By GraphPay Research · Reviewed for accuracy May 2026

Quick Answer

Crypto card fees in 2026 fall into seven categories — and the hidden ones matter most:

- Top-up / loading fee — charged when you add crypto to the card (the headline fee)

- Exchange-rate spread — the hidden markup on crypto-to-fiat conversion (often 0.5-1.5%, rarely listed)

- FX fee — for spending in foreign currencies

- Card issuance fee — one-time cost for the card (virtual or physical)

- ATM withdrawal fee — for cash withdrawals (physical cards)

- Monthly / maintenance fee — some cards charge ongoing fees

- Inactivity fee — some cards charge if unused

The hidden cost to watch: The exchange-rate spread is the most overlooked fee. A card advertising "no fees" may still take 1-1.5% on the conversion rate. Always compare the conversion rate against the market rate — not just the stated fees.

The smart approach: Compare total cost for your usage pattern, factor custody (non-custodial cards reduce certain risks), and check the conversion rate, not just headline fees.

See GraphPay's transparent pricing

Key Takeaways

- Crypto card costs go beyond the headline fee — seven fee types affect your real cost.

- The exchange-rate spread (0.5-1.5%) is the most commonly hidden cost — check conversion rates.

- "No-fee" cards often recover costs through FX spreads or other charges.

- Compare total cost for YOUR usage pattern, not just advertised fees.

Why Crypto Card Fees Are Confusing

Crypto card pricing is deliberately hard to compare. Providers emphasize whatever number looks best in marketing — "0% FX!" or "no monthly fee!" — while quieter costs make up the difference.

The core problem: There's no standardized way crypto cards present fees. One card advertises "no top-up fee" but takes 1.5% on conversion. Another advertises "0% FX" but charges a monthly fee. A third looks expensive on top-up but is cheapest overall for high-volume users. Comparing headline numbers alone is misleading.

The result: Two cards that look very different on advertised fees might cost nearly the same in practice — or a card that looks cheap might be the most expensive for your usage. The only way to compare accurately is to understand every fee type and model your actual usage.

This guide's goal: Break down all seven fee categories so you can calculate true cost — and spot the hidden charges that marketing obscures. Transparent pricing is itself a sign of a trustworthy provider.

Fee #1: Top-Up / Loading Fee

The most visible fee — charged when you add crypto to your card.

How it works: When you load crypto onto a card (or, for non-custodial cards, when you fund spending power), the provider may charge a percentage of the amount. This is often the "headline" fee providers advertise or compete on.

Typical range: Varies widely — from 0% to several percent. Some providers charge a flat percentage; others tier it by volume or KYC level.

What to watch:

- Is it a percentage or flat fee?

- Does it vary by chain or token?

- Does it differ by KYC level?

- Is it lower for higher verification tiers?

The non-custodial nuance: With non-custodial cards, "top-up" works differently — your funds stay in your wallet, and the fee (if any) may apply at the point of spending/conversion rather than a separate loading step. Understand how your specific card structures this.

