By GraphDex Research · Reviewed for accuracy May 2026

Quick Answer

Restaking lets you take staked ETH (or liquid staking tokens like stETH) and reuse them to secure additional protocols called Actively Validated Services (AVSs) — earning extra yield on top of base staking rewards. Key facts in 2026:

- EigenLayer dominance: $15B+ TVL, 94% of the restaking market

- The yield stack: ~3-4% Ethereum staking + ~1-2% AVS rewards = 4-7% real APY; looped strategies reach 15-20% with liquidation risk

- Liquid Restaking Tokens (LRTs): Ether.fi (eETH), Renzo (ezETH), Kelp DAO (rsETH), Puffer (pufETH) — let you participate without managing operators directly

- Major 2026 event: Kelp DAO suffered a ~$300 million exploit in April 2026, triggering ~$5.4 billion in withdrawals across the sector

- The core trade-off: extra yield in exchange for additional slashing risk and smart contract complexity

Restaking is real infrastructure, not just a meme — but it stacks risks beyond standard staking. Not for beginners.

Earn fee-based yield up to 17% APY on GraphDex

Key Takeaways

- Restaking reuses already-staked ETH or LSTs to secure additional protocols (AVSs) for extra yield.

- EigenLayer dominates with $15B+ TVL and 94% market share; LRTs are how most users participate.

- Real yields are 4-7% APY (base + AVS); looped strategies reach 15-20% with liquidation risk.

- The April 2026 Kelp DAO exploit demonstrated that smart contract risk is not theoretical.

What Is Restaking?

Restaking is the practice of taking already-staked ETH (or liquid staking tokens like stETH or rETH) and using them again — committing them to secure additional protocols beyond just Ethereum, in exchange for additional yield. EigenLayer introduced the concept to Ethereum in 2023, and by 2026 it has accumulated tens of billions in restaked ETH.

A simple analogy. Imagine you've deposited money in a bank that pays interest. Restaking is like having that same bank let you simultaneously use those funds to vouch for your neighbor's loan — earning an extra 3% on top of your base interest, without withdrawing your deposit. Your capital works in two places at once.

In crypto terms: when you stake ETH (earning ~3-4% in network rewards), your stake helps secure Ethereum. Restaking lets that same stake also help secure additional services — called Actively Validated Services (AVSs) — earning additional rewards from each one. The same capital, multiple economic security functions, multiple revenue streams.

Why this matters structurally. Bootstrapping a separate validator set for every new blockchain service is inefficient. Ethereum already has a large, economically bonded validator base. EigenLayer's insight was that this base could be reused — Ethereum's staked capital becomes shared security infrastructure for the whole ecosystem (oracles, bridges, data availability layers, rollups, AI verification services, and more).

The trade-off is risk. You earn from multiple services, but you take on slashing risk from each one. If a validator misbehaves on any AVS they're securing, the stake committed to that service can be penalized.

