By GraphPay Research · Reviewed for accuracy May 2026

Quick Answer

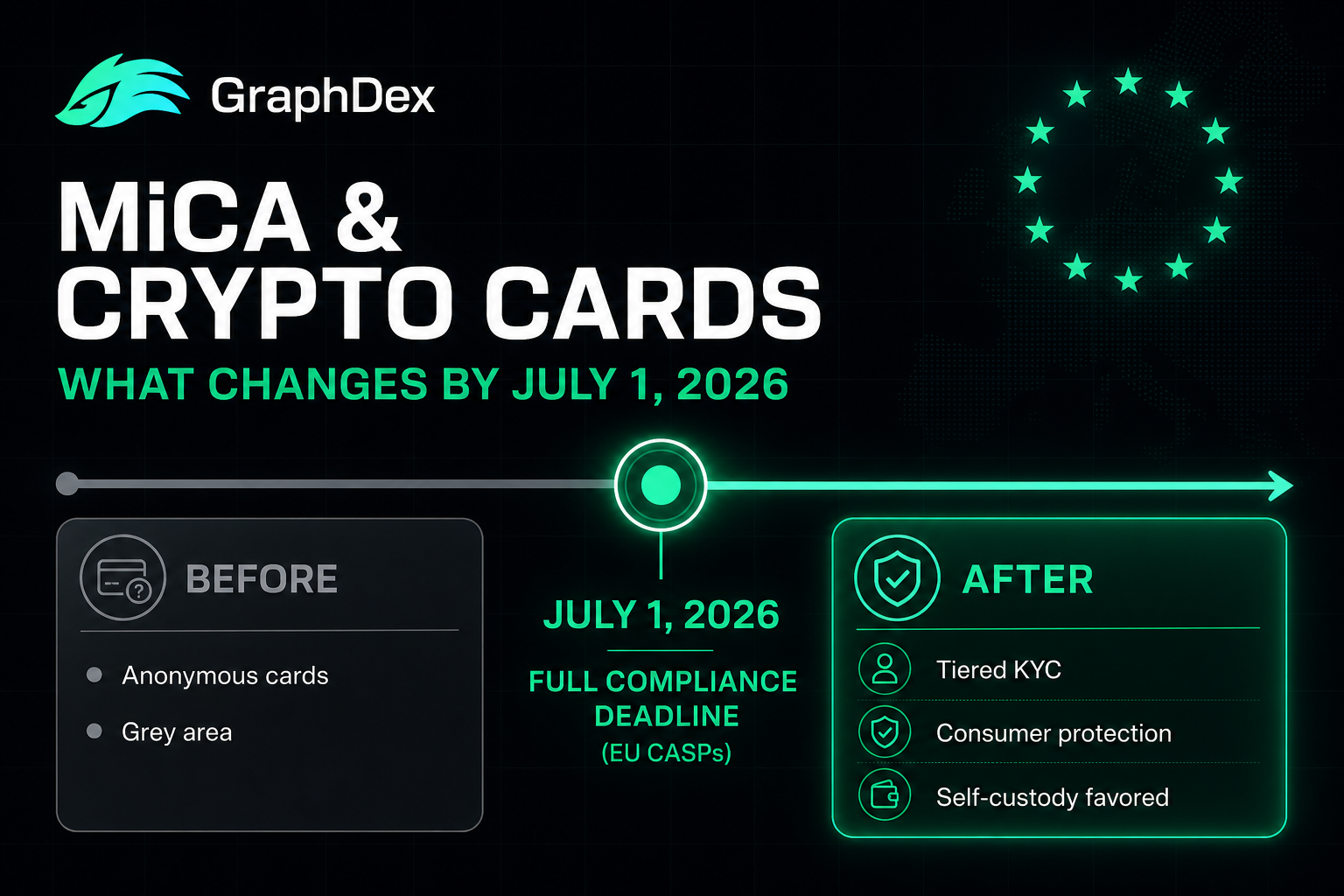

MiCA (Markets in Crypto-Assets) is the EU's comprehensive crypto regulation. For crypto cards, the key changes by July 1, 2026:

