By GraphPay Research · Reviewed for accuracy May 2026

Quick Answer

The best non-custodial crypto cards in 2026, where your funds stay in your own wallet:

- GraphPay — Best overall: tiered KYC (Level 1→3), multi-chain (BNB/Ethereum/TRON), Visa & Mastercard, funds always in your wallet

- Bleap — Best MPC architecture (EU, 0% FX, strong rewards)

- Gnosis Pay — Best on-chain identity (EU/UK, wallet-based)

- Oobit — Best global reach (150+ countries, self-custodial)

- Ready Card — Best rewards (3% STRK, self-custody, EU/US)

Why non-custodial matters: With custodial cards, the issuer holds your funds — adding solvency risk (issuer failure) and security risk (hacker target). Non-custodial cards keep your crypto in your wallet, converting only when you spend. Regulators increasingly recommend self-custodial models, and security-conscious users prefer never surrendering control.

The best combination: Non-custodial architecture + tiered KYC (verify only as much as you need). GraphPay delivers both.

Get a non-custodial GraphPay card

Key Takeaways

- Non-custodial crypto cards keep your funds in your own wallet — the card converts only when you spend.

- This eliminates issuer solvency risk and reduces the security exposure of custodial platforms.

- Leading non-custodial cards: GraphPay, Bleap, Gnosis Pay, Oobit, Ready Card.

- The strongest model combines non-custodial architecture with flexible, tiered KYC.

What Is a Non-Custodial Crypto Card?

A non-custodial crypto card lets you spend crypto at regular merchants while your funds stay in your own wallet. Unlike custodial cards — where you deposit crypto and the issuer holds it — non-custodial cards authorize conversion only at the moment you make a purchase.

How it works:

- You connect your own Web3 wallet (you control the keys)

- Your spending power reflects your wallet balance

- When you make a purchase, the card converts only the needed amount from your wallet to fiat

- The merchant receives a normal card payment; your remaining crypto stays in your wallet

The fundamental difference from custodial cards:

With a custodial card, you transfer crypto to the issuer. They hold it. You're trusting their solvency (will they stay in business?) and their security (will they get hacked?). Your funds sit in their custody until you spend.

With a non-custodial card, your crypto never leaves your control until the instant you spend. There's no deposit sitting in someone else's account. The card is a spending rail connected to your wallet — not a place to park funds.

Why this distinction matters enormously: Crypto's founding principle is self-custody — "not your keys, not your coins." Custodial cards reintroduce the exact counterparty risk crypto was designed to eliminate. Non-custodial cards let you spend crypto in the real world while keeping the self-custody that makes crypto valuable.

