By GraphPay Research · Reviewed for accuracy May 2026

Quick Answer

You can spend crypto without traditionally "selling" it using these methods:

- Crypto cards (best for everyday spending): A card converts crypto to fiat only at the point of purchase — your crypto stays in your wallet until you spend. Non-custodial cards (like GraphPay) keep funds in your control.

- Crypto-backed loans: Borrow fiat against your crypto as collateral — you spend the loan, keep the crypto.

- Direct crypto payments: Pay merchants that accept crypto directly (limited acceptance).

- Stablecoin spending: Spend stablecoins (USDT, USDC) that hold steady value, avoiding volatility concerns.

Important tax note: In many jurisdictions, spending crypto (including via a card) can still be a taxable event, because converting crypto to fiat to pay is a disposal. "Without selling" refers to the user experience (you don't manually sell on an exchange) — but tax treatment varies. Always consult a tax professional.

The best everyday method: A non-custodial crypto card — your crypto stays in your wallet, converts only when you spend, and you keep control throughout.

Spend crypto with a GraphPay card

Key Takeaways

- You can spend crypto without manually selling it via crypto cards, crypto-backed loans, or direct payments.

- A non-custodial crypto card keeps your funds in your wallet, converting only at the point of purchase.

- Spending crypto can still be a taxable event in many jurisdictions — consult a tax professional.

- Stablecoins (USDT, USDC) let you spend without volatility concerns while keeping crypto in your wallet.

Why Spend Crypto Without Selling It?