- Full compliance mandatory: All Crypto-Asset Service Providers (CASPs) serving EU users must achieve full MiCA authorization by July 1, 2026

- Identity verification required: Anonymous cards are eliminated; tiered KYC (Level 1, 2, 3) becomes the standard

- Consumer protection emphasized: Clearer terms, transparency, and safeguards for users

- Self-custody favored: Non-custodial models align with MiCA's consumer-protection goals (your funds aren't exposed to issuer failure)

- Stablecoin rules: Specific requirements for stablecoins (USDT, USDC) used in payments

What it means for you: Compliant cards are safer and more sustainable. Choose a card that's MiCA-aligned with tiered KYC and ideally non-custodial — these are built to operate long-term, not disappear when enforcement tightens.

Get a MiCA-aligned GraphPay card

Key Takeaways

- MiCA requires full compliance from all EU-serving crypto card providers by July 1, 2026.

- Anonymous cards are eliminated; tiered KYC (Level 1/2/3) becomes the universal standard.

- MiCA emphasizes consumer protection — favoring transparency and self-custodial models.

- Choosing a MiCA-aligned, non-custodial card means choosing one built to last.

What Is MiCA?

MiCA — the Markets in Crypto-Assets regulation — is the European Union's comprehensive framework for regulating crypto assets and services. It's the most significant crypto regulation globally, setting standards that influence the entire industry far beyond Europe.

The core purpose: MiCA brings crypto-asset services under a unified regulatory framework, replacing the patchwork of national rules with a single EU-wide standard. It covers crypto exchanges, wallet providers, stablecoin issuers, and — critically for this guide — crypto card providers (as Crypto-Asset Service Providers, or CASPs).

Why it matters globally: The EU is one of the world's largest markets. Any crypto card provider that wants European users must comply with MiCA. Because building separate compliant and non-compliant versions is impractical, many providers adopt MiCA standards globally. MiCA effectively sets the floor for crypto card practices worldwide.

The key deadline: While MiCA has been phasing in, July 1, 2026 is a pivotal date — by which CASPs operating in the EU must have achieved full compliance. Providers that haven't will face restrictions on serving EU users.

The big picture: MiCA represents crypto's maturation from an unregulated frontier into a regulated financial sector. For crypto cards specifically, it ends the era of anonymous, unregulated cards and establishes a clear, compliant model: verified identity (tiered KYC), consumer protection, and — increasingly — self-custody.