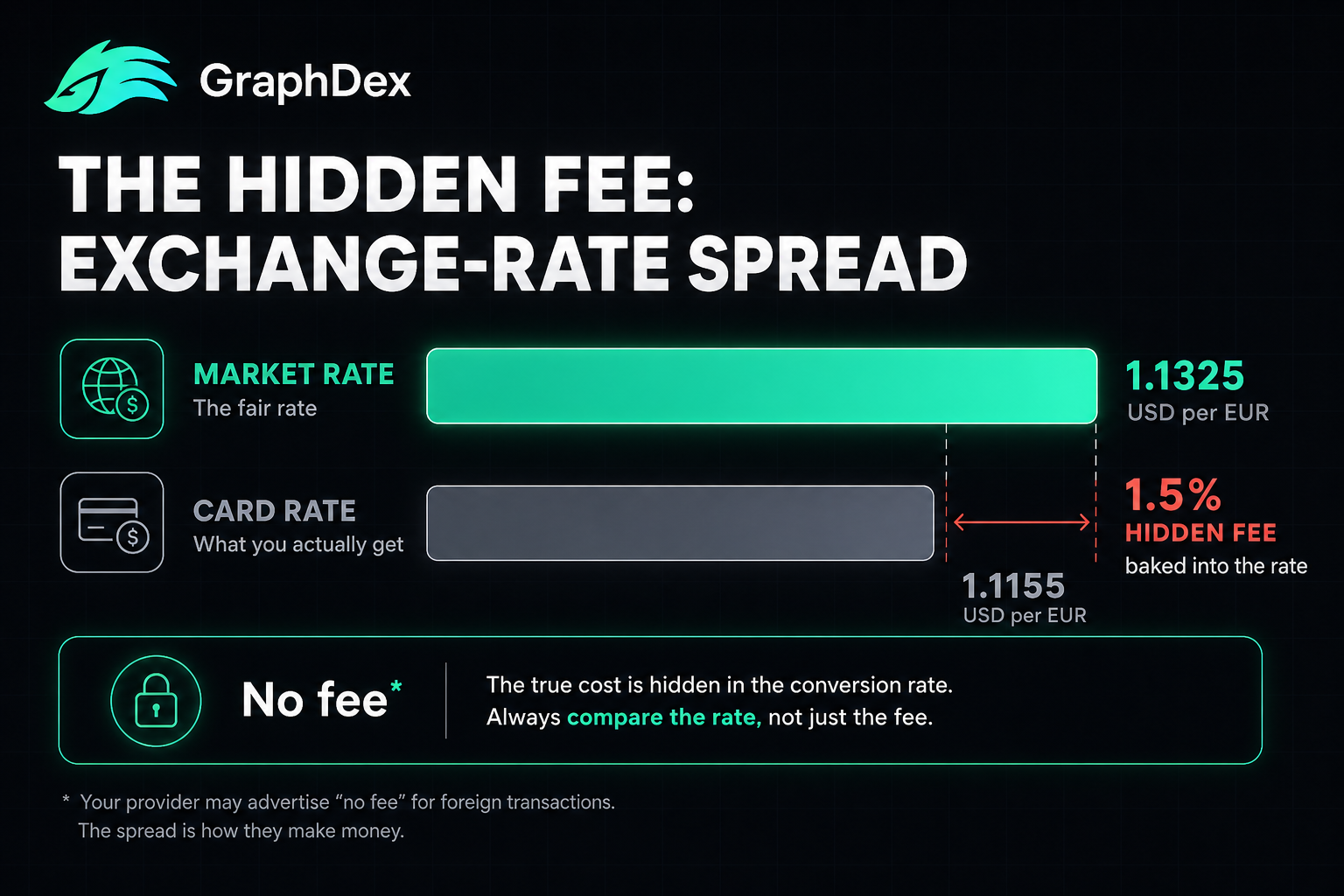

Fee #2: The Exchange-Rate Spread (The Hidden One)

The most important fee most users never notice — the markup baked into the crypto-to-fiat conversion rate.

How it works: When your crypto converts to fiat (to pay a merchant), the provider applies an exchange rate. If that rate is worse than the true market rate, the difference is a hidden fee. A card might convert at a rate 1-1.5% worse than market — effectively a 1-1.5% fee that never appears as a "fee" line item.

Why it's hidden: It's embedded in the rate, not listed as a charge. A card advertising "no conversion fee" might still take 1.5% through an unfavorable rate. The marketing is technically true (no explicit "fee") while the cost is real.

Typical range: Often 0.5-1.5%, though it can be higher on less competitive cards.

How to check it:

- Note the rate your card uses for a conversion

- Compare it to the market rate at that moment (from a major exchange or price aggregator)

- The difference is your real spread cost

Why this matters most: For regular spending, the exchange-rate spread can be your single largest cost — larger than the advertised fees. A card with "no fees" but a 1.5% spread is more expensive than a card with a 0.5% top-up fee but a tight conversion rate. Always factor the spread.

Fee #3: FX Fee (Foreign Currency)

Charged when you spend in a currency different from your card's base currency.

How it works: If your card is denominated in one currency and you spend in another (traveling, buying from foreign merchants), an FX fee may apply — typically a percentage of the transaction.

Typical range: 0% to 3%. Some cards advertise "0% FX" as a key feature (Bleap, Gnosis Pay, for example).

What to watch:

- Does the card charge FX fees at all?

- Is "0% FX" genuine, or offset by a worse exchange rate?

- Does it apply to all foreign currencies or specific ones?

For frequent travelers or international shoppers, the FX fee is a major cost factor. A genuine 0% FX card (with a fair conversion rate) offers real savings.

Fee #4: Card Issuance Fee

A one-time cost to obtain the card.