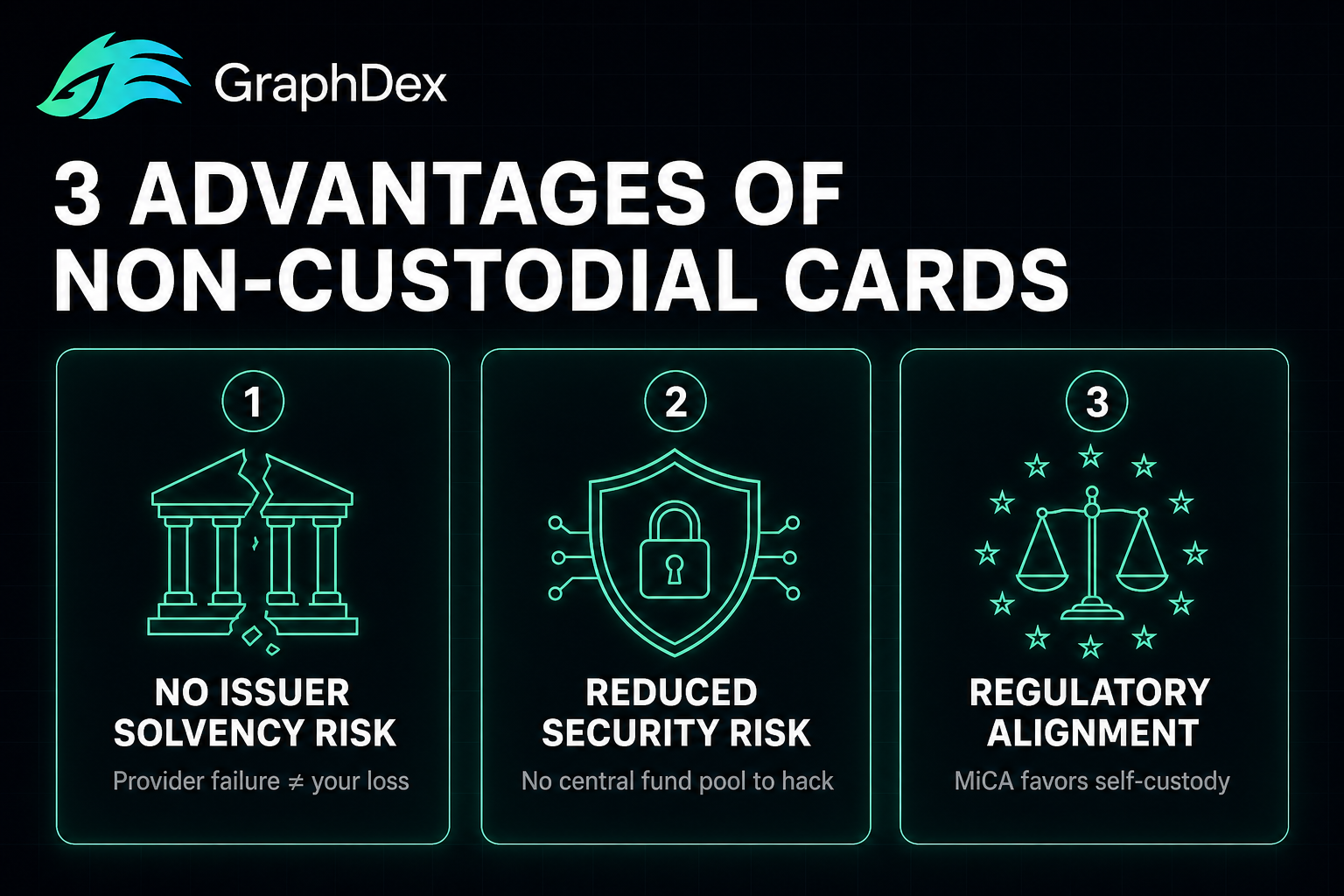

Why Non-Custodial Cards Are the Better Model

Three concrete advantages make non-custodial the superior approach for most users.

1. No Issuer Solvency Risk

When an issuer holds your funds, their failure becomes your loss. The crypto industry has a documented history of custodial platforms failing, freezing withdrawals, or shutting down — taking user funds with them. With a non-custodial card, your funds are in your wallet. If the card provider has problems, your crypto is unaffected — it was never in their custody.

2. Reduced Security Risk

Custodial platforms aggregate many users' funds in one place — making them concentrated, high-value targets for hackers. A single breach can affect thousands of users. With non-custodial cards, there's no central pool of user funds to steal. Your wallet is yours; a breach of the card provider doesn't drain your assets.

3. Regulatory Alignment

Regulators increasingly favor self-custodial models. Frameworks like MiCA (mandatory for EU CASPs by July 1, 2026) emphasize consumer protection — and self-custody inherently protects consumers from issuer failure. Non-custodial cards align with where regulation is heading: compliant identity verification (tiered KYC) combined with user-controlled funds (self-custody).

The combined picture: Non-custodial cards give you the real-world spending utility of a card without the counterparty risk of a custodian. You verify your identity (tiered KYC, for compliance and limits) but never hand over your assets. This is the model that resolves crypto's core tension — using crypto in daily life without abandoning self-custody.

How We Ranked These Non-Custodial Cards

Our rankings weigh:

- True non-custodial architecture: Do funds genuinely stay in your wallet?

- KYC flexibility: Tiered verification (start light, upgrade) vs single-tier

- Network acceptance: Visa/Mastercard global reach

- Multi-chain support: Which chains and tokens can you use?

- Fees: Top-up, FX, issuance

- Geographic availability: Where can you use it?

- Rewards and features: Cashback, mobile pay, physical cards

#1: GraphPay — Best Overall Non-Custodial Card

Architecture: Non-custodial (Web3) KYC: Tiered (Level 1→2→3) Networks: Visa & Mastercard Chains: BNB Chain, Ethereum, TRON (USDT, USDC)

GraphPay ranks #1 for combining true non-custodial architecture with flexible tiered KYC — the two factors that matter most. Your crypto stays in your own wallet at every verification level, and you start light (Level 1) and upgrade only as needed (Level 3).

Why it leads:

- Genuinely non-custodial: Your crypto stays in your own wallet (Web3 infrastructure). The card converts only when you spend — funds are never held by a third party.

