By GraphDex Research · Reviewed for accuracy May 2026

Quick Answer

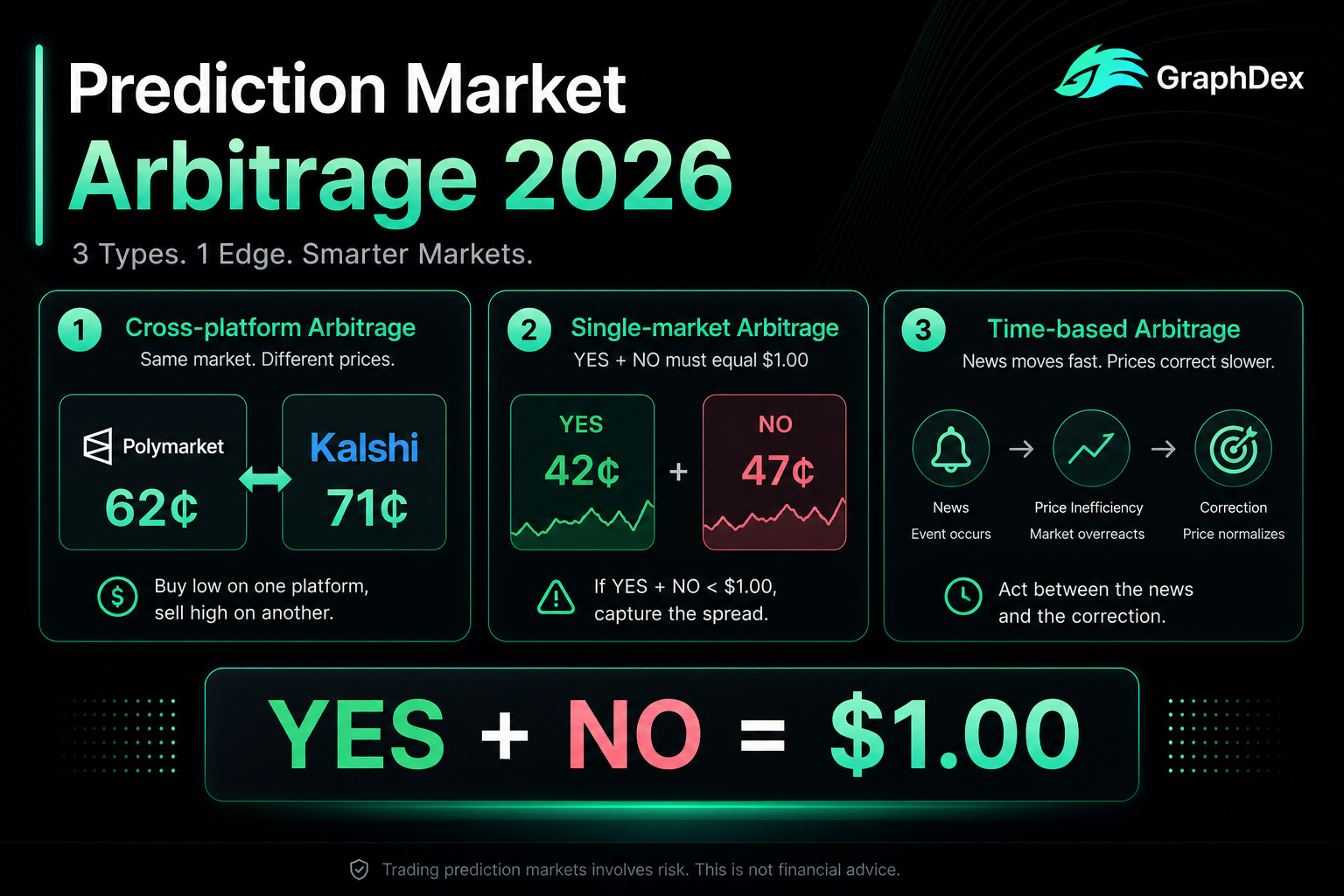

Prediction market arbitrage means capturing profit from price discrepancies that shouldn't exist. The main types:

- Cross-platform arbitrage — the same event priced differently on Polymarket vs Kalshi; buy the cheaper side, sell the dearer

- Single-market arbitrage — when YES + NO prices sum to less than $1.00 in one market, capture the gap

- Time-based arbitrage — exploit temporary mispricing after news before the market adjusts

Because outcomes are mathematically constrained (YES + NO must equal $1.00), gaps create near-guaranteed profit. Over $40 million in arbitrage was documented across prediction markets in 2024-2025. Margins are thin and competition fierce, so speed — often automation — is essential.