What MiCA Changes for Crypto Cards

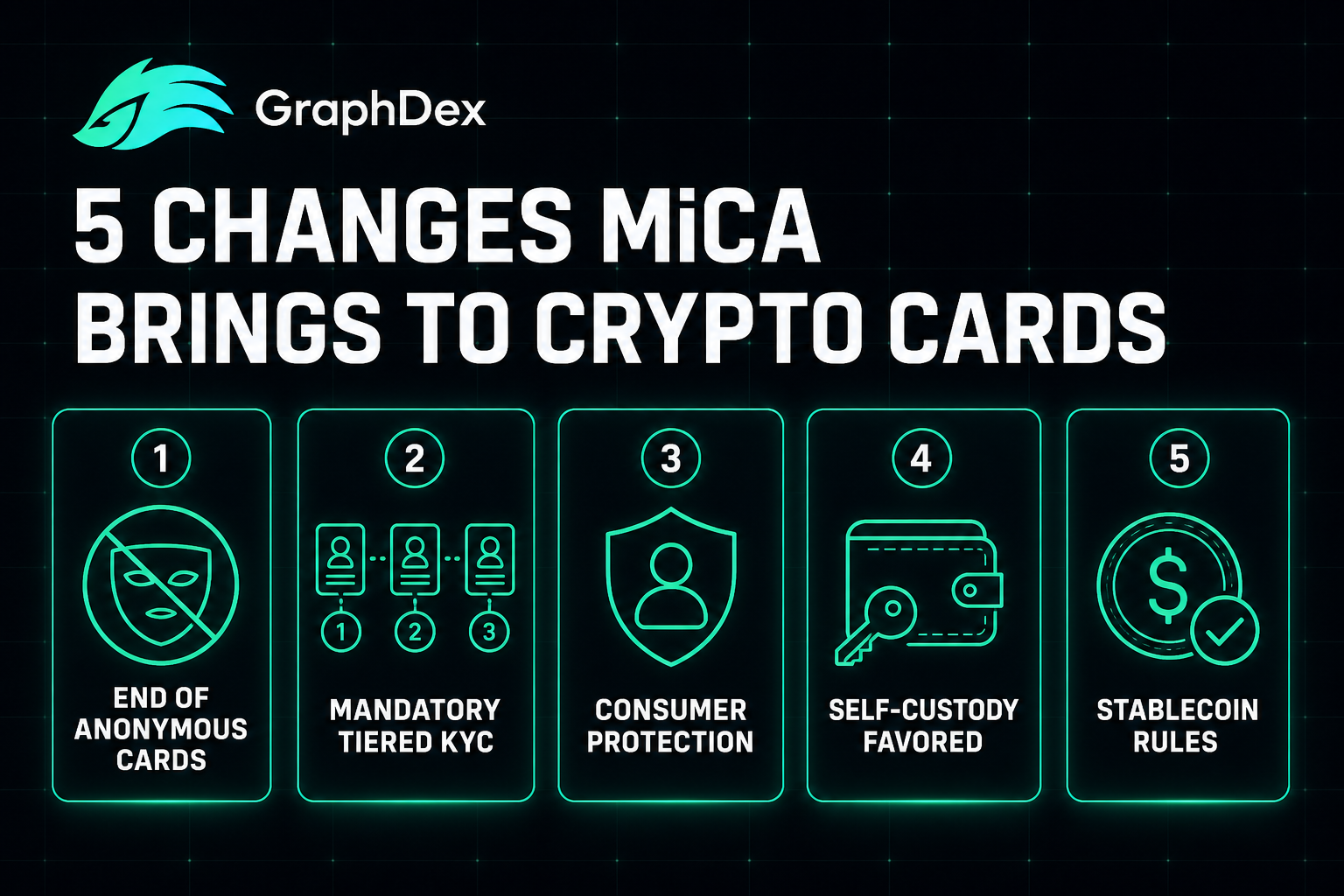

Five concrete changes reshape the crypto card market under MiCA.

1. The End of Anonymous Cards

MiCA requires identity verification for regulated crypto services. This eliminates genuinely anonymous crypto cards from the compliant market. What replaces them is the tiered KYC model — Level 1 (simplified) through Level 3 (full) — where you verify progressively to unlock higher limits.

This isn't a loss for users; it's a shift to a sustainable model. Anonymous cards had a documented history of sudden shutdowns and frozen funds. Compliant tiered cards offer fast Level 1 entry within a framework built to last.

2. Mandatory Tiered KYC

Under MiCA, identity verification scales with activity. Small, low-value transactions can use lighter verification (Level 1); higher limits require fuller verification (Level 3). This is the tiered KYC model — now the universal standard for compliant cards.

3. Enhanced Consumer Protection

MiCA emphasizes protecting users: clearer terms and conditions, transparency about fees and risks, and safeguards around how providers handle funds. For users, this means fewer hidden surprises and more accountability from providers.

4. Self-Custody Favored

MiCA's consumer-protection focus inherently favors self-custodial models. When your funds stay in your own wallet (non-custodial), you're protected from issuer failure — exactly the consumer protection MiCA aims for. Custodial models, where the issuer holds your funds, carry the solvency risk MiCA's safeguards address. This is why non-custodial cards align naturally with MiCA's direction.

5. Stablecoin Requirements

MiCA sets specific rules for stablecoins (like USDT and USDC) used in payments — covering reserves, transparency, and issuer requirements. Since most crypto cards use stablecoins for spending, these rules affect which stablecoins cards can support and how.

The combined effect: MiCA transforms crypto cards from an unregulated grey area into a clear, compliant category — verified identity, consumer protection, and self-custody alignment. The cards built for this model are the ones that will still be operating as enforcement tightens.

