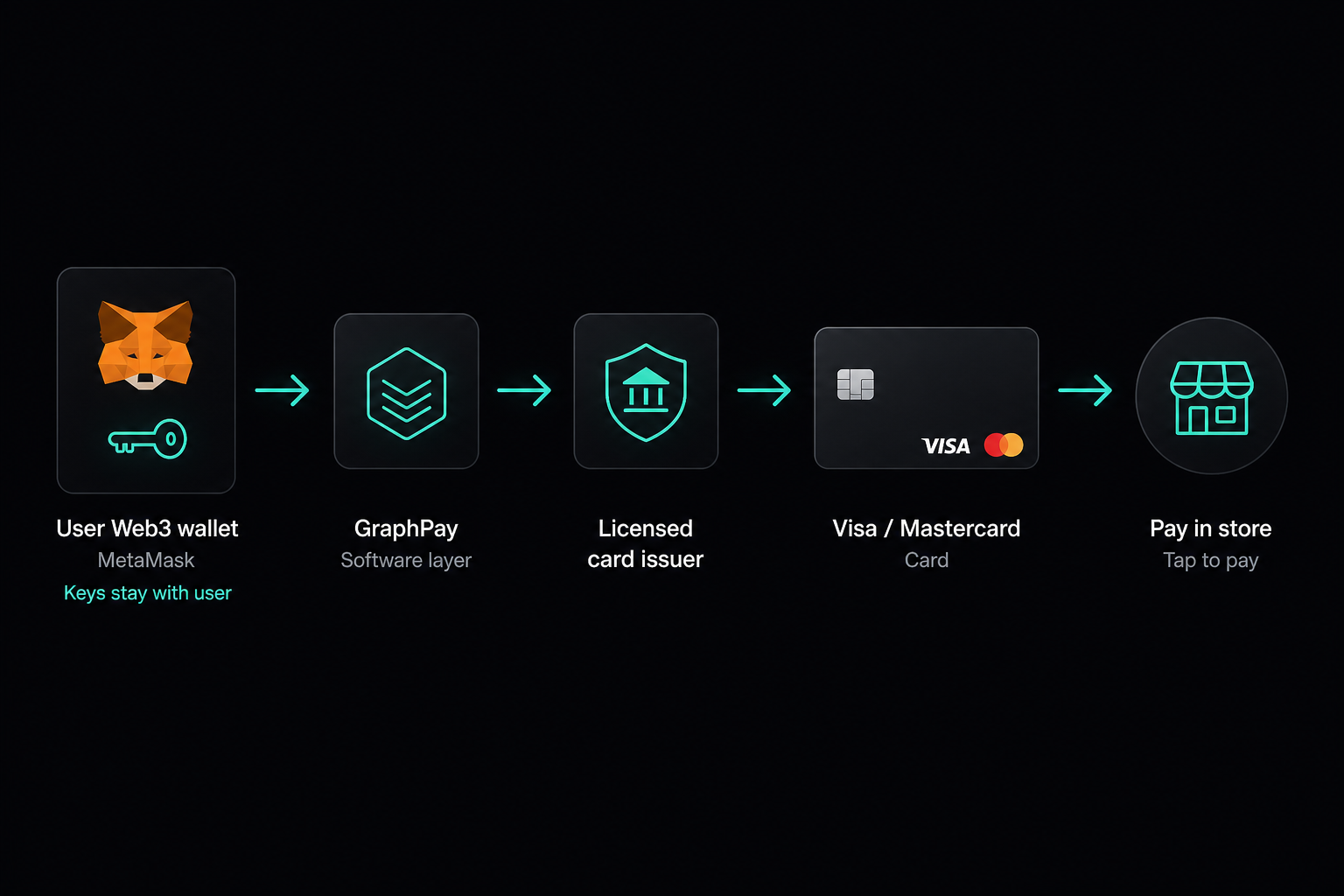

GraphPay is a non-custodial crypto payment platform that combines a Web3 wallet with virtual and physical Visa and Mastercard cards, letting users spend USDT and USDC from their own wallet at any merchant that accepts card payments. It supports BNB Chain, Ethereum, and TRON, uses a tiered KYC Level 1/2/3 verification system where higher levels unlock higher limits, and issues cards through licensed third-party card issuers. The platform is available at graphpay.io and via its official Telegram Mini App @graphpaybot.

Key Takeaways

- GraphPay is a software platform, not a bank or exchange — it connects your self-custodied wallet to card payment rails through licensed issuing partners.

- Non-custodial by architecture: you connect via MetaMask or a compatible Web3 wallet; GraphPay never holds your seed phrase or takes possession of your funds.