Track cross-venue opportunities with GraphDex

Key Takeaways

- Arbitrage captures near-guaranteed profit from price gaps that violate the YES + NO = $1.00 rule.

- Main types: cross-platform (Polymarket vs Kalshi), single-market (YES+NO under $1), and time-based.

- Over $40 million in arbitrage was extracted from prediction markets in 2024-2025.

- Margins are thin and competition fierce — speed and often automation are essential to capture gaps.

What Is Prediction Market Arbitrage?

Prediction market arbitrage is the practice of capturing profit from price discrepancies that, in theory, shouldn't exist. It's considered one of the lower-risk strategies because, when executed correctly, the profit is locked in regardless of the event's outcome.

The foundation is a mathematical constraint: in a binary prediction market, the YES and NO prices should sum to exactly $1.00, because exactly one outcome will occur. A YES share priced at $0.60 implies a 60% probability; the NO share should then be $0.40. When these prices deviate from $1.00 — within one market or across platforms — an arbitrage opportunity exists.

By trading both sides of the discrepancy, you construct a position that pays out $1.00 regardless of which outcome happens, for a total cost less than $1.00. The difference is your locked-in profit. This is why arbitrage is "near risk-free" — you're not betting on an outcome, you're capturing a pricing inefficiency.

The opportunity is real: academic research documented over $40 million in arbitrage profits extracted from prediction markets between April 2024 and April 2025.