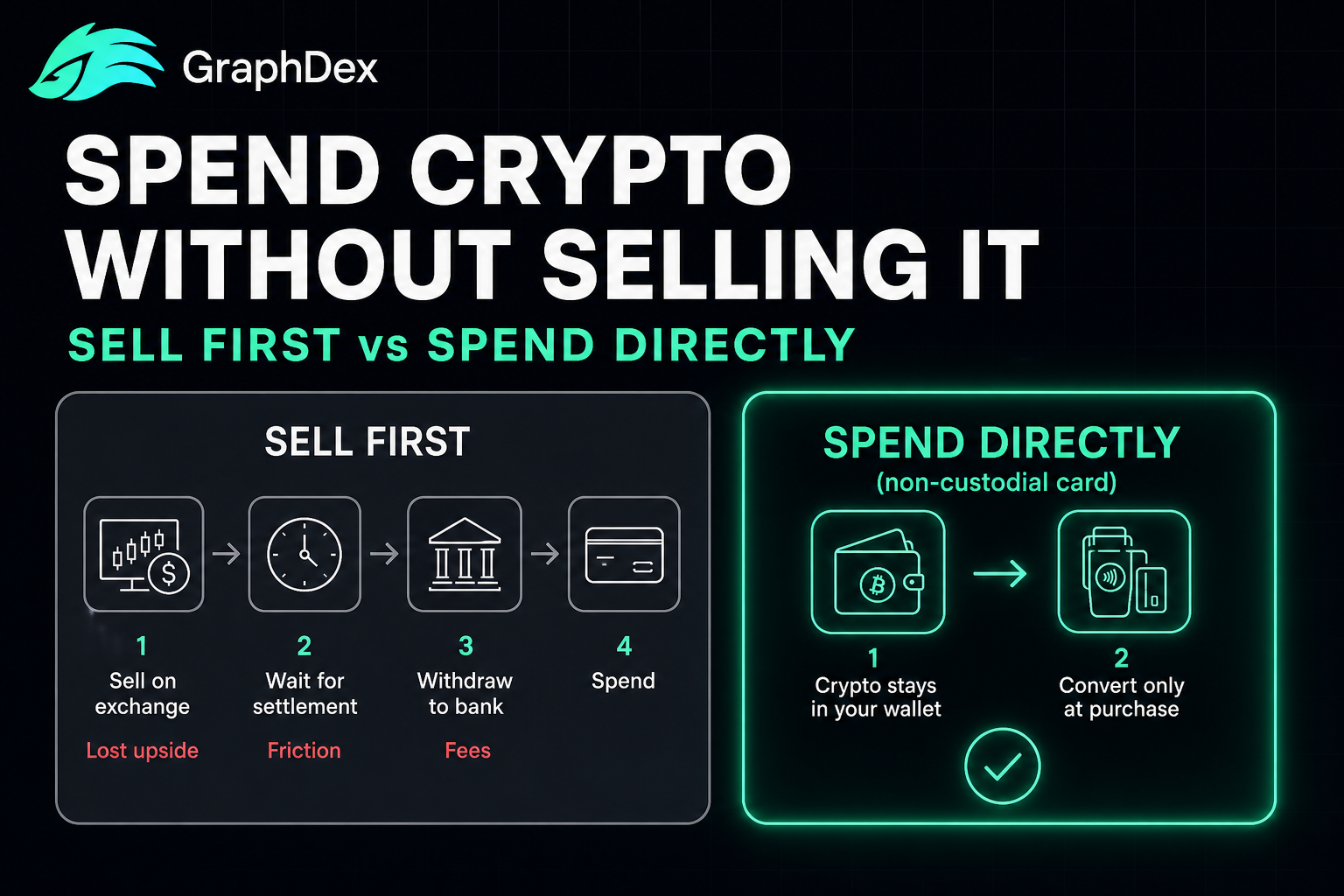

For many crypto holders, the traditional path to spending — sell crypto on an exchange, withdraw fiat to a bank, then spend — is slow, cumbersome, and has downsides. Spending crypto more directly solves several problems.

The problems with selling first:

Lost upside. When you sell crypto to spend, you give up any future price appreciation on those coins. If you sell to buy something and the asset later rises, you've missed that gain.

Friction and time. Selling on an exchange, waiting for settlement, withdrawing to a bank, then spending takes days and multiple steps. It's impractical for everyday purchases.

The "hodler's dilemma." Many crypto holders want to keep their assets long-term but still need to spend in daily life. Selling feels like abandoning their position.

Multiple conversion costs. Each step (sell, withdraw, spend) can carry fees, eating into value.

What spending crypto more directly offers:

- Keep your crypto working until the exact moment you spend

- Avoid the multi-step sell-withdraw-spend process

- Spend at normal merchants without manual exchange transactions

- With the right method, retain control of your assets throughout

The key insight: Modern methods — especially non-custodial crypto cards — let you spend crypto with the convenience of a normal card while your assets stay in your wallet until the instant of purchase. You're not pre-selling; you're converting exactly what you spend, when you spend it.

Method 1: Crypto Cards (Best for Everyday Spending)

The most practical method for everyday spending.

How it works: A crypto card connects to your crypto holdings. When you make a purchase, the card converts the needed crypto to fiat at the point of sale — the merchant receives a normal card payment, and only the amount you spent is converted. The rest of your crypto stays put.

Why it's the best everyday method:

- Works at any merchant accepting the card network (Visa/Mastercard) — tens of millions worldwide

- Converts only what you spend, when you spend it

- No manual exchange transactions

- Online and in-store (with physical cards)

- Apple Pay / Google Pay support (at appropriate verification levels)

Custodial vs non-custodial matters here:

- Custodial cards: You pre-load crypto to the issuer, who holds it. Your crypto is converted/held before you spend.

- Non-custodial cards (like GraphPay): Your crypto stays in your own wallet. The card converts only at the point of sale. You retain control until the instant of purchase.

For spending without selling, non-custodial is ideal — your crypto genuinely stays yours until you spend, rather than being pre-converted or held by a third party. You're keeping your position intact, converting only the exact amount each purchase requires.

This is why a non-custodial crypto card is the best everyday method: maximum convenience (spend anywhere) with maximum control (funds in your wallet until purchase).

Method 2: Crypto-Backed Loans

Borrow against your crypto instead of selling it.

How it works: You deposit crypto as collateral and borrow fiat (or stablecoins) against it. You spend the borrowed funds while keeping your crypto. When you repay the loan, you get your collateral back.

Why people use it:

- Keep your crypto position (and its upside) entirely intact

- Access spending power without selling

- In many jurisdictions, borrowing isn't a taxable event (unlike selling) — though this varies, consult a professional

The risks:

- Liquidation risk: If your collateral's value drops below a threshold, it can be liquidated (sold) to repay the loan — potentially at a bad time

- Interest costs: You pay interest on the loan

- Complexity: More involved than simply spending via a card

Best for: Larger amounts where keeping the full crypto position matters, and you can manage liquidation risk. Less practical for everyday small purchases (where a card is far simpler).