- Flexible KYC: Start at Level 1 (virtual card, minimal verification), upgrade to Level 3 (physical card, highest limits) as your needs grow.

- Multi-chain: Load spending power from BNB Chain, Ethereum, or TRON using USDT or USDC.

- Global acceptance: Visa and Mastercard rails — tens of millions of merchants.

- MiCA-aligned: Built for the compliant, self-custodial model regulators recommend.

Where it wins: The complete package — non-custodial + tiered KYC + multi-chain + dual networks. Start light, grow as needed, funds always yours. Where competitors win: Some EU-specialized cards (Bleap, Gnosis Pay) offer region-specific DeFi features.

#2: Bleap — Best MPC Architecture

Architecture: Non-custodial (MPC) KYC: Full KYC Networks: Mastercard Region: EU focus

Bleap uses MPC (multi-party computation) for non-custodial security — your assets stay in your wallet, secured by distributed key management. It offers 0% FX fees, meaningful cashback, and fee-free trading, all MiCA-compliant.

Where it wins: MPC architecture, 0% FX, strong rewards, MiCA-compliant. Where it falls short: Full KYC only (no lighter entry tier); EU-focused; Mastercard only.

#3: Gnosis Pay — Best On-Chain Identity

Architecture: Non-custodial (on-chain wallet) KYC: Wallet-based tiers Networks: Visa Region: EU/UK

Gnosis Pay connects directly to your on-chain wallet — your wallet address serves as your identity for basic functions. EU/UK-focused Visa with stablecoin support, 0% FX, and variable token rewards. Deeply DeFi-native.

Where it wins: On-chain wallet identity, minimal custodial data, DeFi-native. Where it falls short: EU/UK focus; higher tiers require additional verification.

#4: Oobit — Best Global Reach

Architecture: Self-custodial KYC: Low entry requirements Networks: Visa Region: 150+ countries

Oobit never holds your assets — you connect your own wallet, and it facilitates spending. Available in 150+ countries with minimal basic-account requirements and zero fees, it has the widest global reach of the non-custodial options.

Where it wins: Self-custodial, 150+ countries, zero fees, broad availability. Where it falls short: No cashback rewards; confirm current tier requirements.

#5: Ready Card — Best Rewards

Architecture: Self-custody KYC: Minimal Networks: Visa Region: EU/US

Ready Card is a self-custody Visa offering 3% STRK (Starknet token) cashback with minimal verification requirements. Available in EU and US.

Where it wins: 3% cashback, self-custody, EU and US availability. Where it falls short: STRK rewards carry token price risk; newer program.

Comparison Table

| Card | Architecture | KYC | Networks | Region |

|---|---|---|---|---|

| GraphPay | Non-custodial (Web3) | Level 1→3 | Visa & Mastercard | Multi-region |

| Bleap | Non-custodial (MPC) | Full | Mastercard | EU |

| Gnosis Pay | Non-custodial (on-chain) | Wallet-based | Visa | EU/UK |

| Oobit | Self-custodial | Low entry | Visa | 150+ countries |

| Ready Card | Self-custody | Minimal | Visa | EU/US |

Non-Custodial vs Custodial: The Full Comparison

Understanding the trade-offs helps you choose with confidence.

Custodial Cards

How they work: You deposit crypto; the issuer holds and manages it.

Pros:

- Sometimes simpler initial setup

- May offer integrated exchange features

Cons:

- Solvency risk (issuer failure = your loss)

- Security risk (concentrated hacker target)

- You don't control your funds

- More extensive data collection

- Contradicts crypto's self-custody principle

Non-Custodial Cards

How they work: Your crypto stays in your wallet; the card converts only when you spend.

Pros:

- No issuer solvency risk to your funds

- Reduced security exposure (no central fund pool)

- You always control your assets

- Aligns with self-custody principle

- Regulator-favored model

Cons:

- Requires managing your own wallet (though modern Web3 onboarding simplifies this)

- Slightly different mental model than traditional cards

The verdict for most users: Non-custodial is the safer, more principled choice. The main historical drawback — wallet complexity — has been largely solved by modern Web3 infrastructure that makes self-custody nearly as simple as a traditional account. With non-custodial cards, you get real-world spending without surrendering the control that makes crypto valuable.