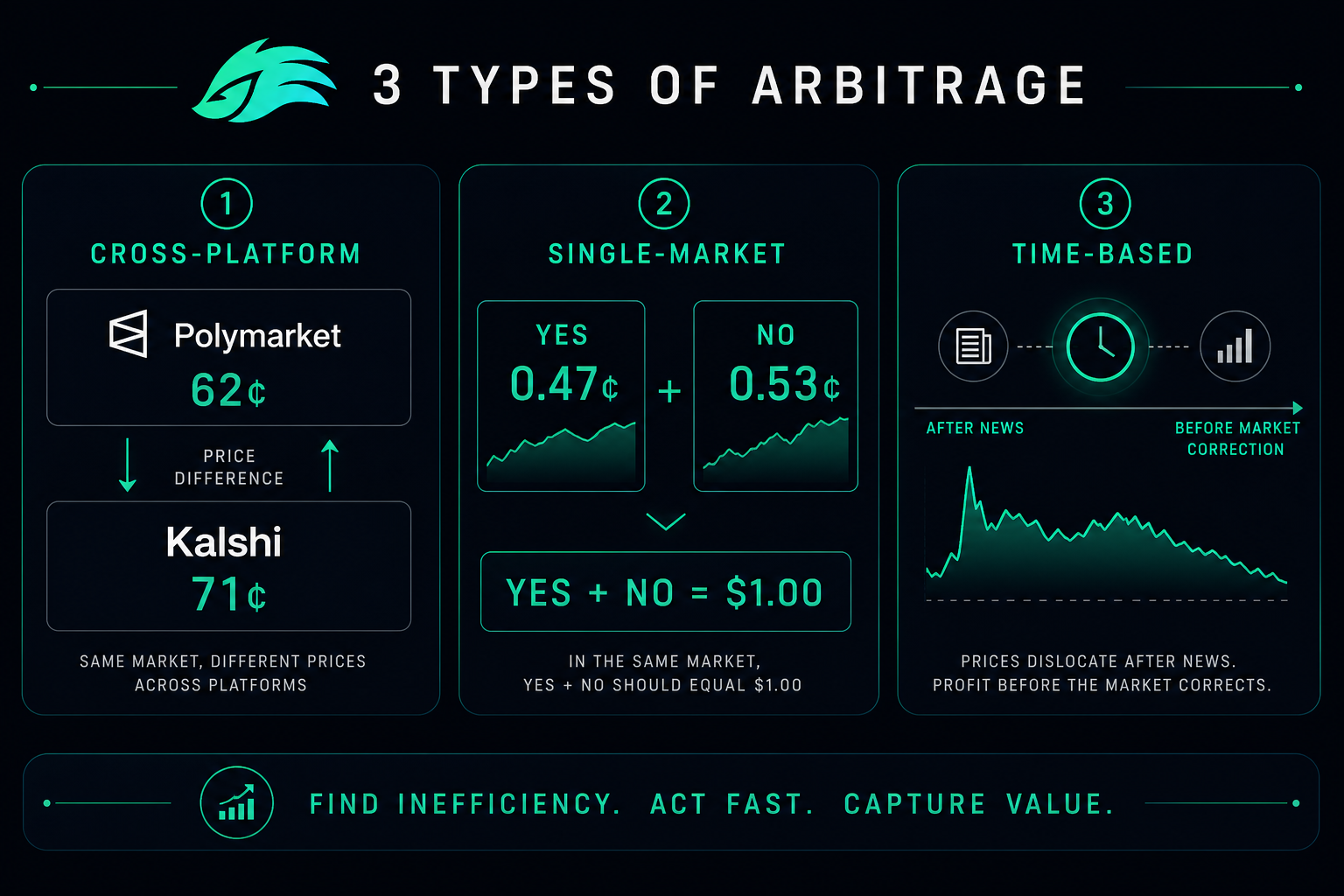

Type 1: Cross-Platform Arbitrage

The most common form exploits price differences for the same event across Polymarket and Kalshi (a CFTC-regulated competitor).

When the same event trades at different prices on the two platforms, you buy the cheaper side on one and the opposite on the other to lock in profit.

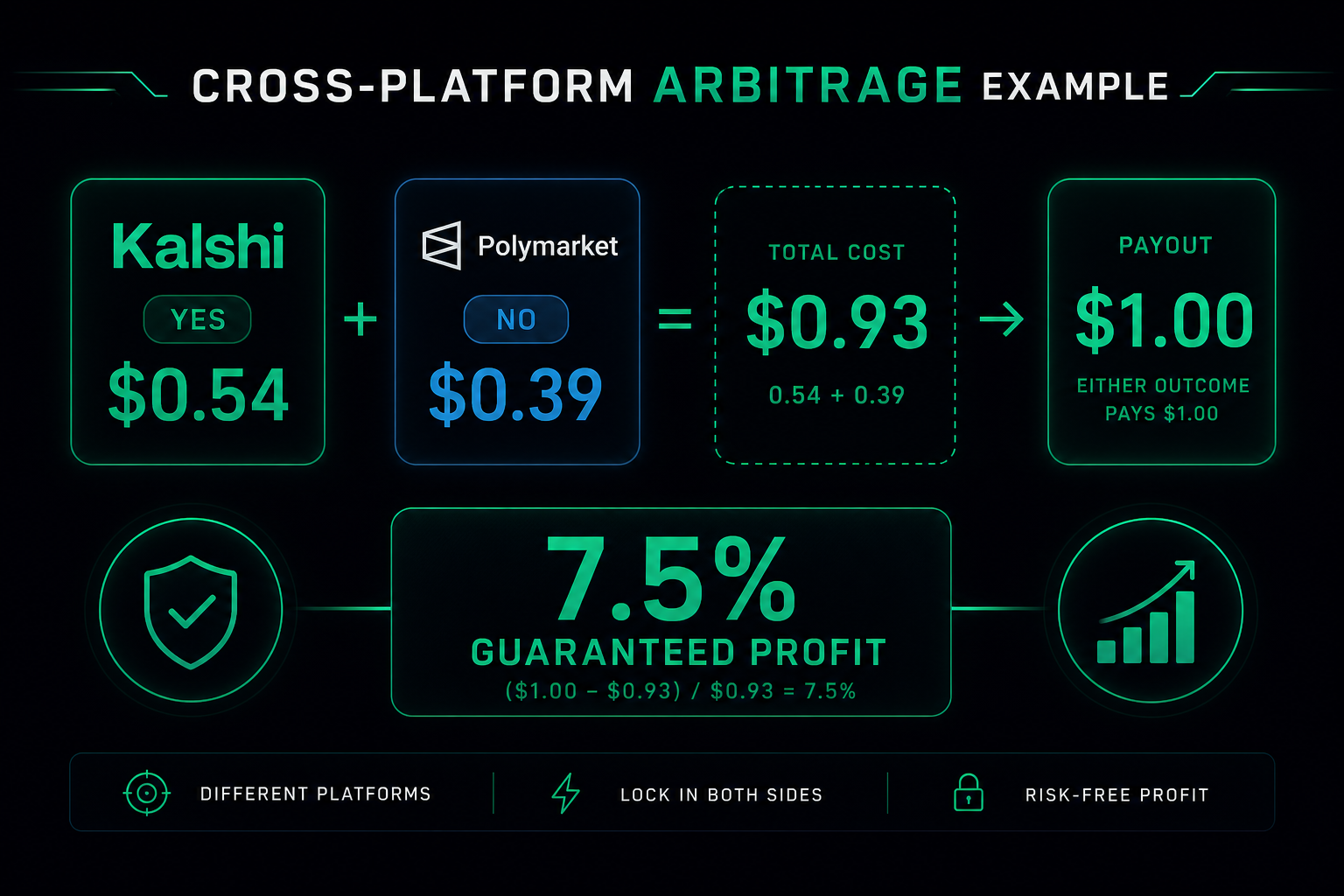

Example: "Will the Senate pass the Budget Reconciliation Act in Q2 2026?"