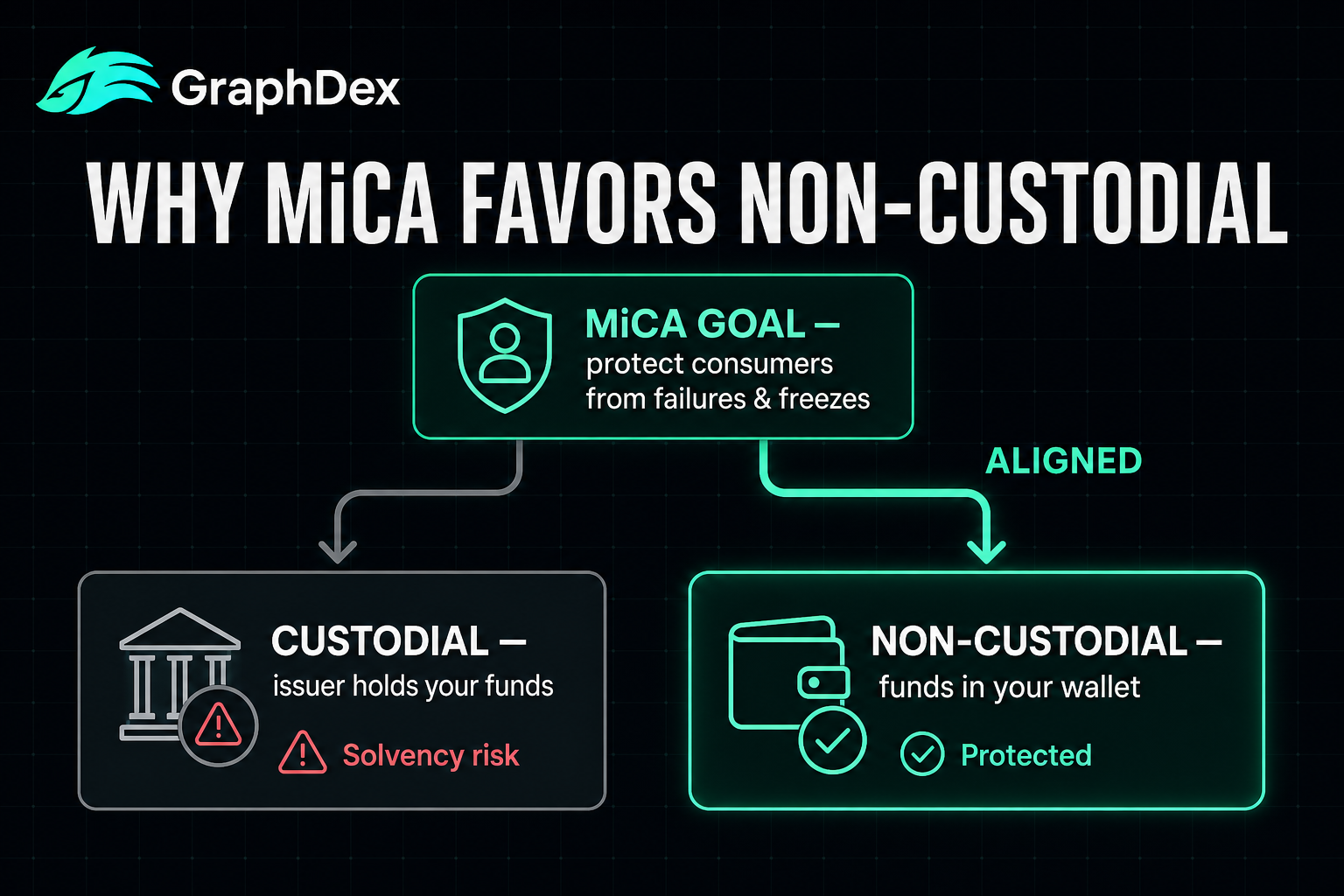

Why MiCA Favors Non-Custodial Cards

A key insight often missed: MiCA's consumer-protection goals align naturally with non-custodial architecture.