Method 3: Direct Crypto Payments

Pay merchants that accept crypto directly.

How it works: Some merchants accept crypto (often stablecoins or major coins) directly. You send crypto from your wallet to the merchant.

Why it's limited:

- Relatively few merchants accept crypto directly compared to card networks

- Acceptance varies by region and merchant type

- Often requires the merchant to use a crypto payment processor

Where it works well:

- Crypto-native businesses

- Some online services

- Certain regions with higher crypto adoption

The reality: Direct crypto payments work where accepted, but acceptance is far narrower than card networks. For broad everyday spending, crypto cards (which work at any Visa/Mastercard merchant) are far more practical. Direct payments are a useful supplement, not a complete solution.

Method 4: Spending Stablecoins

Spend stable-value crypto to avoid volatility concerns.

How it works: Stablecoins (USDT, USDC) are pegged to fiat currencies, holding steady value. You can spend them via crypto cards, direct payments, or other methods — without worrying about price swings between when you hold and when you spend.

Why it helps:

- No volatility risk during the holding-to-spending window

- Predictable value (1 USDC ≈ $1)

- Widely supported by crypto cards and payment methods

- Ideal for spending money you don't want exposed to crypto price swings

The strategic approach: Many users keep volatile assets (BTC, ETH, SOL) for long-term holding and stablecoins for spending. You spend stablecoins (predictable value) while your volatile assets stay invested for upside. A crypto card supporting stablecoins makes this seamless.

With a non-custodial card: Hold stablecoins in your wallet, spend them via the card (converting to fiat at purchase), and keep your volatile crypto separate and invested. Best of both worlds — stable spending plus growth potential.

Comparison of Methods

| Method | Best For | Keeps Crypto? | Everyday Practical? |

|---|---|---|---|

| Non-custodial crypto card | Everyday spending | Yes (until purchase) | Yes — anywhere cards accepted |

| Crypto-backed loan | Larger amounts | Yes (as collateral) | No — complex for small buys |

| Direct crypto payment | Crypto-friendly merchants | Yes (sent directly) | Limited acceptance |

| Spending stablecoins | Avoiding volatility | Yes (stable assets) | Yes — via card |

The Tax Reality: Read This Carefully

A critical clarification that "spend crypto without selling" content often glosses over.

The key point: In many jurisdictions, spending crypto can still be a taxable event — even via a card — because converting crypto to fiat to make a purchase is treated as a disposal of the asset.

What "without selling" actually means: It refers to the user experience — you don't manually sell on an exchange before spending. The card handles conversion seamlessly. But from a tax perspective, that conversion may still count as a disposal in your jurisdiction.

What this means in practice:

- Spending appreciated crypto may trigger capital gains tax on the gain

- Spending stablecoins (minimal price change) typically has minimal gain/loss

- Crypto-backed loans may avoid the taxable event (borrowing isn't selling) — but this varies

- Tax treatment differs significantly by country

Why stablecoins help here: Since stablecoins hold steady value, spending them typically generates little or no taxable gain (there's minimal price change to tax). This is another reason many users spend stablecoins rather than volatile assets.

The essential advice: Tax treatment of crypto spending varies enormously by jurisdiction and changes over time. This guide cannot give tax advice for your situation. Always consult a qualified tax professional about your obligations before relying on any method. The card you use affects convenience and custody — not your underlying tax obligations.

How to Start Spending Crypto Without Selling

A practical path for everyday spending:

Step 1: Choose a non-custodial crypto card. This keeps your crypto in your wallet, converting only at purchase. Look for tiered KYC (start at Level 1), multi-chain support, and Visa/Mastercard acceptance.

Step 2: Decide what to spend. Many users hold volatile assets long-term and spend stablecoins (USDT, USDC) to avoid volatility and minimize taxable gains. Fund your spending power with stablecoins for predictable value.

Step 3: Verify to your needed level. Start at Level 1 for testing and small payments; upgrade to Level 3 for higher limits and a physical card.

Step 4: Connect your wallet (non-custodial). Your crypto stays in your wallet; the card draws from it only when you spend.

Step 5: Spend normally. Use the card online or in-store anywhere the network is accepted. Each purchase converts only the amount needed.

Step 6: Track for taxes. Keep records of transactions. Spending crypto may be taxable in your jurisdiction — maintain records and consult a tax professional.