- Polymarket: YES at $0.61 (so NO is effectively $0.39)

- Kalshi: YES at $0.54

You buy YES on Kalshi at $0.54 and NO on Polymarket at $0.39.

- Total cost: $0.54 + $0.39 = $0.93

- Guaranteed payout: $1.00 (one side must win)

- Guaranteed profit: 7.5% before fees

This works because the two platforms price the same event differently, and you've covered both outcomes. The catch is that you need accounts and capital on both platforms, and the gap must exceed total fees to be profitable.

Type 2: Single-Market Arbitrage

Sometimes the discrepancy exists within a single market — no cross-platform risk required.

This occurs when the YES and NO prices in one market sum to less than $1.00. Buying both sides guarantees a $1.00 payout for less than $1.00 cost.

Example: A binary market on Polymarket:

- YES: $0.58

- NO: $0.38

- Total: $0.96

Buying both YES and NO costs $0.96 but guarantees a $1.00 payout (one must win), for a guaranteed $0.04 (about 4%) profit before fees.

Single-market arbitrage is simpler than cross-platform because it requires only one platform and carries no cross-venue execution risk. However, these gaps are rarer and close quickly, since they represent obvious inefficiencies that bots hunt constantly.

Type 3: Time-Based Arbitrage

A more advanced form exploits temporary mispricing after news breaks, before the market fully adjusts.

When significant news hits — a poll, an economic release, a breaking event — prices should move to reflect the new information. But markets don't adjust instantly. There's a window, sometimes seconds, where the price still reflects the old information. A trader who processes the news faster than the market can capture the gap.

This isn't pure arbitrage (it carries some risk that your read of the news is wrong), but it's closely related — you're exploiting an inefficiency in how fast the market incorporates information. The wallets generating the largest returns on Polymarket are often those being faster than the market's own information processing, rather than predicting outcomes.

This is the hardest type to execute manually, since the window is brief — it typically requires automation or tools that surface news impact instantly.

How Much Can Arbitrage Earn?

Arbitrage returns are typically small per trade but add up with volume and frequency:

| Arbitrage Type | Typical Margin | Risk | Difficulty |

|---|---|---|---|

| Cross-platform | 2-8% per opportunity | Very low | Moderate |

| Single-market | 1-5% per opportunity | Very low | Low |

| Time-based | Variable | Low-moderate | High |

The $40+ million extracted across prediction markets in 2024-2025 shows the cumulative opportunity is significant. However, individual margins are thin, and as more participants and bots compete, gaps close faster and margins compress. Successful arbitrageurs rely on volume (many small captures) and speed (catching gaps before they close).

Why Is Speed the Key Challenge?

Arbitrage sounds like free money, but two factors make it hard in practice.

Competition compresses margins. Because arbitrage is near risk-free, it attracts sophisticated traders and bots constantly scanning for gaps. The more competition, the faster gaps close and the smaller they get. Obvious opportunities rarely last.

Speed is everything. A gap that exists now may vanish in seconds. Capturing it requires near-instant detection and execution across potentially two platforms. Manual trading is often too slow — by the time you spot a gap, navigate to both platforms, and execute, it's gone.

This is why serious arbitrageurs use automation or specialized tools that scan markets continuously and execute fast. Cross-venue aggregators that compare Polymarket and Kalshi prices in real time, and integrated terminals that let you act instantly, are the practical way to capture arbitrage before competition closes the gap.

Spot and act on opportunities fast with GraphDex

What Tools Help With Arbitrage?

Capturing arbitrage efficiently requires the right tools:

Cross-venue scanners compare prices across Polymarket and Kalshi in real time, flagging discrepancies with net profit calculated after fees. These are essential for cross-platform arbitrage.

Fast execution terminals let you act on a detected gap before it closes. The faster the path from detection to execution, the more gaps you capture.

Whale and news tracking surface time-based opportunities — when a large trade or breaking news creates temporary mispricing.

