By GraphDex Research · Reviewed for accuracy May 2026

Quick Answer

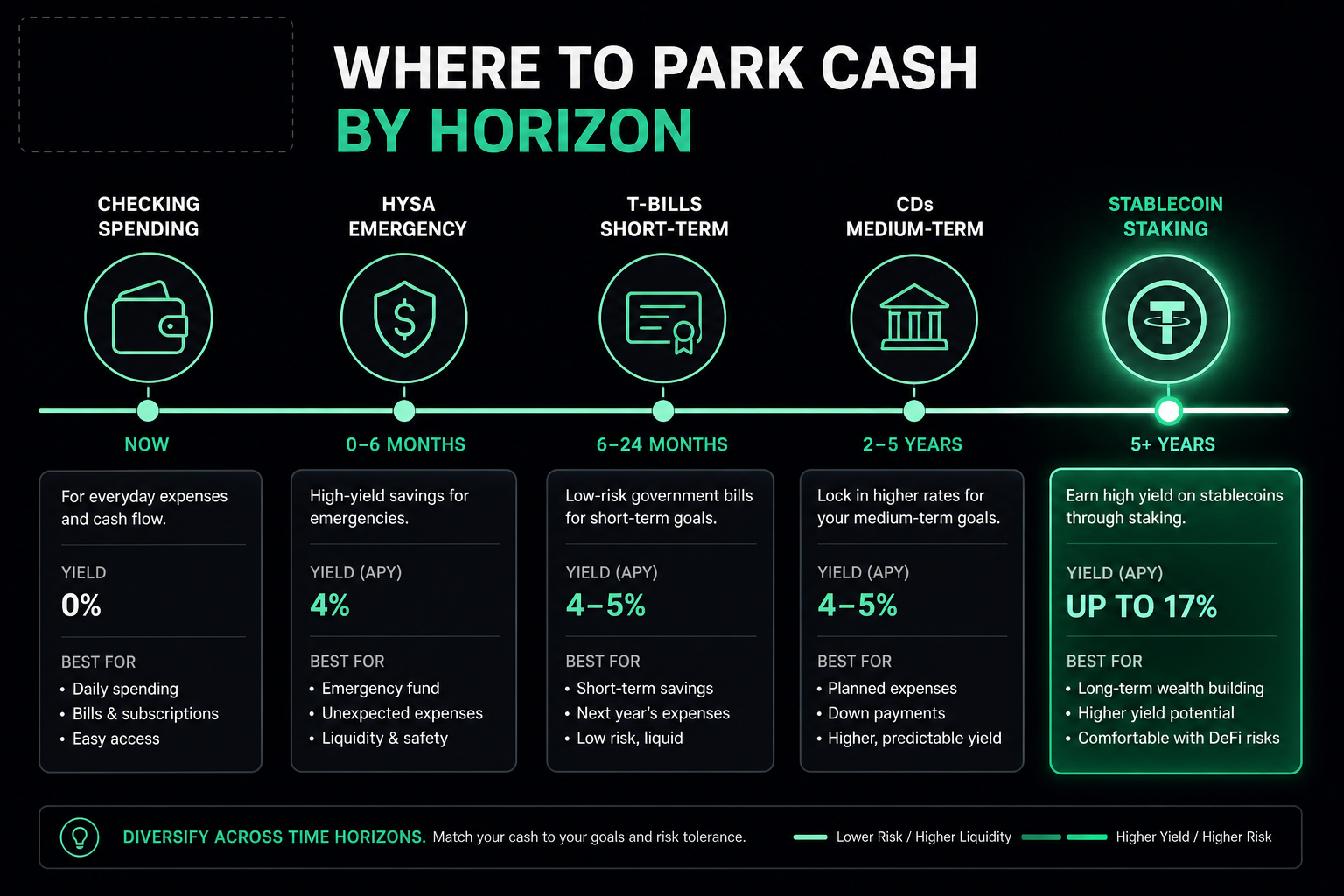

The best places to park cash in 2026, by time horizon:

- Need it now (emergency fund): High-yield savings account (~4%, FDIC-insured, instant access)

- Short-term (under 1 year): T-bills (~4%), money market funds (~5%)

- Medium-term (1-3 years): CDs (~4-5%, locked), or stablecoin staking (up to 17%)

- Can tolerate platform risk for higher yield: Stablecoin staking (up to 17%, dollar-stable)

The worst place is a standard checking account at 0.07% — that's a guaranteed loss to inflation. Match each pool of cash to how soon you'll need it.

Park cash at up to 17% APY with GraphDex

Key Takeaways

- A standard checking account pays just 0.07% — idle cash there loses purchasing power to inflation.