The logic:

MiCA aims to protect consumers from the risks that have plagued crypto — failures, freezes, and fund losses. The single biggest such risk is custodial: when a provider holds your funds, their failure becomes your loss.

Non-custodial cards eliminate this risk class. With your funds in your own wallet:

- Provider failure doesn't touch your funds (they were never in custody)

- There's no central fund pool to be frozen or lost

- You retain control regardless of what happens to the provider

This is exactly the consumer protection MiCA seeks. While MiCA doesn't mandate non-custodial models, the architecture inherently delivers the protection MiCA values.

The practical result: As MiCA enforcement tightens, non-custodial cards with tiered KYC represent the model best aligned with regulatory direction — compliant identity verification combined with consumer-protective self-custody. Providers building on this model are positioning for the regulated future, not fighting against it.

The user benefit: Choosing a MiCA-aligned, non-custodial card means choosing a card built to operate sustainably — one less likely to face the restrictions, shutdowns, or freezes that hit non-compliant providers. Your card keeps working, and your funds stay yours.

What MiCA Means for You as a User

How MiCA affects your experience with crypto cards.

You'll Verify Your Identity (Tiered)

Expect KYC — but tiered. You can start at Level 1 (simplified, minimal verification) for small payments, then upgrade to Level 3 (full) for higher limits and physical cards. The verification scales to your needs; you're not forced into full KYC immediately.

Anonymous Cards Are No Longer an Option

If you were considering an "anonymous" crypto card, that era is over in the compliant market. The good news: tiered KYC gives you fast Level 1 access within a framework that won't suddenly shut down or freeze your funds.

More Transparency

MiCA's consumer-protection rules mean clearer terms, more transparent fees, and better disclosure. The hidden-spread tricks common in the unregulated market face more scrutiny under compliant frameworks.

Safer Providers

Compliant providers have met regulatory standards — capital requirements, operational standards, consumer safeguards. This reduces (though doesn't eliminate) the risk of using a provider that fails or behaves badly.

Self-Custody Increasingly Available

As non-custodial models align with MiCA, more cards offer self-custody — letting you keep funds in your wallet while spending compliantly. This is the best of both worlds: regulatory compliance plus the self-custody that makes crypto valuable.

The bottom line for users: MiCA makes crypto cards safer and more sustainable, at the cost of identity verification (tiered, so you control how much). For most users, this is a clear net positive — fast Level 1 entry, consumer protection, transparency, and the growing availability of non-custodial options.

How to Choose a MiCA-Ready Crypto Card

What to look for in a card built for the compliant future:

1. MiCA alignment. The provider should be working toward or have achieved MiCA compliance. This signals they're building for the long term, not operating in a grey area that enforcement will close.

2. Tiered KYC. Look for Level 1 → Level 2 → Level 3 progression. This lets you start light and upgrade as needed — the compliant, flexible model.

3. Non-custodial architecture. Funds in your own wallet align with MiCA's consumer-protection goals and protect you from issuer failure.

4. Transparency. Clear disclosure of fees (including the FX spread), terms, and how funds are handled — consistent with MiCA's transparency requirements.

5. Major networks. Visa/Mastercard rails indicate the provider meets the AML standards these networks require — a compliance signal.

6. Stablecoin support. Support for compliant stablecoins (USDC, USDT) used within MiCA's framework.

The ideal profile: A MiCA-aligned, non-custodial card with tiered KYC, transparent pricing, and major network acceptance. This combination is built to operate sustainably as regulation tightens — your card keeps working, your funds stay yours, and you're never exposed to the risks of non-compliant providers.

Choose a MiCA-aligned GraphPay card

How GraphPay Is Built for the MiCA Era

GraphPay is designed from the ground up for the compliant, post-MiCA crypto card market.