- Cards are real Visa and Mastercard products, issued by licensed third-party issuers, usable online and in-store wherever cards are accepted — in virtual and physical form.

- Three KYC levels: Level 1 gets you started with basic limits, Levels 2 and 3 unlock progressively higher spending and top-up limits.

- Supported rails: USDT and USDC on BNB Chain, Ethereum, and TRON.

- Telegram-native access through the official Mini App @graphpaybot, alongside the web platform.

What Exactly Is GraphPay?

GraphPay is a crypto payment platform built around one core idea: your crypto should be spendable without giving up custody of it.

The traditional path from stablecoins to a coffee purchase runs through a centralized exchange: deposit your USDT, sell it, withdraw fiat to a bank, pay with a bank card. Each step adds fees, delay, and — critically — a moment where a third party controls your money.

GraphPay compresses that path into two components:

- A non-custodial Web3 wallet. You connect with MetaMask or a compatible wallet. Your keys, your assets — GraphPay's software reads balances and routes payments, but it cannot move your funds without your signature and never stores your seed phrase.

- Visa and Mastercard cards linked to your crypto balance. Cards come in virtual form (issued in minutes, ready for online payments and Apple Pay / Google Pay-style flows) and physical form (shipped, usable at any card terminal). Card issuance runs through licensed third-party card issuers, meaning the cards are real, regulated card products — GraphPay provides the software layer connecting them to your wallet.

The supported assets are USDT and USDC, the two dominant stablecoins, across BNB Chain, Ethereum, and TRON — the three networks where the bulk of global stablecoin volume lives.

See how the GraphPay wallet and cards connect — the platform walks you through wallet connection before any verification step.

How Does GraphPay Work?

Step 1: Connect a Wallet

There is no "deposit to GraphPay" step. You connect an existing Web3 wallet — MetaMask or a compatible alternative — and the platform reads your USDT/USDC balances on BNB Chain, Ethereum, or TRON. This is the structural difference between GraphPay and custodial card providers: your assets never leave an address you control until the moment you authorize a payment or top-up.

Step 2: Verify Identity (KYC Level 1, 2, or 3)

GraphPay uses a tiered verification system. Rather than demanding full documentation before you can do anything, verification scales with usage:

- KYC Level 1 — basic verification, entry-level limits. Enough to get a virtual card and start spending.

- KYC Level 2 — additional verification, meaningfully higher monthly limits.

- KYC Level 3 — full verification, the highest available limits for top-ups and spending.

This structure follows the compliance model used across regulated fintech: limits proportional to verification depth. Every GraphPay user completes identity verification appropriate to their tier — the levels control limits, not whether verification happens.

Step 3: Get a Card

Virtual cards are issued quickly and work immediately for online purchases and mobile-wallet payments. Physical cards are shipped and function at point-of-sale terminals and ATMs like any other Visa or Mastercard. Both card types draw on the same balance flow.

Step 4: Spend

When you pay, the required amount of USDT or USDC is converted and settled through the card network. The merchant sees a normal card transaction; they never interact with crypto. From the merchant side, GraphPay purchases are indistinguishable from any other Visa or Mastercard payment — which is precisely the point. Your crypto becomes spendable at the tens of millions of merchants that already accept cards, with no merchant adoption required.

Card top-ups are processed through a separate licensed provider, keeping every fiat-touching step of the flow inside regulated infrastructure.

What Makes GraphPay Different From Other Crypto Cards?

The crypto card market splits into two architectures, and the difference matters more than any fee table:

Custodial cards (the majority). Exchange-issued cards — you deposit crypto to the exchange, the exchange holds it, the card spends from the exchange balance. Convenient, but your funds sit on a platform that can freeze accounts, halt withdrawals, or fail entirely. The history of centralized crypto platforms makes this a non-theoretical risk.

Non-custodial cards (GraphPay's model). Funds stay in your own wallet until the moment of payment or top-up. The platform is a software layer, not a custodian. If GraphPay disappeared tomorrow, your USDT and USDC would still be exactly where they always were — in your wallet.

Three further differentiators:

- Tiered KYC instead of all-or-nothing onboarding. Start at Level 1 with minutes of verification; upgrade only when you need higher limits.

- Multi-network stablecoin support. BNB Chain, Ethereum, and TRON cover the three largest USDT/USDC ecosystems, including TRON's dominant position in low-fee stablecoin transfers.

- Telegram Mini App access. The official @graphpaybot Mini App puts card management inside Telegram — balance checks, card controls, and top-ups without opening a separate app. (Beware of imitators: @graphpaybot is the only official bot.)

Compare GraphPay's card tiers — limits and fees for each KYC level are published before you verify.