How it works: Some providers charge to issue a card — virtual or physical. Virtual cards are often free or low-cost; physical cards more commonly carry an issuance/shipping fee.

Typical range: Virtual cards often free to low-cost; physical cards may carry a modest one-time fee plus shipping.

What to watch:

- Is the virtual card free?

- What does a physical card cost (Level 3)?

- Does the issuance fee differ by KYC level or card type?

This is a one-time cost, so it matters less for long-term users than recurring fees — but it's worth knowing upfront.

Fee #5: ATM Withdrawal Fee

For physical cards (Level 3), the cost of withdrawing cash.

How it works: When you withdraw cash from an ATM using a crypto card, fees may apply from both the card provider and the ATM operator. Some cards offer a free withdrawal allowance, then charge beyond it.

Typical range: Varies — sometimes a percentage, sometimes flat, sometimes a free allowance then fees. The ATM operator's own fee is separate.

What to watch:

- Is there a free withdrawal allowance?

- Percentage or flat fee beyond it?

- Note the ATM operator's separate fee

For users who need cash access, ATM fees matter. For purely digital spenders, they're irrelevant.

Fee #6: Monthly / Maintenance Fee

Some cards charge an ongoing fee to keep the card active.

How it works: A recurring (usually monthly) charge for maintaining the account or card. Some premium tiers charge monthly fees in exchange for higher limits or better rewards; many standard cards have none.

Typical range: $0 to a monthly subscription, depending on card tier.

What to watch:

- Is there any monthly fee?

- Is it offset by rewards or higher limits?

- Does a free tier exist?

For most users, a card with no monthly fee is preferable unless premium benefits justify the cost.

Fee #7: Inactivity Fee

Some cards charge if you don't use the card for a period.

How it works: If the card goes unused for a defined period (often months), a fee may be deducted. Designed to encourage usage or offset maintenance costs.

Typical range: Varies; many cards have none.

What to watch:

- Does an inactivity fee exist?

- After how long?

- This matters if you want a card for occasional use only

Fees Comparison Table

| Fee Type | Typical Range | Hidden? | Matters Most For |

|---|---|---|---|

| Top-up / loading | 0% to several % | No (advertised) | Everyone |

| Exchange-rate spread | 0.5-1.5%+ | Yes (in the rate) | Regular spenders |

| FX fee | 0% to 3% | Sometimes | Travelers, int'l shoppers |

| Card issuance | Free to modest | No | New users |

| ATM withdrawal | Varies | Sometimes | Cash users |

| Monthly / maintenance | $0 to subscription | No | Long-term users |

| Inactivity | Varies / none | Sometimes | Occasional users |

How to Calculate Your True Crypto Card Cost

Headline fees mislead. Calculate real cost for your usage:

Step 1: Estimate your usage pattern.

- How much will you load/spend monthly?

- Domestic or international spending?

- Need cash (ATM) access?

- Occasional or regular use?

Step 2: Add up the fees that apply to YOU.

- Top-up fee on your monthly load amount

- Exchange-rate spread on your conversions (check the actual rate!)

- FX fee if you spend internationally

- ATM fees if you withdraw cash

- Monthly fee if any

- Issuance fee (one-time)

Step 3: Compare cards on YOUR total, not headlines.

A card with a low top-up fee but high spread might cost more than one with a modest top-up fee and tight spread. A "no monthly fee" card might lose to a subscription card if the subscription unlocks much better rates for your volume.

Step 4: Factor non-fee considerations.

- Custody (non-custodial reduces risk)

- Limits at your KYC level

- Network acceptance (Visa/Mastercard)

- Supported chains/tokens

The key insight: The cheapest card on paper is often not the cheapest in practice. Model your actual usage, check the conversion rate (not just stated fees), and compare total cost.

Red Flags in Crypto Card Pricing

Watch for these warning signs of expensive or untrustworthy pricing:

1. "No fees" with no rate transparency. If a card claims "no fees" but won't clearly show its conversion rate, the cost is likely hidden in the spread.

2. Vague fee disclosure. Trustworthy providers list all fees clearly. Vague or hard-to-find fee schedules suggest hidden costs.

3. Unusually high top-up fees. Some cards charge several percent just to load — eroding your funds before you spend.

4. Poor conversion rates. Compare the card's rate to market. A consistently unfavorable rate is a hidden fee.

5. Stacked fees. Some cards combine high top-up + high FX + high spread — each individually "reasonable" but together expensive.