This approach lets you spend crypto with card-like convenience while your assets stay in your wallet until the moment of purchase — the practical realization of "spending without selling."

Start spending crypto with GraphPay

How GraphPay Enables Spending Without Selling

GraphPay is built for exactly this use case — spending crypto while keeping it in your wallet.

The non-custodial foundation:

- Your crypto stays in your own wallet at all times

- The card converts only the amount you spend, at the moment you spend it

- You never pre-sell or hand funds to a custodian

- Your position stays intact except for exactly what each purchase requires

Built for practical spending:

- Stablecoin support: Spend USDT or USDC for predictable value and minimal volatility/tax concerns

- Multi-chain: Hold and spend from BNB Chain, Ethereum, or TRON

- Visa & Mastercard: Spend anywhere — tens of millions of merchants

- Tiered KYC: Start at Level 1, upgrade to Level 3 for physical cards and higher limits

The complete picture: With GraphPay, you keep your crypto in your wallet, spend stablecoins for everyday purchases (avoiding volatility and minimizing taxable gains), and convert only what each purchase needs — all while your volatile assets stay invested for upside. It's the practical answer to spending crypto without the downsides of selling first.

Keep your crypto. Spend what you need. Stay in control.

Frequently Asked Questions

How can I spend crypto without selling it? Several methods: (1) A non-custodial crypto card converts crypto to fiat only at the point of purchase, keeping your crypto in your wallet until you spend; (2) Crypto-backed loans let you borrow against crypto and spend the loan; (3) Direct crypto payments at accepting merchants; (4) Spending stablecoins to avoid volatility. A non-custodial card is the most practical for everyday spending.

Is spending crypto a taxable event? In many jurisdictions, yes — even via a card. Converting crypto to fiat to make a purchase is often treated as a disposal, potentially triggering capital gains tax on appreciated assets. "Spending without selling" refers to the user experience (no manual exchange sale), not necessarily tax treatment. Spending stablecoins typically generates minimal taxable gain. Always consult a tax professional.

Does a crypto card count as selling crypto? From a user-experience standpoint, no — you don't manually sell on an exchange; the card converts seamlessly at purchase. But from a tax standpoint, the conversion may count as a disposal in your jurisdiction. With a non-custodial card, your crypto stays in your wallet until the moment of purchase, but tax obligations depend on your local rules. Consult a tax professional.

What's the best way to spend crypto without selling? For everyday spending, a non-custodial crypto card — your crypto stays in your wallet, converting only at purchase, and works anywhere Visa/Mastercard is accepted. Spend stablecoins (USDT, USDC) to avoid volatility and minimize taxable gains while keeping volatile assets invested. For larger amounts, crypto-backed loans keep your full position intact.

Can I keep my Bitcoin and still spend it? Yes, indirectly. Two approaches: (1) Use a crypto-backed loan — borrow against your Bitcoin and spend the loan while keeping the BTC; (2) Hold Bitcoin for the long term while spending stablecoins via a crypto card for daily purchases. The second approach is more practical for everyday spending — keep BTC invested, spend stablecoins.

Why spend stablecoins instead of Bitcoin or other crypto? Two reasons: (1) No volatility risk — stablecoins hold steady value, so you don't lose value if prices swing between holding and spending; (2) Minimal taxable gain — since stablecoins barely change in price, spending them typically generates little or no capital gain to tax. Many users keep volatile assets invested and spend stablecoins for daily purchases.

Do non-custodial crypto cards let me keep my crypto? Yes — that's their core advantage. With a non-custodial card (like GraphPay), your crypto stays in your own wallet, and the card converts only the exact amount you spend, at the moment you spend it. You're not pre-selling or handing funds to a custodian. Your position stays intact except for exactly what each purchase requires.

About This Guide

This guide is published by the GraphPay Research team — building non-custodial crypto payment infrastructure. Our content is based on current payment methods, card industry practices, and 2026 market data.

Sources & data: Spending methods and their characteristics reflect publicly available information as of 2026 and may change. Tax treatment of crypto spending varies significantly by jurisdiction and is not addressed here. This guide is educational and not financial, tax, or legal advice — always consult qualified professionals about your specific situation.

GraphPay is non-custodial crypto payment infrastructure — your crypto, your pay. Learn more at graphpay.io.

Last reviewed: May 2026 · GraphPay Research