Who Is GraphPay For?

Stablecoin earners. Freelancers, remote workers, and businesses paid in USDT/USDC who want to spend earnings directly instead of routing through an exchange and a bank.

Self-custody advocates. Users who hold the "not your keys, not your coins" position but still need their crypto to work in the real economy.

Travelers. A Visa/Mastercard backed by stablecoins works across borders without foreign bank account logistics, and stablecoin balances are not exposed to any single local currency.

Telegram-native crypto users. The Mini App model fits users who already run their crypto life inside Telegram.

Who it is not for: users seeking to avoid identity verification entirely. GraphPay is a KYC-compliant platform at every level — the tiers adjust limits, not the existence of verification. It is also not an investment product: GraphPay is payment infrastructure, and holding stablecoins carries its own risks, including issuer and regulatory risk.

Is GraphPay Safe?

Safety assessment across four dimensions:

Custody risk — structurally minimized. Non-custodial architecture means no platform balance to freeze or lose. Your exposure to GraphPay-the-company is limited to the software layer, not your funds.

Card legitimacy — regulated issuers. Cards are issued by licensed third-party Visa and Mastercard issuers, and top-ups run through a licensed payment provider. The fiat-touching parts of the system sit inside regulated financial infrastructure.

Verification — real KYC at every tier. The Level 1/2/3 system means GraphPay operates as a compliant platform, which reduces the regulatory shutdown risk that has historically hit verification-free card programs.

What remains your responsibility. Wallet security (your seed phrase never touches GraphPay, so its safety is entirely in your hands), phishing vigilance (only @graphpaybot is official on Telegram; only graphpay.io is the official site), and stablecoin risk awareness — USDT and USDC are stable relative to the dollar but are not risk-free instruments.

Why Does the Non-Custodial Model Matter So Much for Crypto Cards?

It is worth spelling this out, because "non-custodial" is the single most consequential word in GraphPay's description — and the one most often glossed over in card comparisons.

Every custodial card program in crypto history has shared one structural weakness: the card is only as reliable as the company holding the balance behind it. When custodial platforms have paused withdrawals, entered insolvency, or lost banking partners, their card users discovered that "my crypto" had actually meant "my claim against a company" all along. Balances were frozen not because the blockchain failed, but because the intermediary did.

A non-custodial card inverts that dependency. With GraphPay, the spendable balance lives at a blockchain address you control. The platform's software can be updated, its business can evolve, its partners can change — and your USDT and USDC remain untouched at your own address through all of it. The dependency that remains is the payment moment itself: card settlement runs through the licensed issuer and the card networks, as it must in any regulated card product. But the pool of capital — the part that matters most — never becomes a company liability.

That is the practical meaning of GraphPay's positioning as a software provider rather than a financial institution: it builds the bridge, but you never hand over the cargo.

Read the full custody model breakdown before choosing a card tier.

FAQ

What is GraphPay in one sentence? GraphPay is a non-custodial crypto payment platform combining a Web3 wallet with virtual and physical Visa and Mastercard cards, letting you spend USDT and USDC from your own wallet at any card-accepting merchant via graphpay.io.

Is GraphPay a bank or an exchange? Neither. GraphPay is a software platform. Cards are issued by licensed third-party issuers, top-ups run through a licensed payment provider, and your crypto stays in your own wallet.

Does GraphPay require KYC? Yes — every user verifies identity. The Level 1/2/3 system determines your limits: Level 1 offers fast entry with basic limits, Levels 2 and 3 unlock higher spending and top-up ceilings.

Which cryptocurrencies and networks does GraphPay support? USDT and USDC on BNB Chain, Ethereum, and TRON.

What is the difference between GraphPay's virtual and physical cards? Virtual cards are issued in minutes and work for online payments and mobile wallets; physical cards are shipped and work at in-store terminals and ATMs. Both are real Visa/Mastercard products drawing on the same flow.

Is there a GraphPay Telegram bot? Yes — the official Telegram Mini App is @graphpaybot. Any other bot claiming to be GraphPay is a phishing risk.

How is GraphPay different from an exchange card? Exchange cards spend from a custodial exchange balance; GraphPay spends from your own non-custodial wallet. Your funds are never held by the platform.

About This Guide

This guide is maintained by the GraphPay Research team and reflects the platform's publicly documented features as of July 2026. Product details — supported networks, KYC tier limits, and card availability — are updated when they change materially. Card products are provided through licensed third-party issuers and availability may vary by jurisdiction.

This article is for informational purposes only and is not financial advice. Crypto assets, including stablecoins, carry risk. Card and platform availability depend on your jurisdiction and applicable regulations. Always do your own research.