GraphDex helps by integrating real-time tracking, AI signals (surfacing news impact and mispricing), and fast execution in one terminal. Rather than spotting a gap in one tool and switching to another to act — losing the window — GraphDex lets you track and execute in one place. Combined with Solana DEX trading and staking up to 17% APY, you can pursue arbitrage while your idle capital earns.

For traders serious about arbitrage, the speed advantage of unified detection and execution directly affects how many opportunities you capture before competition closes them.

Pursue arbitrage with integrated tools on GraphDex

What Are the Risks of Arbitrage?

While arbitrage is "near risk-free," it's not entirely without risk — understanding the caveats matters.

Execution risk. In cross-platform arbitrage, you must execute both legs. If one fills and the other doesn't (or moves), you're left with an unhedged position. Speed and reliable execution reduce this.

Fee risk. Margins are thin, so fees can eat the profit. Always calculate net profit after all fees (trading fees, network fees, withdrawal costs) before executing.

Capital lockup. Arbitrage often ties up capital until resolution, especially single-market arbitrage where you hold both sides to payout. This limits how often you can recycle capital.

Resolution risk. Rare events — oracle disputes, cancelled events, ambiguous resolutions — can disrupt the expected payout. Even "guaranteed" arbitrage carries tail risk in edge cases.

Platform and access risk. Cross-platform arbitrage requires accounts on multiple platforms, with the regulatory and access considerations that entails (especially for US users on certain platforms).

Realistic arbitrage is profitable but operationally demanding — it rewards speed, capital efficiency, careful fee math, and reliable tools more than it rewards prediction skill.

Related Guides

- Prediction Market Copy Trading in 2026: The Complete Guide

- Best Polymarket Alternatives 2026: Kalshi, GraphDex & 8 More Compared

- How to Make Money on Polymarket in 2026: 6 Proven Strategies

Frequently Asked Questions

What is prediction market arbitrage? Arbitrage captures near-guaranteed profit from price discrepancies — when the same event is priced differently across platforms, or when YES + NO prices sum to less than $1.00 in one market. By trading both sides, you lock in profit regardless of the outcome. Over $40 million was extracted this way in 2024-2025.

Is prediction market arbitrage really risk-free? It's "near risk-free" but not entirely. Done correctly, profit is locked regardless of outcome. But execution risk (one leg failing), fee risk (thin margins), capital lockup, and rare resolution disputes all add some risk. It's lower-risk than directional betting, not zero-risk.

How much can you make from arbitrage? Margins are typically 1-8% per opportunity, small individually but cumulative with volume. Over $40 million was documented across prediction markets in 2024-2025. Returns depend on capital, speed, and how many opportunities you capture before competition closes them.

What's the difference between cross-platform and single-market arbitrage? Cross-platform arbitrage exploits price differences for the same event across Polymarket and Kalshi — you trade on both. Single-market arbitrage exploits YES + NO summing to under $1.00 within one market — simpler, one platform, no cross-venue risk, but rarer.

Do I need a bot for prediction market arbitrage? Not strictly, but it helps significantly. Gaps close in seconds, and competition is fierce, so manual trading often misses opportunities. Cross-venue scanners and fast execution tools — or automation — dramatically improve how many gaps you capture. Tools like GraphDex unify detection and execution.

Why do arbitrage opportunities exist if markets are efficient? Markets aren't perfectly efficient in real time. Different platforms have different participants and liquidity, news takes time to propagate, and prices adjust at different speeds. These frictions create temporary gaps. Competition closes them quickly, which is why speed matters.

What tools help with prediction market arbitrage? Cross-venue scanners (comparing Polymarket and Kalshi prices), fast execution terminals (acting before gaps close), and news/whale tracking (spotting time-based opportunities). GraphDex integrates real-time tracking, AI signals, and execution in one terminal to capture opportunities fast.

About This Guide

This guide is published by the GraphDex Research team — analysts and traders building the infrastructure for digital asset trading on Solana. Our content is based on live platform data, current market figures, and hands-on experience with the platforms covered.

Sources & data: Arbitrage figures and examples reflect publicly available information as of 2026 and are illustrative, not guarantees. Prediction market trading carries risk, including in arbitrage. This guide is educational and not financial advice — always do your own research.

GraphDex is the infrastructure for digital asset trading — trade, predict, and earn in one place. Learn more at graphdex.io.

Last reviewed: May 2026 · GraphDex Research

The infrastructure for digital asset trading. Trade, predict, stake, repeat. graphdex.io