How Restaking Actually Works

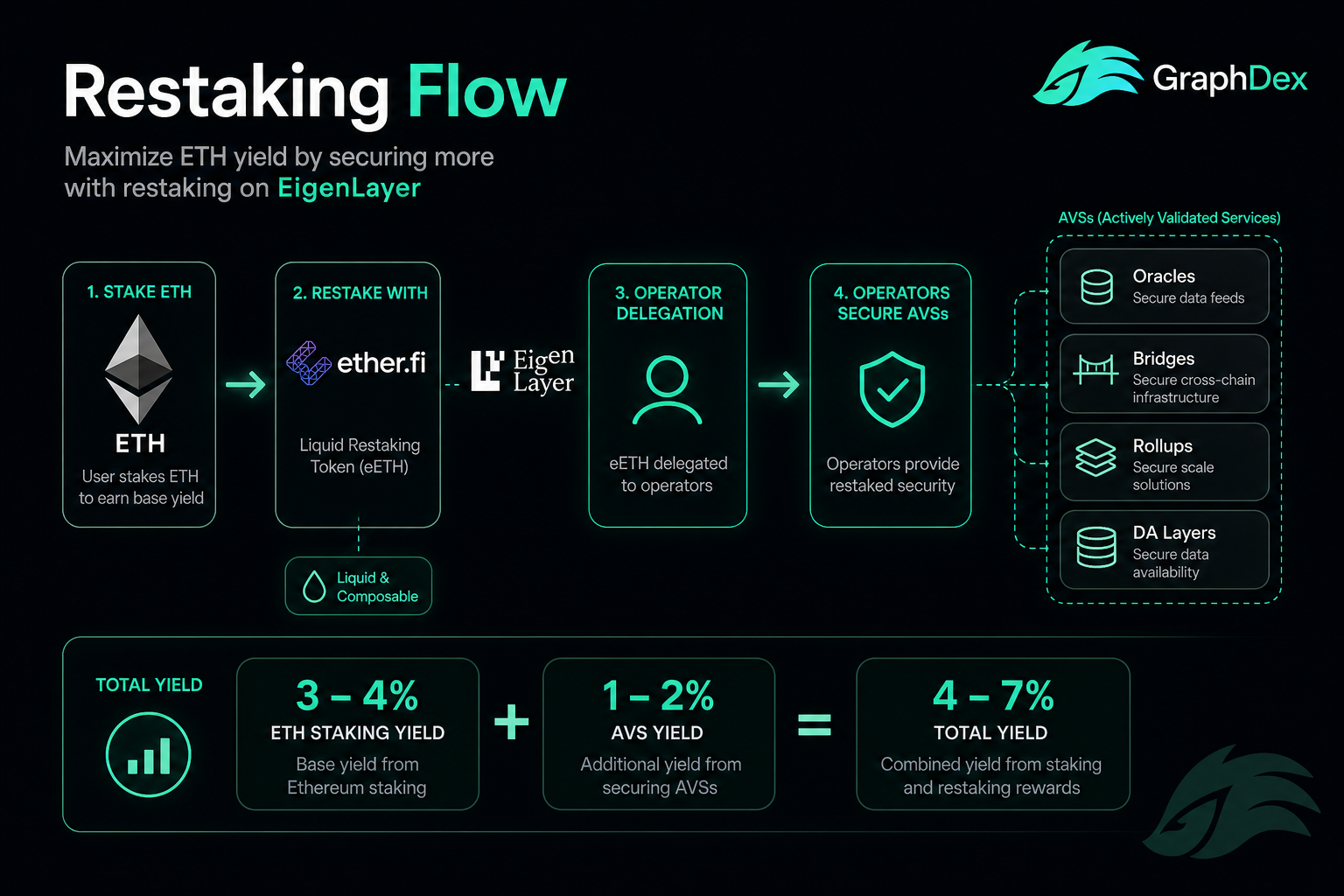

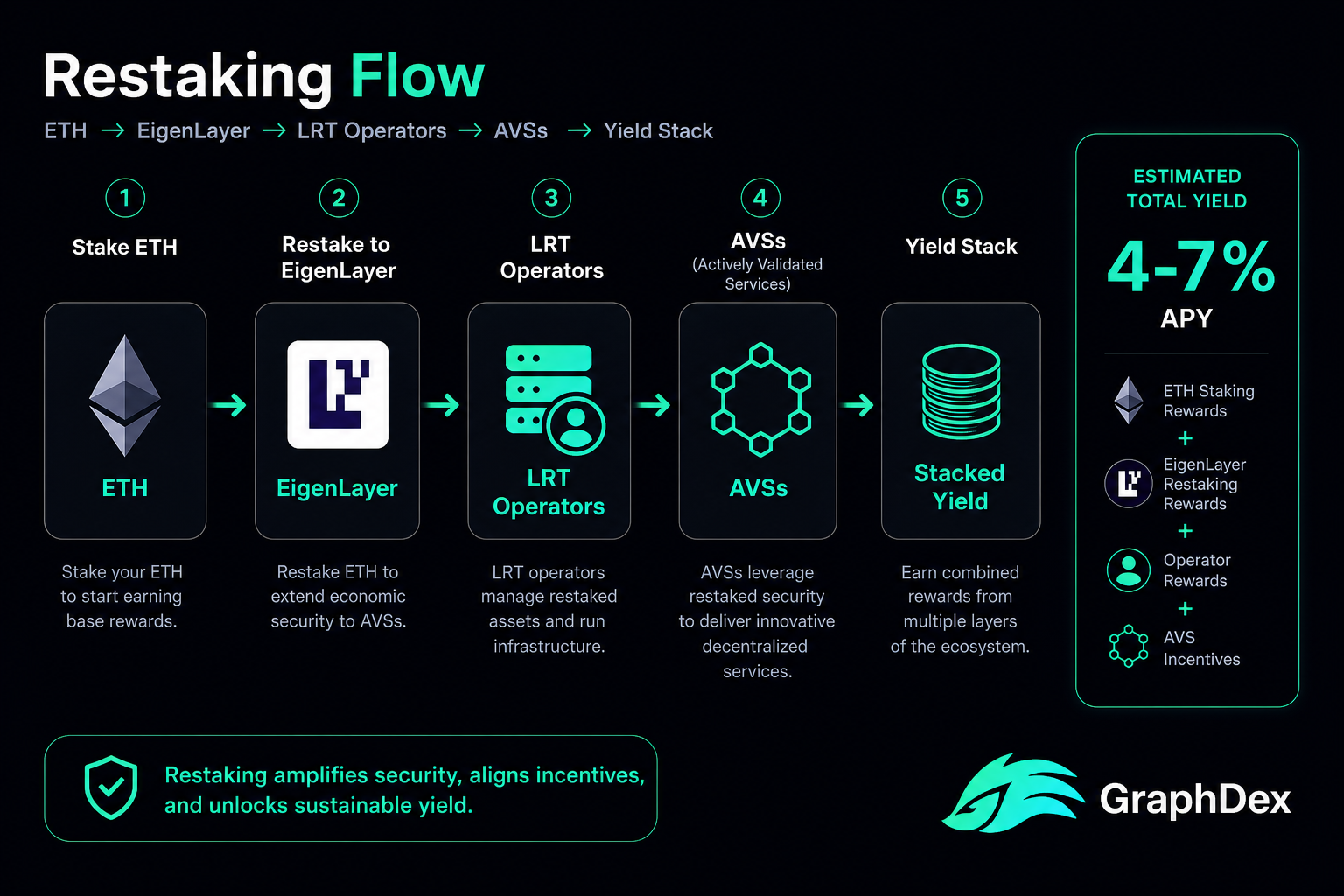

The mechanics involve four main participants:

1. Stakers. You deposit ETH or an LST (like stETH, rETH, cbETH) into a restaking protocol. Your capital becomes available to secure AVSs.

2. Operators. Specialized node operators run the actual software for AVSs. Stakers delegate to operators; operators do the technical work of validating AVS operations. You don't have to run infrastructure yourself.

3. AVSs (Actively Validated Services). Protocols that need cryptoeconomic security but don't want to bootstrap their own validator sets. They pay restakers (via operators) for the security their stake provides. Examples include data availability layers, oracle networks, bridges, rollup sequencing, and AI verification services.

4. The restaking protocol (EigenLayer). The marketplace that connects all three — managing delegations, tracking AVS commitments, and enforcing slashing rules.

The flow:

- You deposit ETH or an LST into EigenLayer (directly) or into an LRT protocol (which manages this for you)

- Your stake is delegated to one or more operators

- Operators sign up to validate specific AVSs and earn fees

- AVSs pay operators; operators share rewards with you (the staker) minus their commission

- Your base Ethereum staking rewards continue accruing

- Result: your single ETH stake earns from Ethereum + AVS rewards = stacked yield

The risks scale similarly. Each AVS your stake secures has its own slashing rules. If an operator misbehaves on any AVS, your stake committed to that service can be penalized. Slashing went live in 2025 — this is no longer theoretical.

What Are LRTs (Liquid Restaking Tokens)?