MiCA-aligned by design:

- Tiered KYC: Level 1 → 2 → 3 progression — start light, upgrade as needed, fully compliant

- Non-custodial: Your crypto stays in your own wallet — aligning with MiCA's consumer-protection goals and protecting you from issuer risk

- Transparent: Clear pricing and terms, no hidden-spread tricks

- Major networks: Visa and Mastercard rails meeting AML standards

- Compliant stablecoins: USDT and USDC support within the regulatory framework

Multi-chain foundation:

- Load from BNB Chain, Ethereum, or TRON

- Spend globally on Visa/Mastercard

- Funds stay in your wallet at every level

Why this matters as July 2026 approaches: As MiCA compliance becomes mandatory, cards built on the compliant model — tiered KYC plus non-custodial architecture — are the ones positioned to operate sustainably. GraphPay is built for this future: you get compliant, verified spending while your crypto stays yours. No grey areas, no sudden shutdowns, no surrendering custody.

The compliant future of crypto cards isn't a restriction — it's a safer, more sustainable model. GraphPay is built for it.

Get your MiCA-aligned GraphPay card

Frequently Asked Questions

What is MiCA and how does it affect crypto cards? MiCA (Markets in Crypto-Assets) is the EU's comprehensive crypto regulation. For crypto cards, it requires full compliance from EU-serving providers by July 1, 2026 — eliminating anonymous cards, mandating tiered KYC (Level 1/2/3), emphasizing consumer protection and transparency, and favoring self-custodial models. It transforms crypto cards from an unregulated grey area into a clear, compliant category.

What happens to crypto cards on July 1, 2026? By July 1, 2026, Crypto-Asset Service Providers serving EU users must have achieved full MiCA compliance. Providers that haven't will face restrictions on serving European users. For users, this means anonymous cards disappear from the compliant market, and the remaining cards use tiered KYC with stronger consumer protections. Compliant providers continue operating; non-compliant ones face restrictions.

Are anonymous crypto cards still available under MiCA? No — MiCA requires identity verification for regulated crypto services, eliminating genuinely anonymous cards from the compliant market. What replaces them is tiered KYC: you can start at Level 1 (simplified verification) for small payments and upgrade to Level 3 (full) for higher limits. This is more sustainable than anonymous cards, which had a history of sudden shutdowns.

Does MiCA require non-custodial crypto cards? MiCA doesn't explicitly mandate non-custodial models, but its consumer-protection goals align naturally with them. Non-custodial cards (funds in your wallet) protect you from issuer failure — exactly the protection MiCA seeks. As enforcement tightens, non-custodial cards with tiered KYC represent the model best aligned with regulatory direction.

Is my crypto card safe under MiCA? MiCA makes compliant cards safer through capital requirements, operational standards, consumer safeguards, and transparency rules. The safest profile combines MiCA alignment with non-custodial architecture — compliant identity verification plus funds staying in your own wallet. This protects you from both regulatory restrictions (non-compliant providers) and custodial risk (issuer failure).

How do I know if a crypto card is MiCA-compliant? Look for: stated MiCA alignment or authorization, tiered KYC (Level 1/2/3), transparent fee and term disclosure, major network acceptance (Visa/Mastercard, which require AML standards), and ideally non-custodial architecture. Providers building openly for compliance signal long-term operation. Opacity about compliance or anonymous-card marketing are red flags.

Will MiCA make crypto cards more expensive? Not necessarily. MiCA's transparency requirements actually help users by exposing hidden fees (like the FX spread) that unregulated cards used to bury. Compliance has costs for providers, but competition and transparency tend to benefit users. The bigger effect is safety and sustainability — compliant cards are less likely to shut down or freeze funds.

About This Guide

This guide is published by the GraphPay Research team — building non-custodial crypto payment infrastructure. Our content is based on current regulatory information, the MiCA framework, and 2026 market data.

Sources & data: MiCA provisions, deadlines, and requirements reflect publicly available information as of 2026 and may change as implementation continues. Regulatory details vary and evolve. This guide is educational and not financial or legal advice — always consult qualified legal and compliance professionals and verify current regulations for your situation.

GraphPay is non-custodial crypto payment infrastructure — your crypto, your pay. Learn more at graphpay.io.

Last reviewed: May 2026 · GraphPay Research