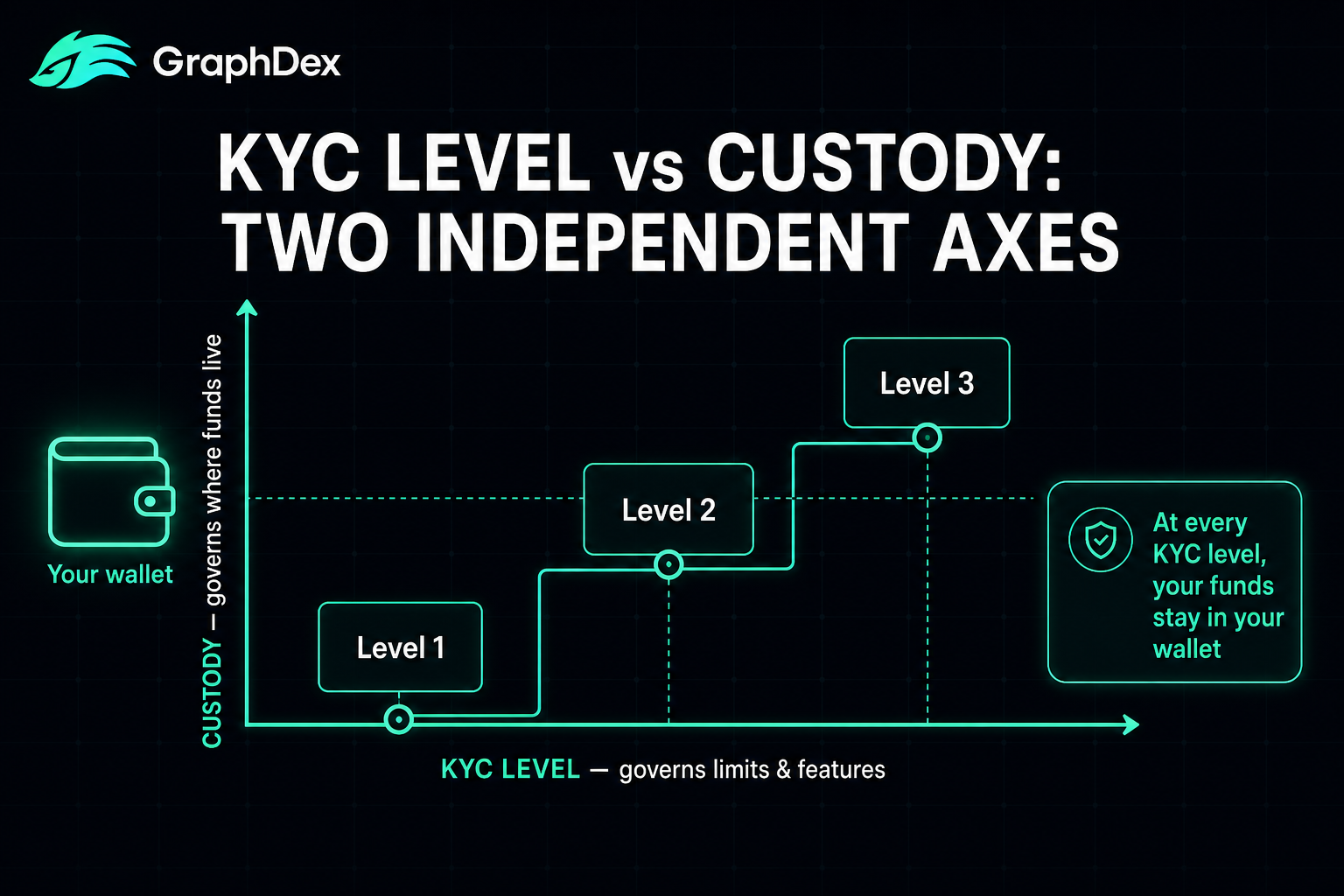

How Non-Custodial Cards Handle KYC

A common misconception: that non-custodial means no identity verification. It doesn't — and that's a good thing.

The reality: Non-custodial cards still implement KYC (often tiered, Level 1→3) because they run on regulated payment networks (Visa/Mastercard) and must comply with AML rules (FATF, MiCA). The "non-custodial" part refers to custody of funds, not verification of identity.

What this means:

- KYC level governs your spending limits and features (verify more = higher limits)

- Non-custodial architecture governs where your funds live (your wallet, not the issuer)

These are independent. A non-custodial card with Level 1 KYC keeps your funds in your wallet AND has lower limits. The same card at Level 3 keeps your funds in your wallet AND has high limits. Custody never changes; verification (and thus limits) scales.