Most users don't restake directly with EigenLayer — they use LRT protocols, which abstract away the operator selection and management.

An LRT (Liquid Restaking Token) is a token you receive when depositing into a liquid restaking protocol. It represents your restaked position plus accrued rewards — and like LSTs (liquid staking tokens), LRTs remain usable across DeFi.

The major LRTs in 2026:

Ether.fi (eETH / weETH). The leading LRT protocol — eETH is the unwrapped version, weETH is the wrapped (rebasing) version used in DeFi. Ether.fi pioneered LRT design and has the largest TVL among LRTs.

Renzo (ezETH). Another major LRT competitor, focusing on user-friendly access to restaking yields.

Kelp DAO (rsETH). Stacked Kelp Miles on top of EigenLayer points and expanded to Layer 2 access earlier than most. Notably suffered a $300 million exploit in April 2026 (more on this below).

Puffer Finance (pufETH). Focuses on a different angle: anti-slashing technology and reducing the operator concentration risk that comes with most LRT protocols.

LRTs make restaking accessible — no operator selection, no manual delegations, no AVS analysis. You deposit ETH (or an LST), receive an LRT, and the protocol handles the complexity. The trade-off: you accept the protocol's choices about operators and AVS exposure.

How Much Can You Actually Earn?

Real yields matter more than headline numbers. Here's the honest breakdown.

The basic LRT yield stack in 2026:

- Base Ethereum staking: 3-4% APY

- EigenLayer AVS rewards: 1-2% APY

- Points and token incentives: variable

- Total real yield: typically 4-7% APY when paid in real revenue

- With speculative token incentives: higher, but sustainability is questionable

Looped restaking strategies. Sophisticated users layer restaking with leverage:

- Deposit 10 ETH into Ether.fi, receive 10 eETH (earning ~7% restaking yield)

- Use eETH as collateral on a lending protocol (Aave, Morpho)

- Borrow regular ETH (often at lower rate than eETH yield)

- Use borrowed ETH to buy more eETH

- Result: amplified ETH exposure, yields reach 15-20%+ — but with serious liquidation risk during market swings

This looped strategy can pay 15-20% APY in calm markets but liquidates quickly during volatility. It's appropriate only for users who understand and can manage liquidation risk.

The realistic takeaway: pure restaking yields cluster around 4-7%, only modestly above pure liquid staking (5-6%). The yield increment for the additional risk complexity is modest. Looped strategies offer higher yields but with materially higher risk.

The Kelp DAO Exploit and What It Changed

April 2026 brought the most significant stress event for the restaking sector.

What happened. Kelp DAO suffered an exploit of approximately $300 million in April 2026. The protocol survived, but the incident triggered roughly $5.4 billion in withdrawals across the entire restaking sector — users pulled funds from LRT protocols broadly, not just Kelp, as the risk conversation reset.

What it demonstrated. The smart contract risk in restaking — adding another protocol layer on top of staking, on top of LSTs — was not theoretical. The composability that gives restaking its power also creates stacked vulnerabilities. A bug in any layer (LST protocol, LRT protocol, EigenLayer itself, or specific AVS contracts) can affect funds.

What changed afterward.

- LRT protocols accelerated audits and bug bounty programs

- More users moved toward established protocols with longer audit histories (Ether.fi)

- EigenLayer pushed harder on operator safety scores and AVS risk ratings (still developing)

- The sector's risk conversation shifted from yield-chasing to risk-pricing

The Kelp exploit established a useful benchmark: when evaluating restaking yields, the appropriate comparison isn't "extra yield vs base staking" but "extra yield vs the additional smart contract surface area you're exposing yourself to."

The Risks of Restaking

For balance, restaking introduces specific risks worth understanding.

Stacked slashing risk. You're exposed to slashing on Ethereum AND slashing on every AVS your operator secures. Operators choose AVSs; you accept their choices. Misbehavior on any AVS can penalize your stake.