6. Custodial risk on top of fees. A custodial card adds counterparty risk to its fees. Non-custodial cards reduce this risk dimension entirely.

7. Fees that change without notice. Read terms on whether fees can change and how you'll be notified.

How GraphPay Approaches Fees

GraphPay aims for transparent, straightforward pricing combined with non-custodial security.

The GraphPay approach:

- Clear top-up pricing: A transparent fee when you fund spending power — no hidden surprises

- Non-custodial: Your crypto stays in your wallet, converting only when you spend — you're not paying to park funds in someone else's custody

- Multi-chain flexibility: Load from BNB Chain, Ethereum, or TRON (USDT, USDC) — choose the most cost-effective chain for your needs

- Tiered KYC economics: Higher verification levels (Level 3) typically unlock better limits and economics

- Visa & Mastercard: Global acceptance without surprise network surcharges

Why transparency matters: The biggest crypto card cost — the exchange-rate spread — thrives on opacity. GraphPay's approach favors clarity so you can calculate your real cost upfront. Combined with non-custodial architecture, you avoid both hidden fees and the counterparty risk of custodial cards.

When comparing GraphPay to other cards, model your actual usage and compare total cost — including the conversion rate, not just headline fees. Transparent pricing plus self-custody is the combination worth seeking.

Frequently Asked Questions

What fees do crypto cards charge? Seven main types: top-up/loading fee (adding funds), exchange-rate spread (hidden markup on conversion, often 0.5-1.5%), FX fee (foreign currency spending), card issuance fee (one-time), ATM withdrawal fee (cash), monthly/maintenance fee (ongoing), and inactivity fee (if unused). The exchange-rate spread is the most commonly hidden and often the largest real cost.

What is the hidden fee on crypto cards? The exchange-rate spread — the markup baked into the crypto-to-fiat conversion rate. A card might convert at a rate 0.5-1.5% worse than the true market rate, effectively charging a fee that never appears as a "fee" line item. A card advertising "no fees" may still take 1.5% this way. Always compare the conversion rate to the market rate.

Are "no-fee" crypto cards really free? Rarely fully free. "No-fee" usually means no explicit top-up or monthly fee — but costs may be recovered through the exchange-rate spread (the markup on conversions) or FX fees. To know the real cost, check the conversion rate against the market rate, not just the advertised fees. Transparent providers show their rates clearly.

How do I calculate the true cost of a crypto card? Estimate your usage (monthly spend, domestic vs international, cash needs), then add up only the fees that apply to you — top-up, exchange-rate spread (check the actual rate!), FX, ATM, monthly. Compare cards on your total, not headline numbers. The cheapest card on paper is often not cheapest in practice once the spread is included.

Do non-custodial cards have lower fees? Not necessarily lower headline fees, but they remove one cost dimension: you're not paying to park funds in someone else's custody, and you avoid the counterparty risk of custodial cards. Non-custodial cards (like GraphPay) still have fees (top-up, spread, etc.), but your funds stay in your wallet — reducing risk alongside whatever fees apply. Compare both fees and custody.

Why do crypto cards charge FX fees? FX fees apply when you spend in a currency different from your card's base currency — covering the currency conversion. Some cards advertise "0% FX" as a benefit, but verify it's genuine and not offset by a worse exchange rate. For travelers and international shoppers, FX fees (or their absence) significantly affect total cost.

How can I avoid hidden crypto card fees? Five steps: (1) Always check the conversion rate against the market rate; (2) Read the full fee schedule, not just marketing; (3) Calculate total cost for your specific usage; (4) Watch for "no fee" claims without rate transparency; (5) Choose providers with clear, upfront pricing. Transparent pricing is itself a sign of a trustworthy provider.

About This Guide

This guide is published by the GraphPay Research team — building non-custodial crypto payment infrastructure. Our content is based on current card industry practices and 2026 market data.

Sources & data: Fee structures and typical ranges reflect publicly available information as of 2026 and may change. Specific fees vary by provider, KYC level, and jurisdiction. This guide is educational and not financial advice — always verify current fees and conversion rates with your provider before committing.

GraphPay is non-custodial crypto payment infrastructure — your crypto, your pay. Learn more at graphpay.io.

Last reviewed: May 2026 · GraphPay Research