Why this is the ideal model: You comply with regulations (tiered KYC for limits) while retaining self-custody (funds in your wallet). You're verifying your identity to use the payment rails — not handing over your assets. This resolves the tension between compliance and self-custody that defines the 2026 crypto card market.

GraphPay is built on exactly this model: tiered KYC for compliant limits, non-custodial architecture for fund control.

How GraphPay Delivers Non-Custodial Spending

GraphPay is built from the ground up on non-custodial architecture combined with flexible tiered KYC.

The non-custodial foundation:

- Your crypto stays in your own Web3 wallet at all times

- The card converts only the amount you spend, at the moment you spend it

- No deposits sitting in third-party custody

- No issuer solvency risk to your funds

Combined with flexible KYC:

- Level 1: Virtual card, minimal verification — funds in your wallet

- Level 2: Higher limits, more features — funds in your wallet

- Level 3: Physical card, highest limits — funds in your wallet

Plus full capability:

- Multi-chain: BNB Chain, Ethereum, TRON (USDT, USDC)

- Visa and Mastercard global acceptance

- MiCA-aligned for the compliant, self-custodial future

The bottom line: GraphPay gives you the real-world spending utility of a card — online, in-store, anywhere the networks are accepted — while your crypto stays in your wallet at every KYC level. You verify your identity for compliant limits, but you never surrender your assets. That's the non-custodial promise, delivered.

Get your non-custodial GraphPay card

Frequently Asked Questions

What is a non-custodial crypto card? A non-custodial crypto card lets you spend crypto at regular merchants while your funds stay in your own wallet. Unlike custodial cards (where the issuer holds your deposited crypto), a non-custodial card converts crypto to fiat only at the moment you make a purchase. Your assets remain under your control until you spend — eliminating issuer solvency and custody risk.

Why are non-custodial cards safer? Two reasons. First, no issuer solvency risk — if the card provider fails, your funds are in your wallet, unaffected. Second, reduced security risk — there's no central pool of user funds for hackers to target. Custodial platforms have a documented history of failures and freezes; non-custodial cards keep your assets out of that risk entirely.

Do non-custodial crypto cards require KYC? Yes — non-custodial refers to custody of funds, not identity verification. Non-custodial cards still implement KYC (often tiered, Level 1→3) because they run on regulated networks (Visa/Mastercard) and must comply with AML rules. The difference: KYC governs your limits, while non-custodial architecture keeps your funds in your wallet. The two are independent.

What's the best non-custodial crypto card in 2026? For the complete package — non-custodial + tiered KYC + multi-chain + dual networks — GraphPay leads. For MPC architecture in the EU: Bleap. For on-chain identity: Gnosis Pay. For global reach: Oobit (150+ countries). For rewards: Ready Card (3% STRK). The best choice combines non-custodial architecture with flexible verification.

Can I use a non-custodial card anywhere? Yes — non-custodial cards on Visa/Mastercard rails are accepted at tens of millions of merchants worldwide, online and in-store, just like any traditional card. The merchant sees a normal card payment; the crypto-to-fiat conversion happens behind the scenes from your wallet. Acceptance depends on the network (Visa/Mastercard) and your card's geographic availability.

Is a non-custodial card harder to use than a custodial one? Not significantly anymore. The historical drawback — managing your own wallet — has been largely solved by modern Web3 infrastructure that makes self-custody nearly as simple as a traditional account. You connect your wallet, verify to your chosen KYC level, and spend. The slight learning curve is well worth keeping control of your funds.

Does non-custodial mean my transactions are anonymous? No. Non-custodial means you control your funds, not that transactions are anonymous. Non-custodial cards on regulated networks implement KYC and comply with AML rules. Your spending is processed through regulated payment rails. "Non-custodial" is about fund control and security — not anonymity. Tiered KYC is part of every compliant non-custodial card.

About This Guide

This guide is published by the GraphPay Research team — building non-custodial crypto payment infrastructure. Our content is based on current card industry practices, regulatory frameworks, and 2026 market data.

Sources & data: Card architectures, custody models, and features reflect publicly available information as of 2026 and may change. Specific terms vary by provider and jurisdiction. This guide is educational and not financial or legal advice — always verify current terms and consult local regulations.

GraphPay is non-custodial crypto payment infrastructure — your crypto, your pay. Learn more at graphpay.io.

Last reviewed: May 2026 · GraphPay Research