Smart contract risk multiplication. Native staking has one risk layer (Ethereum). Liquid staking adds another (LST protocol). Restaking adds another (EigenLayer). LRTs add another. Each layer is a potential exploit vector. The April 2026 Kelp DAO exploit proved this.

Concentration risk. EigenLayer holds 94% of the restaking market. An exploit at EigenLayer would not just be a protocol failure — it would be a systemic event for everything secured by AVSs, including data availability layers used by major rollups. This systemic concentration is the question to watch through 2026.

Operator risk. You delegate to operators who can misbehave or fail. LRT protocols choose operators on your behalf, but you inherit their decisions.

LRT depeg risk. Like LSTs, LRTs can trade at a discount to underlying assets during stress events. The 3-10 day exit window common in restaking can mean you're forced to sell at a discount if you need immediate liquidity.

Opacity between yield and risk. Most LRT holders see the yield (it shows up in the token's rewards) but don't read the slashing conditions of AVSs their ETH is exposed to. The gap between yield visibility and risk visibility is substantial. EigenLayer has proposed operator safety scores and AVS risk ratings, but as of mid-2026 these tools are still developing.

Governance risk. Major LRT and restaking protocols have governance tokens with concentration concerns.

Regulatory risk. Restaking sits in an evolving regulatory landscape. The March 2026 SEC/CFTC ruling cleared liquid staking but specific restaking treatment remains nuanced.

The honest takeaway: restaking is genuinely interesting infrastructure, but it stacks risks that pure staking doesn't have. The yield increment above liquid staking is modest, while the risk complexity increase is substantial. Suitable for sophisticated users who price in the complexity; less appropriate for beginners wanting simple passive yield.

Restaking vs Liquid Staking vs Native Staking

Three related concepts often get conflated. Here's how they compare:

| Model | Yield (typical) | Risk Level | Best For |

|---|---|---|---|

| Native staking | 3-5% (ETH), 5-7% (SOL) | Low | Passive holders wanting simplicity |

| Liquid staking | 5-6% (ETH/SOL) | Low-moderate | Active DeFi users wanting capital efficiency |

| Restaking (LRTs) | 4-7% real, up to 15-20% looped | Moderate-high | Sophisticated users who understand stacked risk |

Native staking is simplest — lock tokens, earn rewards.

Liquid staking adds capital efficiency via LSTs at the cost of smart contract risk.

Restaking stacks additional yield from AVSs at the cost of additional slashing and smart contract risk layers.

For most retail users, the practical choice is native or liquid staking. Restaking adds material complexity and risk for what is often a modest yield premium. The Kelp DAO exploit reinforces this — the extra yield from restaking didn't compensate users for the smart contract risk that was eventually realized.

Compare yield strategies safely on GraphDex

Restaking and Solana

Restaking as EigenLayer pioneered it is an Ethereum-native concept. On Solana, the ecosystem is younger and different in structure.

Solana doesn't yet have a dominant EigenLayer-equivalent. Some projects are exploring shared security and Solana restaking, but the category is in early stages compared to Ethereum's restaking maturity. Solana validators are smaller in number (~1,400 vs Ethereum's 900,000+), and the dynamics of shared security on Solana differ.

For Solana users wanting stacked yields, the more developed paths are:

- Liquid staking with JitoSOL (which captures MEV rewards on top of staking — somewhat analogous to additional yield layers)

- Yield farming with LSTs as collateral in DeFi protocols (Kamino, Drift)

- Fee-based yield platforms like GraphDex's up to 17% APY on stablecoins (a fundamentally different yield source than restaking)

Restaking specifically is currently an Ethereum-centric phenomenon. Solana's path to similar stacked yields uses different mechanics.

How GraphDex Approaches Yield (Without Restaking Risk)

GraphDex offers up to 17% APY on stablecoins and SOL — substantially higher than restaking yields, with a fundamentally different risk structure.

Fee-based yield, not network rewards. GraphDex's yield comes from platform trading fees — real revenue from actual trading activity on the platform. This is fundamentally different from restaking yields, which combine network rewards + AVS rewards + token incentives across multiple protocol layers.