- Match cash to time horizon: instant-access for emergencies, higher-yield for money you can commit.

- High-yield savings (~4%) and money market funds (~5%) are safe, liquid options.

- Stablecoin staking offers up to 17% on dollar-stable assets for cash that can tolerate platform risk.

Why Does Idle Cash Lose Value?

With inflation forecasts rising and market volatility surging, many people are rethinking where to keep their cash. The OECD raised its US inflation forecast to 4.2% for 2026, and consumer confidence dropped to a 12-year low in early 2026.

Here's the issue: as of 2026, the average checking account pays just 0.07%. That's nowhere near the rate of inflation, so money sitting there loses purchasing power every month. Leaving cash in standard checking is great for quick access — but terrible for preserving value.

The solution is to park each pool of cash in the right place based on when you'll need it. Money for daily spending stays accessible; money you can commit longer earns more. The goal is keeping cash safe and accessible while still growing — not sitting idle losing value.

Where to Park Cash in 2026: By Time Horizon

| Time Horizon | Best Option | Return | Access |

|---|---|---|---|

| Daily spending | Checking (minimal balance) | 0.07% | Instant |

| Emergency fund | High-yield savings | ~4% | Instant |

| Under 1 year | T-bills, money market funds | 4-5% | Days |

| 1-3 years | CDs | 4-5% | Locked |

| Higher yield, flexible | Stablecoin staking | Up to 17% | Flexible terms |

For Your Emergency Fund: High-Yield Savings

Financial advisors recommend keeping an emergency fund covering 3-6 months of expenses somewhere safe and accessible. But "accessible" doesn't mean "idle."

A high-yield savings account (HYSA) lets you earn a better return without compromising on quick access. These accounts offer annual rates as high as 4% — versus 0.07% for checking — and remain FDIC-insured up to $250,000.

Best for: Your emergency fund and any cash you might need on short notice. Why: Combines instant access with a real return, keeping your safety net from eroding to inflation.

This is the baseline move: even money you can't risk should be earning ~4%, not 0.07%.

For Short-Term Cash: T-Bills and Money Market Funds

For cash you won't need for a few months up to a year, two safe options stand out.

Treasury bills (T-bills) are government-issued securities with maturities under a year. They're nearly risk-free and highly liquid — very safe places to park cash you'll need soon. You can buy them directly via TreasuryDirect.gov or through brokerages.

Money market funds invest in short-term, high-quality debt and yield around 5%, offering a low-risk way to earn interest on cash reserves.

Best for: Cash earmarked for a near-term goal (a purchase, a tax bill) you can't risk but want earning. Why: Higher yield than savings, still very safe and reasonably liquid.

For Medium-Term Cash: CDs

If your emergency fund is complete and you have additional savings you can lock up, a certificate of deposit (CD) can be a good fit. CDs offer fixed rates (around 4-5%) in exchange for committing your money for a set term.

Best for: Cash you're confident you won't need for the CD's term (6 months to a few years). Cons: Early withdrawal penalties; money is locked. Why: Slightly higher, guaranteed returns for committed capital, FDIC-insured.

For Higher Yield: Stablecoin Staking

For cash you want earning significantly more — and can tolerate platform risk instead of FDIC insurance — stablecoin staking has emerged as a high-yield option.

You hold dollar-pegged stablecoins (USDC, USDT) and earn yield from platform fees or lending. On GraphDex, this reaches up to 17% APY — several times more than any traditional cash option. Because stablecoins stay pegged to the dollar, your principal doesn't fluctuate like stocks or crypto.

Best for: Cash you want generating high yield, that can tolerate platform risk for a portion of your reserves. Cons: Not FDIC-insured; platform and smart contract risk. Why: At up to 17% versus ~4% for savings, the yield difference is dramatic — on dollar-stable assets.

The key distinction from a savings account: you trade FDIC insurance for much higher yield. Using a non-custodial platform like GraphDex (where funds stay in your own wallet) reduces the platform risk that affected custodial services like FTX.

Earn up to 17% on parked cash with GraphDex

How Should You Decide Where to Park Cash?

The right answer depends on one question: when will you need this money?

Money for this month's bills → checking account (minimal balance, just for spending).

Emergency fund (3-6 months expenses) → high-yield savings. Accessible, FDIC-insured, ~4%.

Cash for a goal in the next year → T-bills or money market funds. Safe, ~4-5%.

Cash you can lock for 1-3 years → CDs for guaranteed returns, or stablecoin staking for much higher yield if you accept platform risk.

Cash you want maximizing yield on → stablecoin staking at up to 17%, for the portion of reserves that can tolerate platform risk over FDIC insurance.