No stacked smart contract risk. Restaking layers smart contract risk: LST + EigenLayer + LRT + AVS contracts. GraphDex's fee-based yield doesn't stack these layers — funds stay in a non-custodial wallet via Privy while earning yield from platform fees.

No slashing exposure. Restaking adds slashing risk from every AVS your stake secures. GraphDex's fee-based yield carries no slashing risk because it doesn't depend on PoS validation.

Integrated with broader activity. Your capital earns fee-based yield while you trade, use prediction markets, and discover tokens through Pulse — all in one non-custodial terminal.

This isn't to dismiss restaking — for sophisticated users who understand the risks, restaking can be a meaningful part of an ETH yield strategy. It's to say that fee-based platform yield (where the yield source is clearly identifiable as platform revenue) is a complementary, often simpler alternative for users prioritizing risk transparency.

Earn fee-based yield up to 17% APY on GraphDex

Frequently Asked Questions

What is restaking in simple terms? Restaking lets you take already-staked ETH (or liquid staking tokens like stETH) and reuse them to secure additional protocols (called AVSs) beyond Ethereum itself. Your stake earns base Ethereum staking rewards PLUS additional rewards from each protocol it helps secure. EigenLayer pioneered this in 2023; by 2026 it holds over $15 billion in restaked ETH.

How is restaking different from staking? Regular staking locks your tokens to secure one network (Ethereum) and earn its rewards (~3-4% APY). Restaking takes those same staked tokens and additionally commits them to secure other protocols (AVSs), earning extra rewards. The trade-off: you take on additional slashing risk from every AVS your stake secures.

What are LRTs? LRTs (Liquid Restaking Tokens) are tokens you receive when depositing into a restaking protocol. Examples: eETH (Ether.fi), ezETH (Renzo), rsETH (Kelp DAO), pufETH (Puffer). They represent your restaked position plus accrued rewards, and remain usable in DeFi — combining restaking yield with capital flexibility. Most retail users participate in restaking through LRTs rather than directly.

How much can you earn from restaking? Real yields are typically 4-7% APY (base Ethereum staking + AVS rewards), only modestly above pure liquid staking. Looped restaking strategies (using LRTs as collateral for leverage) can reach 15-20%, but with serious liquidation risk during market volatility. Beware speculative token incentives that inflate headline APYs.

What happened with the Kelp DAO exploit? Kelp DAO suffered a ~$300 million exploit in April 2026, triggering ~$5.4 billion in withdrawals across the entire restaking sector. The protocol survived, but the incident demonstrated that smart contract risk in restaking is not theoretical and reset the sector's risk conversation. Users became more cautious about LRT protocols generally.

Is restaking safe? Restaking adds risk layers beyond standard staking: slashing on each AVS, smart contract risk at multiple protocol levels, concentration risk at EigenLayer (94% market share), and LRT depeg risk during stress. The April 2026 Kelp exploit demonstrated this isn't theoretical. Suitable for sophisticated users who understand stacked risk; less appropriate for beginners wanting simple yield.

Is restaking available on Solana? Not in the dominant EigenLayer model. Restaking as a concept is currently Ethereum-centric. Solana's path to stacked yields uses different mechanics — MEV-capturing LSTs like JitoSOL, LST-as-collateral strategies in Solana DeFi (Kamino, Drift), and fee-based platform yields like GraphDex's up to 17% APY. The Solana shared-security category is younger than Ethereum's restaking maturity.

About This Guide

This guide is published by the GraphDex Research team — analysts and traders building the infrastructure for digital asset trading on Solana. Our content is based on live protocol data, current market figures, and hands-on experience.

Sources & data: TVL figures, APY rates, and exploit details reflect publicly available information as of 2026. Restaking carries significant risks including slashing and smart contract failure. This guide is educational and not financial advice — always do your own research.

GraphDex is the infrastructure for digital asset trading — trade, predict, and earn in one place. Learn more at graphdex.io.

Last reviewed: May 2026 · GraphDex Research

The infrastructure for digital asset trading. Trade, predict, stake, repeat. graphdex.io