Most people benefit from spreading cash across these based on need: a small checking balance, a high-yield savings emergency fund, and — for those comfortable with it — a stablecoin staking allocation for the cash they want working hardest.

A Practical Example

Imagine you have $25,000 in cash currently sitting in checking at 0.07%, earning about $17 a year while losing ~4% ($1,000) to inflation.

Reallocated by time horizon:

- $3,000 in checking for monthly spending

- $12,000 emergency fund in high-yield savings at 4% → $480/year

- $10,000 in stablecoin staking at up to 17% → up to $1,700/year

Total potential earnings: up to ~$2,180 a year versus $17 — while keeping your emergency fund fully accessible and insured. The portion in staking trades FDIC insurance for dramatically higher yield, a choice you make only for cash that can tolerate it.

This illustrates the core principle: idle cash is a guaranteed loss, but matching each pool to the right home turns the same money into meaningful, inflation-beating returns.

Put your idle cash to work with GraphDex

Common Cash Management Mistakes

People lose money on idle cash through avoidable mistakes. Here are the most common ones to watch for.

Leaving everything in checking. The biggest mistake. A checking account paying 0.07% is for transactions, not savings. Any balance beyond your monthly spending should be earning more elsewhere.

Keeping too much in cash overall. While cash provides stability, holding far more than your emergency fund and near-term needs means missing the higher returns of invested capital. Cash beyond your safety net often belongs in higher-yield options.

Chasing teaser rates. Some accounts advertise high introductory rates that drop after a few months. Read the terms — a sustainable 4% beats a teaser 5% that falls to 1%.

Ignoring the inflation cost. Many people don't realize idle cash is actively losing value. At 3-4% inflation, "doing nothing" with cash is a real, compounding loss — not a neutral choice.

Over-locking liquidity. The opposite mistake: locking all your cash in CDs or long staking terms, leaving nothing accessible for emergencies. Always keep your emergency fund liquid.

The fix for all of these is the same: match each pool of cash to when you'll need it, ensure even safe money earns a real return, and never let large balances sit idle losing value to inflation.

Stop losing cash to inflation with GraphDex

Frequently Asked Questions

Where is the best place to park cash in 2026? It depends on when you'll need it. For emergency funds, high-yield savings (~4%, FDIC-insured). For short-term cash, T-bills or money market funds (4-5%). For higher yield on cash you can commit, stablecoin staking (up to 17%, not insured). Avoid leaving large balances in checking at 0.07%.

Why shouldn't I keep cash in a checking account? The average checking account pays just 0.07%, far below the 3-4% inflation rate. Money there loses purchasing power every year. Keep only spending money in checking; move the rest to high-yield options that earn a real return.

What's the safest place to park cash with good returns? High-yield savings accounts and money market funds (~4-5%) combine safety, FDIC insurance (savings), and liquidity. For higher yield without price volatility but no insurance, stablecoin staking offers up to 17% on dollar-stable assets.

How much can I earn parking cash in stablecoin staking? On GraphDex, up to 17% APY. On $10,000, that's up to $1,700 a year versus about $7 in a checking account or $400 in high-yield savings. The trade-off is no FDIC insurance and platform risk, so it suits cash that can tolerate those.

Is stablecoin staking safe for parking cash? It carries platform and smart contract risk and isn't FDIC-insured, unlike bank accounts. However, stablecoins hold their dollar value (no price volatility), and non-custodial platforms like GraphDex keep funds in your wallet. It suits a portion of cash you want maximizing yield, not your essential emergency reserve.

How should I split my cash across different options? Match each pool to when you'll need it: minimal checking for spending, high-yield savings for your emergency fund, T-bills or CDs for short-to-medium-term goals, and stablecoin staking for cash you want earning the most and can tolerate platform risk on.

What return should I expect on parked cash in 2026? Checking pays ~0.07%, high-yield savings ~4%, money market funds ~5%, CDs 4-5%, and stablecoin staking up to 17%. Higher returns come with trade-offs — locked terms (CDs) or platform risk (staking) instead of instant insured access.

About This Guide

This guide is published by the GraphDex Research team — analysts building the infrastructure for digital asset trading on Solana. Our content is based on live platform data and current market figures.

Sources & data: Rates and figures reflect publicly available information as of 2026 and are estimates. All investments carry risk; returns are not guaranteed. Stablecoin staking is not FDIC-insured. This guide is educational and not financial advice — consult a financial advisor for your situation.

GraphDex is the infrastructure for digital asset trading — trade, predict, and earn in one place. Learn more at graphdex.io.

Last reviewed: May 2026 · GraphDex Research

The infrastructure for digital asset trading. Trade, predict, stake, repeat. graphdex.io